.svg)

.png "Investor Ready Capital decorative background element")

Which Firms Offer the Best Anti-Dilution Protections for Real Estate Developers?

Which Firms Offer the Best Anti-Dilution Protections for Real Estate Developers?

When most people hear "anti-dilution protection," they think of startup equity rounds and venture capital term sheets. For real estate developers, the concept is different but equally critical. Anti-dilution in real estate is not about share price adjustments. It is about protecting your promote, your waterfall, and your carried interest across every raise you do.

The developers who give away too much equity are rarely doing it on purpose. It happens through weak waterfall design, compounding preferred returns, clawback provisions buried in LP agreements, and advisory relationships that are not aligned with GP economics. As part of the broader institutional capital playbook for real estate developers, understanding how to protect your economics before you sign is one of the highest-leverage things you can do.

This article explains what anti-dilution actually means in a real estate context, the three most common ways developers give away too much, and what to look for in an advisory firm that takes GP economics seriously.

Key Takeaway: Anti-dilution protection for real estate developers is about waterfall design, preferred return mechanics, and clawback provisions, not share price formulas. The advisory firm you choose either helps you protect these economics or ignores them.

How Anti-Dilution Actually Works in Real Estate (It Is Not What You Think)

In startup equity, anti-dilution protection is a clause that adjusts your share count if a future round prices below your entry valuation. That definition does not apply here.

For real estate developers, anti-dilution protection means something different. It means designing the deal so that the promote you negotiated at the start is still intact at exit. It means structuring the waterfall so compounding preferred returns do not eat into your carried interest. It means reading every clawback clause before you sign.

Most developers who give away too much do not know it happened until the deal closes and the distributions come out.

Key Takeaway: Anti-dilution for real estate GPs is about three things: waterfall design, preferred return mechanics, and clawback provisions. The advisory firm you choose either helps you protect all three or ignores them entirely.

Why This Is Different From the Startup World?

Startup anti-dilution protections are backward-looking. They protect you from a down round.

Real estate anti-dilution protections are forward-looking. They protect you from a waterfall structure that looks fair on paper but pays you far less than you expected at exit.

The developers who lose the most are not the ones who negotiated badly. They are the ones who signed LP agreements without modeling what the waterfall actually produces under different exit scenarios. A 10% preferred return sounds reasonable. But if it is cumulative and compounding over a four-year hold with uneven cash flows, it can add hundreds of thousands of dollars to what LPs receive before your promote kicks in.

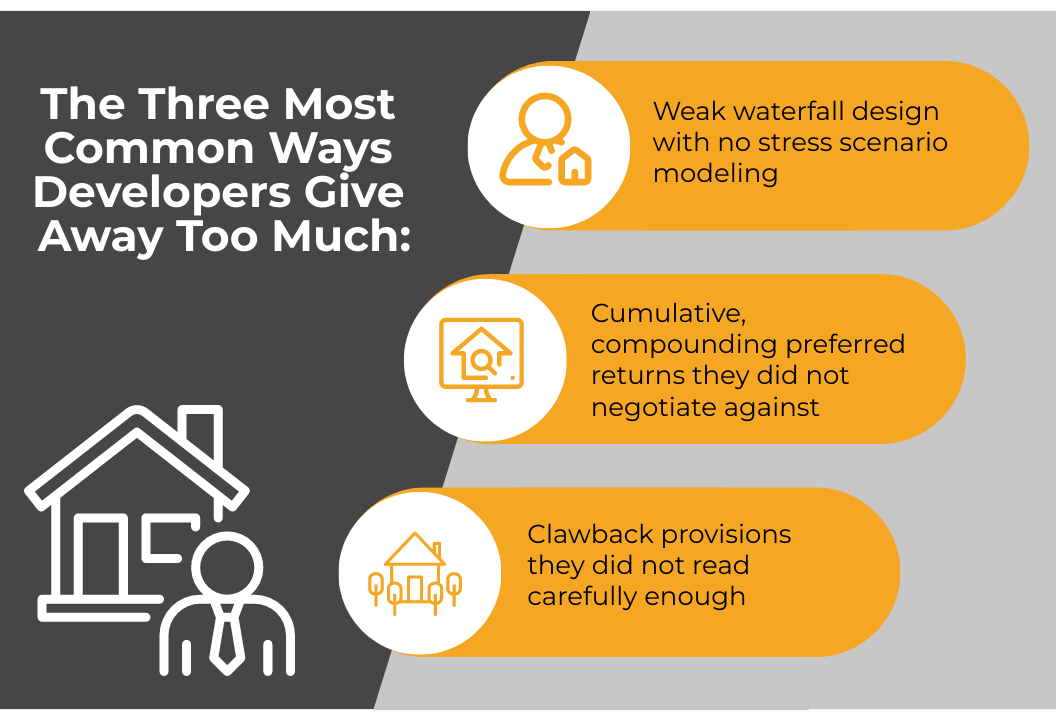

The three most common ways developers give away too much:

- Weak waterfall design with no stress scenario modeling

- Cumulative, compounding preferred returns they did not negotiate against

- Clawback provisions they did not read carefully enough

American vs. European Waterfall: Which Structure Protects Your Promote?

The single most consequential structural decision for GP economics is the choice between an American (deal-by-deal) waterfall and a European (fund-level) waterfall. Most developers do not push on this hard enough.

What Is The American (Deal-by-Deal) Waterfall?

The American waterfall calculates and pays the promote on each deal as it closes. You do not wait for the entire fund to wind down. If deal one performs, you get paid on deal one.

Why this matters: For developers who are not running a large blind pool fund, the American waterfall is almost always the right structure. It accelerates your promote payments and protects your cash flow. It also means a single underperforming deal does not wipe out promote you already earned on earlier exits.

According to NAIOP's research on accessing institutional capital in 2026, family offices are increasingly moving toward deal-by-deal structures rather than blind pool fund commitments. This shift actually benefits developers who push for American waterfall terms, because the LP preference and the GP preference are now aligned.

What Is The European (Fund-Level) Waterfall?

The European waterfall calculates promote at the fund level, after all LP capital across the entire fund is returned. You wait. If early deals outperform but later deals underperform, you may earn far less promote than your track record deserves.

Why this hurts emerging managers: European waterfalls were designed for large, diversified institutional funds with decades of track record. They put GPs at a serious disadvantage when earlier deals outperform later ones. For a developer raising $10M-$50M on a deal-by-deal basis, the European waterfall is the wrong structure in almost every case.

{{main-cta}}

Side-by-Side Comparison

The bottom line: If you are a developer raising institutional capital on a deal-by-deal basis, push for the American waterfall. It is now acceptable to institutional LPs who are themselves shifting toward deal-by-deal structures. An advisor who does not push for this on your behalf is not protecting your economics.

The 3 Dilution Risks Developers Miss Until It Is Too Late

Most developers focus on the preferred return percentage when they review an LP agreement. That is not where the real dilution risk hides.

Dilution Risk 1: Compounding Preferred Returns

There are two types of preferred returns: cumulative and non-cumulative.

Non-cumulative preferred returns do not carry forward. If a distribution period misses the hurdle, unpaid preferred returns from that period simply lapse. This is far better for GP economics.

Cumulative preferred returns carry forward and compound. If the deal distributes less than the preferred return in year one, the shortfall rolls into year two's calculation. Over a four-year hold with uneven cash flows, as James Moore & Co's waterfall analysis demonstrates, compounding can add hundreds of thousands of dollars to what LPs receive before your promote kicks in.

What to negotiate: Push for non-cumulative preferred returns wherever possible. Many institutional LPs will accept this, particularly in deal-by-deal structures where they are evaluating each project individually.

Dilution Risk 2: Weak Hurdle Rate Design

A flat 20% promote sounds standard. But the hurdle rate that triggers it determines how much you actually earn.

A well-structured waterfall uses tiered promote levels rather than a single binary threshold. Industry data from Realty Capital Analytics shows that tiered structures are becoming the institutional standard:

- 0% promote below an 8% IRR

- 10% promote between 8-12% IRR

- 20% promote between 12-15% IRR

- 30% promote between 15-20% IRR

- 40% promote above 20% IRR

This structure rewards exceptional performance. It also gives LPs confidence that the GP is not earning promote on mediocre returns. And critically, it means a GP who delivers 18% IRR earns significantly more than one who delivers 12%. The tiered structure actually protects GP economics at the high end better than a flat 20% promote with a single 8% hurdle.

Dilution Risk 3: Clawback Provisions That Were Not Modeled

A clawback provision requires the GP to return previously paid promote if the deal or fund ultimately underperforms the agreed hurdle. For deal-by-deal structures, clawbacks are less common. For fund structures, they are standard.

The risk: Clawbacks are often written in ways that are difficult to model at signing. The calculation methodology, the time period, and the trigger conditions all matter. A clawback that kicks in at fund wind-down based on blended fund performance can require a GP to return promote earned on earlier outperforming deals if later deals underperform.

What to do: Before signing any LP agreement with a clawback provision, model at least three scenarios (base case, downside, extended hold). Know exactly what you owe back under each scenario. If your advisor cannot run this analysis, they are not the right advisor for a $10M+ raise.

This is why choosing an advisory firm that goes beyond introductions and actually architects your LP structure is one of the highest-leverage decisions a developer can make before going to market.

What to Look for in an Advisory Firm's Approach to Promote Protection

Not every advisory firm treats promote protection as part of their job. Most do not. Here is how to tell the difference before you sign an engagement.

Red flags that an advisory firm does not protect your economics:

- They ask you to bring a fully structured deal before they start introductions

- They do not ask about your preferred return terms or waterfall design

- Their compensation is a cash fee at close (no skin in the game)

- They cannot model your waterfall across multiple exit scenarios

- They have never reviewed an LP agreement on behalf of a client

Green flags that an advisory firm takes GP economics seriously:

- They structure the capital stack before going to market, not after

- They model the waterfall across at least three scenarios before any LP meetings

- They push back on compounding preferred returns and negotiate non-cumulative terms

- Their compensation is equity-based (they only win when you win)

- They review every LP agreement clause before you sign

The distinction matters most at the moment you are most vulnerable: when you are deep in a raise, capital is close, and you are tempted to sign whatever the LP puts in front of you. An equity-aligned advisor who has modeled your downside scenario will tell you when a term is unacceptable. A transactional placement agent who already earned their fee has no reason to.

Understanding how the capital stack for a development project is structured before LP negotiations begin is the single best preparation for protecting your promote in every deal you bring to market.

How IRC Partners Architects Promote Protection

IRC Partners structures the deal before going to market. This is not a tagline. It is the operational sequence that determines whether a developer's promote survives contact with institutional LP due diligence.

IRC Partners protect real estate developers from dilution.

The IRC process for promote protection:

- Waterfall design: IRC models the waterfall across base case, downside, and extended hold scenarios before the first LP meeting. Developers know exactly what they earn under each scenario before they negotiate.

- Preferred return structuring: IRC pushes for non-cumulative preferred returns wherever the LP relationship allows. The difference between cumulative and non-cumulative terms on a $20M raise over a four-year hold can be significant.

- Tiered promote architecture: IRC designs tiered promote structures that protect GP economics at high performance levels while giving institutional LPs the alignment signal they require.

- LP agreement review: IRC reviews every LP agreement provision before a developer signs. Clawback mechanics, distribution timing, and GP removal provisions are all flagged before close.

- Equity-aligned compensation: IRC takes 3-5% advisory equity. The firm only earns when the developer earns. That alignment means IRC has the same incentive to protect the promote as the developer does.

For developers who want to understand how equity preservation works across the full capital raise process, the promote protection work starts before the first LP meeting, not after.

Frequently Asked Questions

What does anti-dilution protection mean for real estate developers?

In real estate, anti-dilution refers to waterfall design, preferred return mechanics, and clawback provisions that safeguard the developer share of profits. It ensures that the upside is preserved across various performance scenarios, preventing the investor preference from eroding the profit split.

What is the difference between cumulative and non-cumulative preferred returns?

Cumulative preferred returns carry forward and compound if a distribution is missed, significantly increasing the amount investors must be paid before the developer sees a profit. Non-cumulative preferred returns lapse if unpaid in a given period. The latter is far superior for developer economics as it prevents the compounding effect that can drain deal profits.

Which waterfall structure is better for a developer promote?

The American or deal-by-deal waterfall is almost always better for developers. It allows the developer to receive their profit split as each individual deal closes. A European waterfall requires all investor capital across an entire fund to be returned before the developer receives any profit, which delays cash flow and increases financial risk.

What is a clawback provision in a real estate agreement?

A clawback provision requires the developer to return previously distributed profits if the overall deal or fund underperforms the agreed hurdle rate at the end of its life. This is common in fund structures where earlier wins might be taken back to cover later losses. Modeling these provisions across multiple exit scenarios is critical before signing.

What is a tiered promote structure and how does it protect economics?

A tiered structure increases the developer share of profits as the deal internal rate of return crosses specific milestones, such as jumping from a 20 percent split at a 12 percent return to a 30 percent split at an 18 percent return. This ensures developers capture a massive upside on high-performing deals while aligning with investors who only pay higher fees for exceptional results.

How does the advisor compensation model affect profit protection?

Transactional placement agents focused on cash fees may ignore toxic waterfall terms to close a deal quickly. Equity-aligned advisors earn only when you do, which incentivizes them to fight for non-cumulative returns, better hurdle rates, and limited clawback exposure to protect your long-term wealth.

Can developers negotiate waterfall terms with institutional investors?

Yes. In 2026, institutional family offices are increasingly flexible regarding deal-by-deal structures and American waterfalls. Developers have the most leverage to negotiate these terms when they have a verified track record and a partner who specializes in institutional-grade deal packaging to present the opportunity.

Continue reading this series:

- The Institutional Capital Playbook for Real Estate Developers: How to Raise $10M-$100M Without Giving Away Your Promote

- Which advisory firms offer comprehensive capital raising services for developers?

- Top firms for real estate capital raising without losing equity

IRC Partners advises founders raising $5M to $250M of institutional capital on structure, positioning, and round architecture. 7 strategic partners per quarter. No placement agent model. No success-only theater. If you want a structural review of your current raise, apply at HERE

Sponsors weighing this decision should first complete a capital raise readiness assessment for sponsors to confirm the raise is investor-ready.

Need guidance on your capital raise?

.jpg "The 7 non-negotiables that make or break your institutional raise")

The 7 Non-Negotiables That Make Or Break Your Institutional Raise

Avoid Broad Audit Rights Before Signing $10M+ Sponsor Investment Deals

Capital Raise Audit vs Pitch Deck Review: What Institutional Investors Actually Screen

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of seven

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.