.svg)

.png)

Raising Capital for Real Estate: How to Choose the Right Advisory Firm

When a developer searches for help raising $10M or more in institutional capital, they quickly discover that the advisory landscape is crowded and confusing. Every firm claims to raise capital. Very few actually do what developers at the institutional level need.

The difference between a comprehensive capital advisory firm and a transactional placement agent is not marketing language. It shows up in how your deal is structured, how your LP relationships are managed, and how much of your promote you keep. If you are serious about building the institutional capital stack your next project requires, the type of firm you choose matters more than almost any other decision you make before going to market.

Understanding how capital instruments are structured before going to market is the foundation every developer needs before evaluating any advisory firm's claims.

This article breaks down the four types of advisory firms developers use for capital raising, what each actually does, and what questions to ask before signing any engagement.

Key Takeaway: Most advisory firms offer access. A comprehensive capital advisory firm offers structure, access, due diligence preparation, waterfall design, and ongoing support across every raise. Those are not the same service.

The 4 Types of Capital Raising Firms Developers Use

Not all advisory firms are built the same. Understanding the differences is the first step to choosing the right partner for a $10M+ institutional raise.

Type 1: Placement Agents

Placement agents are the most common type of firm developers encounter. They maintain a network of investor contacts and earn a cash fee (typically 1-3% of capital raised) when a deal closes. Some also charge upfront retainers.

What they do: Make introductions to investors in their network. Facilitate meetings. Sometimes assist with pitch materials.

What they don't do: Structure the capital stack. Design the waterfall. Prepare LP due diligence packages. Support future raises.

Best for: Developers who already have an institutional-grade structure and just need introductions to investors they don't already know.

The risk: A placement agent's incentive is to close quickly and collect the fee. They are not aligned with your long-term economics or your next raise.

Type 2: Investment Banks (Middle-Market)

Middle-market investment banks offer capital raising as part of a broader suite of services that may include M&A advisory, debt placement, and structured finance. They are typically more expensive than placement agents and more process-driven.

What they do: Formal capital raising processes, investor marketing materials, structured deal processes. Some offer capital stack advisory.

What they don't do: Take equity positions in client engagements. Provide ongoing advisory beyond the transaction. Specialize in real estate developer economics.

Best for: Larger, more institutional developers raising $50M+ who need a formal process and the credibility of a recognized firm name.

The risk: High fees, slow processes, and advisors who are generalists rather than real estate capital specialists.

Type 3: Real Estate Brokers with Capital Advisory Services

Some commercial real estate brokerage firms have added capital advisory arms. These teams typically focus on debt placement (construction loans, bridge loans) and may also handle equity introductions.

What they do: Debt placement. Some equity introductions. Market knowledge.

What they don't do: Architect institutional-grade equity capital stacks. Design waterfall structures. Provide comprehensive LP due diligence preparation.

Best for: Developers primarily seeking debt financing with some equity introduction capability.

The risk: Their core business is brokerage. Capital advisory is a secondary service line, not their primary expertise.

Type 4: Equity-Aligned Capital Advisory Firms

This is the smallest category and the most relevant for developers seeking $10M-$100M in institutional LP equity. These firms take equity positions in client engagements, structure deals before going to market, and maintain ongoing relationships with institutional allocators.

What they do: Capital stack architecture, waterfall design, LP due diligence preparation, warm introductions to institutional allocators, and ongoing advisory across all future raises.

What they don't do: Earn cash fees at close. Disappear after a single transaction. Work with any developer who walks in the door.

Best for: Experienced developers (3+ completed projects) raising $10M+ in institutional LP equity who want a long-term capital formation partner, not a one-time transaction.

The risk: Selectivity. These firms work with fewer clients. Getting accepted into an engagement requires a strong track record and a fundable deal.

What "Comprehensive" Actually Means for a $10M+ Raise

The word "comprehensive" gets used loosely in the advisory space. Here is what it actually means for a developer raising $10M or more in institutional capital.

A comprehensive capital raising service for real estate developers covers six distinct areas. Most firms cover one or two. A true comprehensive advisory firm covers all six.

The gap between "sometimes" and "yes" in this table represents the difference between a developer who closes and one who stalls.

Why Incentive Alignment Is the Most Important Factor

According to NAIOP's research on accessing institutional capital, institutional LPs in 2026 are placing a premium on alignment. They want to see that everyone involved in a deal has skin in the game. That includes the GP, the LP, and increasingly, the advisory firm.

When your advisor earns only when you earn, their incentives shift. They push back on bad deal structures. They refuse to introduce you to investors who are not a fit. They help you prepare for diligence questions you have not thought of yet. That is what alignment looks like in practice.

A transactional advisor who earns a cash fee at close has no reason to do any of those things. The fee is the same whether the deal structure is optimal or not.

The Ongoing Advisory Requirement

Most developers underestimate how important ongoing advisory support is across multiple raises. Institutional LP relationships are long-term. The family office that invested in your first institutional deal is a candidate for your second, third, and fourth project. Managing those relationships, updating LPs on project performance, and positioning your next deal with existing investors is a continuous process.

A transactional placement agent does not do this. An equity-aligned advisory firm does. For developers who plan to build a true institutional platform, the ongoing advisory relationship is not a nice-to-have. It is the foundation of the entire capital formation strategy. Part of that ongoing work is sourcing the right institutional allocators for each successive raise, not recycling the same contact list from the previous deal.

Understanding how anti-dilution protections and waterfall structures affect your long-term economics is a core part of what a comprehensive advisory firm helps you navigate across every raise. Developers who skip this step often discover the most common structural mistakes that kill an institutional raise only after they have already lost leverage in negotiations.

10 Questions to Ask Any Advisory Firm Before Signing

Before engaging any advisory firm for a $10M+ raise, ask these questions. The answers will tell you everything you need to know about whether the firm is actually comprehensive or just claims to be.

- How are you compensated? Cash fee at close, retainer, equity, or some combination? An equity-aligned advisor only earns when you earn.

- Do you help structure the capital stack before going to market, or only after? A comprehensive advisor structures the deal first. A placement agent starts pitching immediately.

- Do you design the waterfall, or do you expect us to bring one? A comprehensive advisor has the expertise to architect the waterfall. A placement agent does not.

- How many institutional allocators do you have warm relationships with, and what is the average check size? Generic answers like "hundreds of investors" are a red flag. Ask specifically about allocators who write $10M+ checks.

- What does your LP due diligence preparation process look like? If the answer is vague or non-existent, they are not a comprehensive advisor.

- How many developers are you currently working with? A firm working with dozens of clients simultaneously cannot provide the focused attention a $10M+ raise requires.

- Does one engagement cover future raises, or do we need to re-engage for each transaction? A comprehensive advisor embeds across your entire capital formation strategy. A transactional advisor re-charges for every deal.

- Can you provide references from developers who have closed $10M+ with your firm? Any reputable advisory firm should be able to provide references.

- What happens if the raise does not close? Understanding the risk allocation in the engagement agreement tells you a lot about incentive alignment.

- What is your process for matching us with the right allocators, not just available ones? A comprehensive advisor pre-qualifies investors for fit. A placement agent blasts their contact list.

The right answers: An equity-aligned, comprehensive advisory firm will answer these questions with specificity. They will describe a structured process, a defined network, and a compensation model that ties their outcome to yours. If the answers are vague, the firm is transactional.

How IRC Partners Delivers Comprehensive Capital Advisory

IRC Partners is an equity-aligned national capital advisory firm that works exclusively with experienced real estate developers raising $10M or more in institutional capital. The firm does not operate as a placement agent. It does not charge cash fees at close.

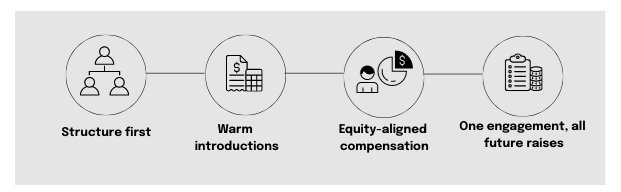

IRC's Embedded Capital Partner model works as follows:

- Structure first: IRC architects the institutional-grade capital stack before any investor meetings. This includes waterfall design, preferred return structuring, stress scenario modeling, and LP due diligence package preparation.

- Warm introductions: IRC coordinates introductions to institutional allocators through a network of 307,000+ investors and 77 global investment bank syndicate partners. The firm focuses specifically on the 13% of family offices that write $10M+ checks, not the broader universe of smaller allocators.

- Equity-aligned compensation: IRC takes 3-5% advisory equity in each engagement. The firm only wins when the developer wins.

- One engagement, all future raises: A single IRC engagement covers all future capital events through exit. Developers do not re-engage and re-pay for each transaction.

For developers who want to understand how to preserve equity across multiple raises while accessing institutional capital, the IRC model is specifically designed to solve that problem. For a deeper look at how large-scale raises are structured from the ground up, the $100M raise playbook outlines the process and investor expectations at the institutional level.

IRC Partners accepts a maximum of 10 new strategic partners per quarter, by application only. This selectivity is intentional. It ensures every developer in an IRC engagement receives the focused attention that a $10M+ institutional raise requires.

IRC's network includes family offices managing $17B+ that request deal referrals directly from the firm. That means developers in an IRC engagement are not cold-pitching. They are being introduced to allocators who are already interested in the asset class and deal type.

Frequently Asked Questions

What is the difference between a placement agent and a capital advisory firm?

A placement agent primarily makes investor introductions and earns a cash fee upon closing. In contrast, a capital advisory firm structures the deal, designs the waterfall, and prepares due diligence materials. The clearest signal is compensation: placement agents earn cash, while equity-aligned advisors earn a stake in the project.

How do I know if an advisory firm has real access to institutional allocators?

Ask for specifics: how many current relationships write $10M+ checks per deal and can they provide references from developers who closed at that size? Vague mentions of extensive networks are a red flag; genuine institutional access is always backed by a specific track record of large-scale closures.

What should a comprehensive capital raising service include?

It must include capital stack design, waterfall structuring with stress scenarios, a full LP due diligence package, and warm introductions to institutional allocators. Post-close support for future raises is also vital to ensure the developer can scale beyond a single project.

How are advisory fees structured for institutional real estate raises?

Placement agents typically charge 1% to 3% of capital raised in cash. Equity-aligned advisory firms often take 3% to 5% advisory equity with no cash fee at close. This model aligns the advisor’s success with the developer’s long-term outcomes rather than just transaction speed.

Can mid-size firms access institutional capital without a major bank?

Yes. Equity-aligned advisory firms with direct relationships to family offices and private equity allocators provide access to the same capital pools as middle-market banks. These firms often offer better incentive alignment and specialized expertise without the overhead of a large institution.

How many developers should an advisory firm work with at one time?

Fewer is better. A firm managing dozens of clients cannot provide the deep focus needed for a complex $10M+ raise. Look for firms that intentionally limit their roster to a few strategic partners per quarter to ensure your project receives the necessary attention.

Do advisory firms help with both equity and debt?

Most comprehensive advisory firms focus on the equity side, specifically LP and preferred equity. While some coordinate debt, debt placement is often a separate specialized service. The primary value for an institutional raise lies in securing the right equity partners who provide the foundation for the project.

IRC Partners advises founders raising $5M to $250M of institutional capital on structure, positioning, and round architecture. 7 strategic partners per quarter. No placement agent model. No success-only theater. If you want a structural review of your current raise, apply at HERE

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.