.svg)

.png)

How Seasoned Real Estate Developers Access Institutional Allocators: The Warm Introduction Framework for $10M+ Raises

Seasoned real estate developers access institutional allocators for $10M+ raises through warm introductions from credible capital advisors, not through cold outreach or conference networking. Warm introductions convert at over 30% with institutional allocators. Cold outreach to the same allocators converts at less than 1%. The access gap is not a deal quality problem. It is an infrastructure problem.

The developers who consistently close $10M to $75M institutional raises share one structural advantage: a capital advisor with active, maintained relationships with the 13% of family offices that write $10M+ checks. Without that infrastructure, even a strong track record and a well-structured deal will not produce meetings.

Family offices now provide over 50% of deal-level capital in real estate, up from a historical 20%, according to Altss's February 2026 family office deal flow report. They are no longer minority co-investors filling out a syndicate. They are the price-setters, the governance-setters, and in many cases the majority equity provider. The capital is there. The appetite is real. But institutional allocators do not take inbound pitches from operators they have never heard of.

They operate on trust networks. And trust networks require warm introductions from credible intermediaries.

This is the framework IRC Partners uses to connect seasoned developers with the institutional allocators that write $10M+ checks. It covers why the access wall exists, what allocators actually evaluate before saying yes, and the exact four-layer system that gets $10M+ raises closed. If you are raising in the next 12 months and still relying on your HNWI network or cold outreach, this guide is the most important thing you will read before going to market. For context on how capital structure decisions affect your raise before any introduction is made, see our breakdown of what investors actually look for in a capital stack.

Why Most Developers Hit a Wall at $10M+

Most developers who hit a ceiling at $10M+ are not doing anything wrong. They are doing the right things in the wrong arena.

The HNWI network that funded your first three deals is built for check sizes of $500K to $3M. It is a relationship network, not an institutional capital network. Scaling into a $15M to $75M raise requires a completely different set of relationships, a different process, and a different access strategy. The two worlds do not overlap.

The Three Structural Barriers

1. You are targeting the wrong 87% of family offices.

Only 13% of family offices write checks of $10M or more per deal. The other 87% deploy $1M to $5M. Most developers do not know this. They spend 6 to 12 months pitching family offices that are structurally incapable of leading their raise, then conclude that the market is not there. The market is there. The targeting is wrong.

2. Cold outreach does not work at this level.

According to PwC's 2025 Global Family Office Deals Study, 69% of all family office investments are club deals, meaning they co-invest alongside other trusted parties. Family offices do not respond to unsolicited decks. They respond to referrals from people they already trust. If you are not inside that referral chain, you are invisible regardless of deal quality.

3. The fund structure shift has raised the bar.

Family office fund investments peaked at 2,871 transactions in H2 2021. By H1 2025, that number had collapsed to just 186, per PwC. Family offices are not writing fewer checks. They are writing them differently: deal-by-deal, with direct relationships to the operator, and with more due diligence on the GP than ever before. The blind pitch to a fund administrator is dead. Understanding the difference between family office deal-by-deal structures and blind pool commitments is now a prerequisite for going to market.

The real barrier is not capital availability. It is access infrastructure. Developers who solve the access problem close raises. Developers who do not, keep hitting the same wall.

These barriers are structural. They do not go away with a better deck or a lower preferred return. They go away when you have the right intermediary making the right introduction to the right allocator.

What Institutional Allocators Actually Look For Before Saying Yes

Most developers prepare for the meeting. The best-capitalized developers prepare for what happens before the meeting is even offered.

Institutional allocators make a preliminary judgment long before they open your deck. That judgment is based on who introduced you, how your deal is structured, and whether your track record presentation meets institutional standards. The pitch itself is almost secondary.

The Sponsor Comes Before the Deal

According to the JP Morgan 2026 Global Family Office Report, family offices targeting returns above 11% allocate over 40% of their portfolios to alternatives and have nearly double the exposure to direct control investments compared to lower-return-target offices. These are sophisticated allocators. They have seen hundreds of deal decks. What separates the operators they fund from the ones they pass on is not the deal. It is the GP.

Allocators evaluate the sponsor first. Your track record, your team, your prior LP relationships, and your reputation in the market are the pre-qualifiers. If those do not hold up, the deal does not get opened.

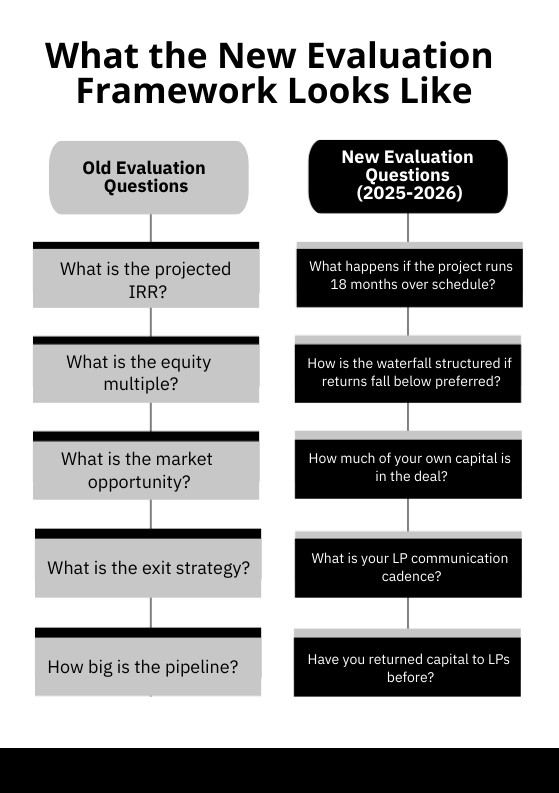

What the New Evaluation Framework Looks Like

The questions allocators ask have shifted. The old framework centered on projected returns. The new framework centers on downside protection and operator alignment.

This shift matters for how you structure your capital stack before going to market. Allocators want to see preferred return mechanics, co-investment alignment, and GP commitment. They want to know you have skin in the game. The question of whether to target a single-family office versus a multi-family office for your LP equity also affects which evaluation framework applies, since SFOs and MFOs have meaningfully different due diligence processes.

"The allocators we work with are not asking 'what's the return?' They are asking 'what happens if things don't go to plan?' Developers who can answer that question with precision get the meeting. Developers who cannot, get a polite pass." - IRC Partners

Real estate's share of total family office investment rebounded to 39% in H1 2025, its highest level since 2019, per PwC. The appetite is back. But the selectivity is higher than it has ever been.

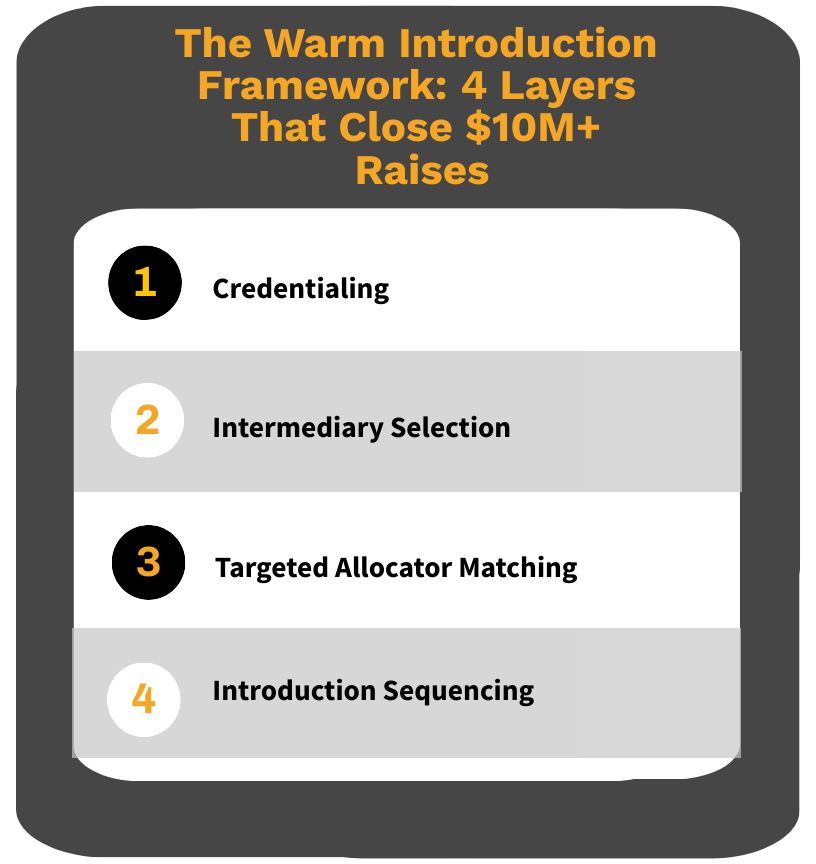

The Warm Introduction Framework: 4 Layers That Close $10M+ Raises

A warm introduction is not a referral. A referral is passive. A warm introduction is an active vouching from a credible party who has a relationship with both the developer and the allocator. That distinction matters because institutional allocators treat them differently.

Here is the four-layer framework IRC Partners uses to structure warm introductions for $10M+ real estate raises.

Layer 1: Credentialing

Before any introduction is made, the deal and the sponsor must be institutional-grade. This means more than a polished deck.

Credentialing covers three things:

- Capital stack structure. Waterfall mechanics, preferred return thresholds, co-investment alignment, and GP commitment must be explicit and defensible. An allocator's first question after a warm intro is often "can you send the deal summary?" If that summary does not reflect institutional-grade structuring, the introduction dies there.

- Track record presentation. A list of completed projects is not a track record. An institutional track record shows realized returns by project, LP communication history, timeline adherence, and exit execution. It is formatted for due diligence, not for marketing.

- Deal materials. The investment memo, financial model, and risk analysis must be built to withstand institutional scrutiny. Not because the allocator will read every line before the first meeting, but because their team will after it.

The rule: No introduction goes out before the materials are ready. Sending an unprepared deal through a warm channel burns the relationship with the allocator and the credibility of the intermediary.

Layer 2: Intermediary Selection

The quality of the introducer determines the quality of the response. An introduction from a trusted capital advisor with active allocator relationships produces a different outcome than an introduction from a mutual contact who knows someone at a family office.

Advisors with existing, maintained relationships with institutional allocators outperform cold referrals by a factor of 10 to 1. This is because the allocator's decision to take the meeting is based on their trust in the introducer, not their knowledge of the developer. The introducer's credibility is the first layer of diligence.

Layer 3: Targeted Allocator Matching

Not all family offices are the right fit. Matching requires more than identifying that a family office invests in real estate. It requires matching on:

- Check size. Target only the 13% of family offices that write $10M+ checks.

- Asset class preference. A family office with a track record in multifamily is a better first call than one that has never touched residential.

- Current deployment cycle. Family offices that just deployed a large allocation are in a different position than those with dry powder actively seeking deals.

- Structure preference. As covered in our analysis of family offices versus private equity funds as LP partners, the governance and timeline expectations of each allocator type differ significantly.

Targeting the wrong allocator with a warm introduction wastes the relationship. Targeting the right one closes the deal.

Layer 4: Introduction Sequencing

The introduction itself must be sequenced correctly. A generic "I'd like to introduce you to a developer" email is not a warm introduction. It is a forwarded cold pitch.

Effective introduction sequencing works like this:

- The intermediary previews the opportunity to the allocator before making the introduction, framing it against the allocator's known thesis and current deployment priorities.

- The developer receives a briefing on the allocator's specific interests before the first contact.

- The initial communication is a targeted deal summary, not a full deck, positioned to answer the allocator's pre-qualification questions before they have to ask them.

- The intermediary remains in the communication loop through the first meeting, reinforcing the vouching relationship.

The result: The allocator enters the first meeting already interested, already briefed, and already trusting the source. That is a fundamentally different starting point than a cold introduction.

According to IRC's own data, warm introductions structured this way convert at over 30%. Cold outreach to the same allocators converts at less than 1%. The framework is the difference.

The IRC Model: How Warm Introductions Get Structured at Scale

The four-layer framework above describes the process. IRC Partners is the infrastructure that executes it.

Most placement agents and capital brokers operate differently. They maintain a database of investor contacts, send your deck to a list, and charge a fee when someone bites. That is not a warm introduction. That is a managed cold outreach with a better-looking spreadsheet.

What IRC Does Differently

IRC's model is built around three structural differences from the traditional placement agent approach:

- Structure before raise. IRC architects the capital stack before going to market. Waterfall mechanics, preferred equity terms, and LP alignment are built to institutional standards before the first introduction is made. Allocators see a credentialed opportunity, not a raw pitch.

- Equity-aligned compensation. IRC takes 3 to 5% advisory equity in each engagement. This means IRC only wins when the developer wins. That alignment is itself a credibility signal to allocators, because they know the advisor has skin in the game alongside the GP.

- Active network, not a database. IRC maintains active relationships with over 307,000 institutional allocators, including family offices managing over $17 billion in assets that actively request deal referrals from IRC. The difference between an active relationship and a database entry is the difference between a warm introduction and a cold email with a contact name attached.

One Engagement, All Future Raises

One of the most common mistakes developers make is treating capital advisory as a transaction. They hire a broker for one raise, close the deal, and start from scratch on the next one.

IRC embeds as a permanent capital formation partner. One engagement covers all future raises through exit. The allocator relationships built during the first raise become the foundation for the second, third, and fourth. Over time, the developer's LP network grows, the raises get faster, and the terms improve because the relationships are already established.

This is how the best-capitalized developers operate. They do not raise deal by deal. They build a capital formation infrastructure that compounds across their entire development pipeline.

For a deeper look at how to evaluate which type of institutional LP is the right fit for your specific project, our guide to choosing between family offices and private equity funds for real estate LP equity walks through the structural differences in detail.

Case Study: How One Developer Broke Through to Institutional Capital

The following is an anonymized account of a real engagement. Details have been changed to protect confidentiality.

The Problem

A Southeast-based developer with five completed multifamily ground-up projects came to IRC with a $28M raise for a mixed-use development in a high-growth secondary market. He had a strong track record, a clean project history, and a deal that penciled well at multiple exit scenarios.

He had also spent eight months trying to raise capital. He had sent decks to dozens of family offices. He had attended three industry conferences. He had one LP commitment for $3M from an existing HNWI relationship.

The core problems were three:

- His capital stack was built for HNWI investors, not institutional LPs. The waterfall did not include a preferred return structure that institutional allocators recognize as standard. There was no GP co-investment commitment documented in the materials.

- His track record presentation was a project list with completion dates. It did not show realized LP returns, exit timelines, or LP communication history. It could not pass institutional due diligence.

- He had no warm access to family offices writing $10M+ checks. The contacts he had were either too small or too far removed from the right relationships to produce a credible introduction.

The IRC Intervention

IRC restructured the capital stack over six weeks. The waterfall was rebuilt with an 8% preferred return, a 70/30 LP/GP split to the preferred, and a promote structure that rewarded performance without front-loading GP economics. The track record was reformatted into an institutional presentation showing realized IRR by project, hold period, and LP distribution history.

With the materials institutional-grade, IRC coordinated warm introductions to seven targeted family offices from its allocator network, each matched on check size, asset class preference, and current deployment cycle.

The Result

$22 million in institutional LP equity committed within six months. Two family offices co-invested, structuring it as a club deal, which is exactly how 69% of family office real estate investments are structured per PwC's 2025 data.

The same two family offices are now in active conversation for the developer's next project. The first raise built the relationship. The second raise will be faster, on better terms, and with allocators who already know the GP.

That is what a capital formation infrastructure looks like when it compounds. As our piece on what actually works when pitching institutional investors makes clear, the mechanics of credibility transfer the same way across asset classes: the introducer's trust is the first layer of diligence.

What Developers Should Do Next

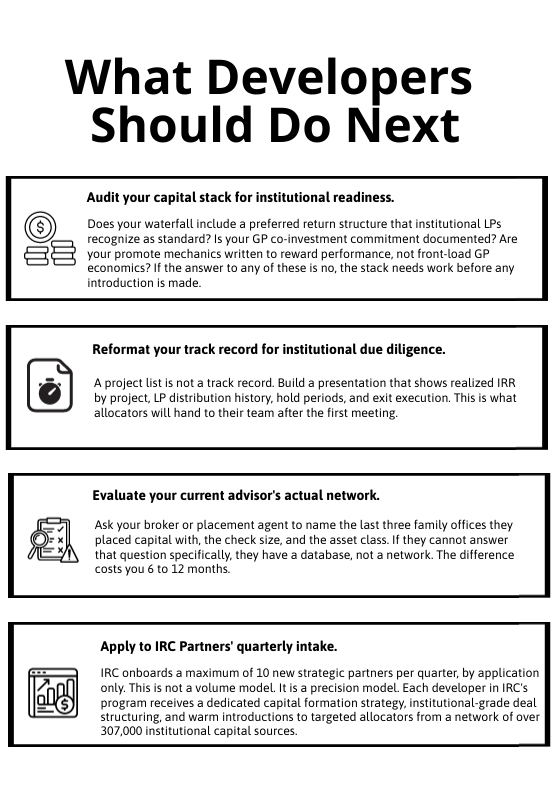

If you are raising $10M or more in the next 12 months, here are the four steps to take before going to market.

- Audit your capital stack for institutional readiness. Does your waterfall include a preferred return structure that institutional LPs recognize as standard? Is your GP co-investment commitment documented? Are your promote mechanics written to reward performance, not front-load GP economics? If the answer to any of these is no, the stack needs work before any introduction is made.

- Reformat your track record for institutional due diligence. A project list is not a track record. Build a presentation that shows realized IRR by project, LP distribution history, hold periods, and exit execution. This is what allocators will hand to their team after the first meeting.

- Evaluate your current advisor's actual network. Ask your broker or placement agent to name the last three family offices they placed capital with, the check size, and the asset class. If they cannot answer that question specifically, they have a database, not a network. The difference costs you 6 to 12 months.

- Apply to IRC Partners' quarterly intake. IRC onboards a maximum of 10 new strategic partners per quarter, by application only. This is not a volume model. It is a precision model. Each developer in IRC's program receives a dedicated capital formation strategy, institutional-grade deal structuring, and warm introductions to targeted allocators from a network of over 307,000 institutional capital sources.

The capital exists. The family office appetite for real estate is at its highest point since 2019. The developers who access it are not the ones with the best deals. They are the ones with the right infrastructure around their deals.

IRC Partners accepts applications on a rolling basis. Quarterly intake is limited. Apply to work with IRC Partners to start the conversation.

Frequently Asked Questions

What is a warm introduction in real estate capital raising?

A warm introduction is an active vouching from a credible intermediary who has existing relationships with both the developer and the institutional allocator. It is not a simple referral; the introducer frames the opportunity against the allocator known thesis before making contact. Warm introductions convert at over 30 percent with institutional partners, compared to less than 1 percent for cold outreach.

How do I access family offices for a raise over 10M dollars?

Access to family offices at this level requires a capital advisor with live relationships, as only about 13 percent of family offices write checks of 10M dollars or more. Targeting smaller offices often leads to months of wasted effort. The advisor relationship acts as the first layer of due diligence, signaling that the deal is institutional-grade.

What do institutional allocators look for in a developer?

Allocators evaluate the sponsor institutional credibility first. This includes a track record showing realized internal rates of return and exit execution, standard preferred return mechanics, and documented developer co-investment. They prioritize sponsors who can answer rigorous downside protection questions rather than just presenting optimistic return projections.

How long does a 10M dollar plus real estate raise typically take?

With institutional-grade materials and warm access, a raise of this size typically takes four to eight months to close. Without proper preparation—which usually takes four to eight weeks—developers often spend 12 to 18 months in unproductive outreach that fails to gain traction with major funds.

Why do family offices prefer deal-by-deal structures over blind pool funds?

Family offices increasingly favor deal-by-deal participation because it offers direct governance input, better economics, and total transparency. Blind pool funds require a level of trust that is harder to monitor, leading to a massive shift toward club deals and direct investments where the office can evaluate each specific asset.

What asset classes are family offices most interested in for 2026?

Multifamily and Industrial remain the top conviction sectors. Data centers are the fastest-growing allocation category due to high demand for digital infrastructure. In 2026, real estate share of family office investment has rebounded to near-record highs, driven by a preference for tangible assets with resilient cash flows.

Can a developer with only HNWI experience qualify for institutional capital?

Yes. The primary requirement is not the source of previous capital, but a strong execution track record and professional management of past investor relationships. By restructuring materials for institutional review and standardizing the capital stack with professional waterfall mechanics, developers can successfully transition to institutional funding.

IRC Partners advises founders raising $5M to $250M of institutional capital on structure, positioning, and round architecture. 7 strategic partners per quarter. No placement agent model. No success-only theater. If you want a structural review of your current raise, apply at HERE

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.