.svg)

.png "Investor Ready Capital decorative background element")

Which Advisory Firms Offer Comprehensive Capital Raising Services for Real Estate Developers?

Which Advisory Firms Offer Comprehensive Capital Raising Services for Real Estate Developers?

Most experienced real estate developers do not fail to raise $10M or more because their deals are bad. They fail because they show up to institutional capital with the wrong structure and the wrong advisory model. This guide covers what separates developers who close institutional rounds from those who stall, how to evaluate advisory firms before you sign, and which model is built to protect your promote across multiple raises - not just one.

The rules changed. Understanding how the capital stack for large development projects actually works is no longer optional for developers who want to scale. Institutional LPs in 2026 are asking different questions, running deeper diligence, and choosing fewer new relationships than ever before.

The good news: the capital is there. According to Cushman & Wakefield, CRE fundraising is on pace to hit $129 billion in 2025, up 38% from 2024. Multifamily and industrial attract the strongest LP conviction. Data centers are the fastest-growing allocation category. The capital is moving. The question is whether it moves toward your project or someone else's.

This is the playbook. It covers why most developers stall at the institutional threshold, what the best-capitalized projects do differently, and how to structure your raise so that you close without giving away your promote.

Key Takeaway: The gap between developers who close $10M-$100M institutional rounds and those who don't is not deal quality. It is capital structure, advisory alignment, and access to the right allocators.

Why Most Developers Fail to Raise $10M+

The developers who struggle at the institutional threshold almost always make the same mistakes. They are not bad operators. They have track records, completed projects, and real deals. The problem is structural.

The three most common failure points:

- HNWI-grade packaging, not institutional-grade. A pitch that worked for a $3M HNWI raise will not survive institutional LP due diligence. Institutional allocators want to see a formal capital stack, a defined waterfall, LP protections, and evidence that the GP has thought through every stress scenario.

- No warm access to the right allocators. Most developers cold-pitch family offices or attend conferences hoping to meet the right person. The reality: only about 13% of family offices write checks of $10M or more. The other 87% are not your target. Without a warm introduction system, you are burning time on the wrong relationships.

- Transactional advisors with no skin in the game. A placement agent who earns a cash fee on close has no incentive to help you structure the deal correctly. They move fast, introduce you to whoever is in their Rolodex, and disappear after close. That model does not serve developers who want to build a long-term institutional capital pipeline.

The 2026 Market Reality

According to NAIOP's Fall 2025 research, North American closed-end fundraising volumes have fallen approximately 45% below the 2021 peak. Institutional investors now prefer to limit the number of sponsor relationships they maintain. The bar for adding a new sponsor is much higher than it was three years ago.

This does not mean capital is unavailable. It means the capital is concentrating. Megafunds and specialized operators are winning. Diversified mid-size sponsors without a clear niche or institutional-grade structure are being squeezed out.

What this means for you: If your capital stack, your LP documents, and your advisory relationships are not institutional-grade, you are competing for a shrinking pool of capital with developers who have already done the work.

The Institutional Capital Stack Framework

The best-capitalized development projects share one thing in common: they structure the deal before they go to market. Not after. Not during. Before.

This is the framework that separates developers who close institutional rounds from those who don't.

Step 1: Define Your Capital Stack Before You Pitch

Every institutional LP wants to know exactly where they sit in the capital structure. That means you need to define each layer before the first meeting.

A typical institutional capital stack for a $20M-$50M development project looks like this:

The GP co-investment requirement is real. Institutional LPs now expect GPs to contribute 1-10% of total equity. It signals alignment. If you are not prepared to put capital in alongside your LPs, many institutional allocators will not engage.

Step 2: Design the Waterfall Before You Negotiate

The waterfall determines how profits flow from the project to you and your LPs. Get this wrong and you give away your upside. Get it right and a GP contributing 10% of equity can achieve a 46.2% IRR while LPs earn a healthy 15.4% IRR, as demonstrated in Wall Street Prep's waterfall analysis via James Moore & Co.

The standard institutional waterfall has four tiers:

- Return of capital - 100% to LPs until invested capital is returned

- Preferred return - 100% to LPs until they earn their preferred return (typically 8-10%)

- Catch-up - 100% to GP until GP has received its promote percentage of total profits

- Residual - Split between LP and GP per the agreed promote structure (commonly 80/20)

The specific hurdle rates and promote percentages are negotiable. But you need to walk into every LP meeting with a fully modeled waterfall. If you are still figuring it out during negotiations, you have already lost leverage.

Step 3: Choose the Right Waterfall Structure

The choice between an American (deal-by-deal) waterfall and a European (fund-level) waterfall has a direct impact on when you get paid.

American waterfall: Promote is calculated and paid on each deal as it closes. This accelerates your promote payments and is far better for cash flow. It is the preferred structure for emerging managers and developers who are not running a blind pool fund.

European waterfall: Promote is calculated at the fund level, after all capital is returned. You wait longer. This structure is standard for large institutional funds but puts GPs at a disadvantage if earlier deals outperform later ones.

For most developers raising $10M-$100M on a deal-by-deal basis, the American waterfall is the right structure. It protects your economics and is increasingly acceptable to institutional LPs who are shifting toward deal-by-deal structures anyway.

Step 4: Build Your LP Due Diligence Package

Institutional LPs run a different diligence process than HNWIs. They want:

- Track record documentation for every completed project (cost, timeline, returns)

- Audited financials or CPA-reviewed statements

- Fully modeled waterfall with stress scenarios

- Legal LP agreement with defined protections

- Market analysis specific to the asset class and geography

- Sponsor background checks and references

If any of these are missing, the diligence process stalls. Most developers underestimate how thorough institutional LP diligence actually is.

What Institutional LPs Actually Ask

Most developers prepare for the question "what is the return?" That is not the question that kills deals.

The questions that kill deals are:

- "What happens if the project runs 18 months over schedule?"

- "How are you personally aligned with LP capital?"

- "What is your plan if the exit market softens?"

- "Who else have you raised from and can we speak with them?"

Institutional LPs in 2026 are not making bets on returns projections. They have seen too many pro formas that did not survive contact with reality. They are making bets on operators. They want to know that you have been through a difficult cycle and come out the other side. They want to see that your incentives are aligned with theirs through the full life of the project.

The Alignment Question

The single most important thing an institutional LP is evaluating is alignment. Are you, the GP, incentivized to perform? Or are you incentivized to collect fees and move on?

This is why the advisory model matters. A transactional placement agent who earns a cash fee on close is not aligned with you. They close the deal and move on. An equity-aligned advisor who takes 3-5% advisory equity only wins when you win. That distinction changes the entire dynamic of how a raise is structured and executed.

Understanding how the choice between debt and equity structures affects your long-term economics is foundational to answering the alignment question correctly in every LP meeting.

The Access Problem

Even if your structure is perfect, you still need to get in front of the right LPs. This is where most developers hit a wall.

Family offices are the most active deal-by-deal investors for $10M-$50M raises. But most family offices deploy $1M-$5M per deal. Only 13% write checks of $10M or more. That means your target universe is much smaller than it appears. Cold outreach to family offices rarely works. They receive hundreds of deal submissions and respond to almost none of them.

The developers who close institutional rounds have warm introductions. They are referred by advisors, co-investors, or existing LP relationships. Building that introduction network takes years unless you have an advisor with the right relationships already in place.

The Promote Protection Playbook

Protecting your promote is not about being greedy. It is about making sure the economics you negotiated at the start of the deal are still intact at the end.

There are three ways developers give away too much promote without realizing it.

{{main-cta}}

1. Weak Waterfall Design

A poorly designed waterfall can cost a GP millions at exit. The most common mistake is agreeing to a high preferred return without modeling what that means across different performance scenarios.

If your preferred return is 10% and the deal takes four years to exit, LPs need to earn 10% annually before you see a dollar of promote. In a scenario where the project underperforms, that preferred return accrues and compounds. By the time you exit, LPs may have received their full preferred return plus capital, leaving little room for your promote.

The solution: model the waterfall across at least three scenarios (base case, downside, extended hold) before you sign any LP agreement. Know exactly what you earn under each scenario.

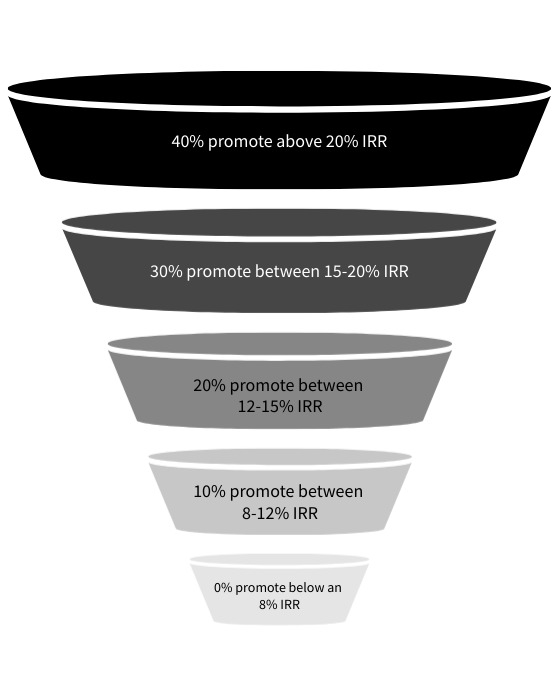

Tiered promote structures are becoming the institutional standard and actually protect GP economics better than a flat 20% promote. Industry data shows tiered structures might include:

- 0% promote below an 8% IRR

- 10% promote between 8-12% IRR

- 20% promote between 12-15% IRR

- 30% promote between 15-20% IRR

- 40% promote above 20% IRR

This structure rewards exceptional performance and gives LPs confidence that the GP is not earning promote on mediocre returns.

2. Compounding Preferred Returns

Watch the difference between cumulative and non-cumulative preferred returns. Cumulative preferred returns carry forward if a distribution period misses the hurdle. They compound. Over a four-year hold with uneven cash flows, compounding preferred returns can add hundreds of thousands of dollars to what LPs receive before your promote kicks in.

Non-cumulative preferred returns do not carry forward. Unpaid preferred returns from one period simply lapse. This is significantly better for GP economics and is a negotiating point most developers do not push on.

3. Clawback Provisions

A clawback provision requires the GP to return previously paid promote if the fund or deal ultimately underperforms the agreed hurdle. For deal-by-deal structures, this is less common. For fund structures, it is standard.

If you are raising a fund rather than a single deal, read every clawback provision carefully. The mechanics of how clawback is calculated, and over what time period, can significantly affect your actual economics at fund wind-down.

The bottom line: Your promote is your most valuable asset as a GP. Protecting it requires understanding every clause in your LP agreement before you sign it.

The Transactional Broker Problem (And What to Do Instead)

Most developers who have tried to raise institutional capital have worked with a placement agent at some point. The experience is often the same: the agent makes introductions, the developer pitches, and if a deal closes, the agent collects a fee and moves on. The next raise starts from scratch.

This model has a fundamental problem. It is optimized for the agent's outcome, not yours.

How Placement Agents Are Compensated

A typical placement agent charges 1-3% of capital raised as a cash fee at close. Some charge retainers. Almost none take equity. This means:

- They have no incentive to help you structure the deal before going to market

- They have no incentive to ensure the LP relationship is durable

- They have no incentive to support your next raise

The fee is earned at close. After that, you are on your own.

The Equity-Aligned Alternative

An equity-aligned capital advisor takes 3-5% advisory equity in the engagement. They only earn when you earn. This alignment changes everything.

IRC Partners operates on the equity-aligned model. One engagement covers all future capital events through exit. The firm only wins when the developer wins. That is the model that produces durable institutional relationships, not one-time closes.

For developers who plan to bring multiple projects to market, working with an advisory firm that structures your capital formation strategy for the long term is not just better. It is the only model that makes sense.

Case Study: From Stalled HNWI Raise to $28M Institutional Close

A mid-sized multifamily developer with six completed projects and a strong track record had spent eight months trying to raise $25M for a ground-up multifamily development in a high-demand Sun Belt market. They had pitched 30+ family offices. They had two soft commitments that never converted. Their placement agent had gone quiet.

The problem was not the deal. The market was strong. The developer's track record was real. The problem was the structure.

"When we looked at their LP package, the waterfall had no defined catch-up mechanism, the preferred return was cumulative and compounding at 10%, and there was no stress scenario modeling. Any institutional LP running proper diligence would have flagged all three immediately."

IRC Partners restructured the capital stack before going back to market. The preferred return was renegotiated to 8%, non-cumulative. The waterfall was redesigned with a tiered promote structure. Stress scenarios were modeled across three exit timelines. The LP package was rebuilt to institutional standards.

Within six months of restructuring, the developer closed $28M in institutional LP equity through IRC's network of family offices and private equity allocators. The developer's promote was protected. The LP relationship was structured for multiple future deals.

The lesson: The deal quality was never the issue. The structure was. Fix the structure first, then raise.

This is the model IRC Partners applies to every engagement. For a deeper look at how advisory firms that offer comprehensive capital raising services differ from placement agents, the distinction comes down to what happens before the first LP meeting.

What Developers Should Do Next

If you are a seasoned developer with 3+ completed projects and a deal requiring $10M-$100M in institutional capital, here is where to start.

Step 1: Audit your current capital stack. Does it reflect institutional standards? Is your waterfall fully modeled? Is your preferred return structure competitive?

Step 2: Map your allocator access. How many of your current LP relationships write $10M+ checks? How many are family offices vs. HNWIs? If most of your capital comes from HNWIs writing $500K-$2M checks, you have an access problem.

Step 3: Evaluate your advisory relationship. Is your current advisor equity-aligned? Do they support every raise or just one transaction? Are they embedded in your capital formation strategy or transactional?

Step 4: Assess your LP due diligence package. Would it survive institutional scrutiny? Have you stress-tested your waterfall? Do you have audited or CPA-reviewed financials?

If any of these steps reveal gaps, that is where to focus before your next raise. The developers who close institutional rounds are not luckier or better operators. They are better prepared.

IRC Partners works with experienced developers on exactly this process. The firm structures the capital stack, designs the waterfall, prepares the LP due diligence package, and then coordinates warm introductions to institutional allocators through a network of 307,000+ investors and 77 global investment bank syndicate partners.

One engagement covers all future capital events. IRC only wins when you win.

For developers ready to move beyond HNWI capital and build a true institutional platform, the next step is a conversation. IRC accepts a maximum of 10 new strategic partners per quarter, by application only.

Frequently Asked Questions

What is the minimum track record required to raise institutional capital?

Most institutional LPs require a minimum of 3 completed development projects with documented returns. In 2026, the bar is higher than in previous years; investors heavily favor operators who can demonstrate a verifiable track record across at least one full market cycle to prove resilience.

How long does it take to raise $10M–$100M for a project?

A well-structured raise typically takes 4 to 9 months. Poorly organized efforts or cold outreach can easily extend this to 18 months. Having your capital stack, waterfall, and due diligence package pristine and ready before your first pitch is the most effective way to compress this timeline.

What is a GP promote and how do I protect it?

The GP promote is the developer's share of profits above the LP preferred return, typically 20%. To protect your promote, you must design waterfalls with favorable hurdle rates and avoid compounding preferred returns. It is vital to model various stress scenarios to ensure the promote remains intact even if project costs rise.

What is the difference between an American and European waterfall?

An American waterfall pays the GP promote on a deal-by-deal basis as each asset is sold or refinanced. A European waterfall only pays the promote after 100% of all LP capital across an entire fund is returned. For developers raising capital on a per-project basis, the American structure is superior for maintaining healthy cash flow.

How much GP equity co-investment do institutional LPs require?

LPs typically expect a GP co-investment of 1% to 10% of the total project equity. This skin in the game is a critical signal of alignment; without a meaningful financial commitment from the developer, many institutional allocators will refuse to engage regardless of the project's quality.

What asset classes attract the strongest conviction in 2026?

Multifamily and Industrial remain the top conviction sectors for institutional capital. Data centers are currently the fastest-growing allocation category, followed by life sciences and mixed-use residential. Sponsors who lack a clear, specialized focus in one of these areas currently face significant difficulty accessing capital.

What is the biggest mistake developers make when pitching LPs?

Using HNWI-grade materials for institutional meetings. Institutional allocators require formal capital stacks, stress-modeled waterfalls, and audited financials. Failing to provide these sophisticated materials signals a lack of institutional readiness and usually results in an immediate screen-out.

Continue reading this series:

- Which advisory firms offer comprehensive capital raising services for developers?

- Which firms offer the best anti-dilution protections for real estate developers?

- Top firms for real estate capital raising without losing equity

The wrong structure doesn't just cost you this round. It costs you the next three. IRC Partners advises founders raising $5M to $250M of institutional capital. If you're about to go to market and want the structure reviewed before investors see it, book a call here

Need guidance on your capital raise?

What Do Pension Funds and Endowments Require Before Investing in a First-Time Real Estate Fund?

.webp "How to Value a Startup Complete Valuation Guide for Founders (2026)")

How to Value a Startup: Complete Valuation Guide for Founders (2026)

When Does a Company Need Capital Raising Outcomes and Advisor Success Rates

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of seven

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.