.svg)

.png)

Family Offices vs. Private Equity Funds: Which Institutional LP Is Right for Your Development?

For seasoned real estate developers raising $10M or more, the choice between a family office and a private equity fund comes down to four variables: required check size, deal timeline, governance tolerance, and return profile. This guide compares both LP types across eight decision factors so you can identify the right fit for your specific development before you start outreach - and avoid the months of mismatched diligence that comes from targeting the wrong one.

Neither LP type is universally superior. The right one depends entirely on how the deal is structured and what the GP can operationally support. Choosing the wrong LP type does not just slow down a raise. It wastes months in mismatched diligence, burns allocator relationships, and can force the GP to give up economics to close a deal that was never a real fit.

According to the McKinsey Global Private Markets Report 2026, real estate returns in this cycle are being driven by execution, capital structure discipline, and platform scale. That means the LP relationship is not a formality. It is a structural variable that shapes whether a deal closes on time, on terms, and with the right economics intact.

This is Spoke 4 of IRC Partners' institutional allocator series. The full warm introduction framework for $10M+ raises covers how experienced developers access institutional capital at scale. This article goes deeper on one specific decision: whether a family office or a private equity fund is the right LP for your development, and how to make that call before you start outreach.

This guide covers:

- When family offices are the better institutional LP and what they actually screen for

- When private equity funds are the stronger fit and what they will pressure-test

- A side-by-side comparison across eight decision factors every developer should evaluate before going to market

Quick Answer: Family Office or PE Fund?

The short answer is that neither LP type is universally better. The right choice depends on your deal's required check size, timeline, capital stack structure, and how much institutional governance you can absorb. According to the Goldman Sachs 2025 Family Office Investment Insights Report, 44% of surveyed family offices now invest primarily in private real estate, and U.S. family offices raised real estate allocations from 10% in 2023 to 18% in 2024. Capital is available from both LP types. The question is fit.

Key takeaway: If your deal needs flexibility, a relationship-led diligence process, and a longer hold runway, a family office is likely the better starting point. If your deal is larger, tightly underwritten, and you can support formal quarterly reporting, a PE fund may be the stronger fit.

What Family Offices Want from a Real Estate Developer

Family offices are not passive checkwriters. They have become increasingly active, direct, and selective in how they deploy capital into real estate. According to the PwC Global Family Office Deals Study 2025, family offices have shifted decisively away from fund commitments toward direct investments, with direct and co-investment strategies now representing the majority of how family capital enters private markets.

That shift has a direct implication for developers: family offices want to understand the deal at an asset level, not just as a line item in a portfolio. They are not trying to beat a quarterly benchmark. They are trying to preserve and grow multigenerational wealth, which changes what they screen for.

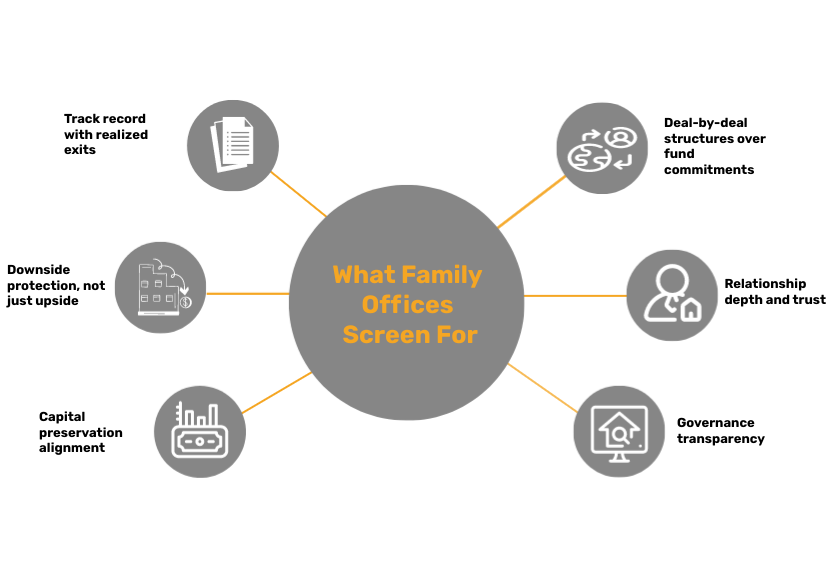

What Family Offices Screen For

- Track record with realized exits. A developer with three or more completed projects and documented returns carries far more weight than one with a compelling pipeline narrative. Family offices are not early adopters of unproven operators.

- Downside protection, not just upside. Family offices increasingly ask "what happens if things do not go to plan?" before they ask about projected IRR. Clear downside scenarios, conservative underwriting, and defined loss-mitigation strategies are not optional.

- Capital preservation alignment. Because family offices target return profiles in the 7% to 12% range (per J.P. Morgan's 2026 Family Office Report), they are not chasing the same return profile as PE funds. Developers who pitch 30% IRR projections without grounding them in realistic assumptions often lose credibility faster than they gain interest.

- Deal-by-deal structures over fund commitments. Research from Morningstar notes that families increasingly view deals as opportunities to make money rather than funds as vehicles associated with fees and lock-ups. If a developer is raising for a specific project, that is often more appealing to a family office than a blind pool ask.

- Relationship depth and trust. Family offices deploy capital through people they trust. A cold outreach with a pitch deck rarely closes a family office. A warm introduction from a credible intermediary, a shared connection, or a co-investment track record with a known contact is how most family office relationships start.

- Governance transparency. According to IQ-EQ's 2026 family office research, family offices are formalizing their own governance structures and expect the same clarity from the operators they back. Developers who can show clean waterfall mechanics, clear GP/LP rights, and a defined reporting cadence are more likely to pass initial screening.

"Family offices benefit from direct and co-investment opportunities that offer control, closer alignment with long-term objectives, and the ability to capture bespoke deals that traditional fund structures may miss." — IQ-EQ, 2026 Key Predictions for Family Offices

Understanding how family offices differ from each other is also important. A single-family office managing $900M in assets behaves very differently from a multi-family office platform. For a deeper breakdown of how to target the right family office type for your raise, see single-family office vs. multi-family office for real estate LP equity.

What Private Equity Funds Want from a Real Estate Developer

Private equity funds are not harder to work with than family offices. They are just different in what they require, and those requirements are non-negotiable. A PE fund's capital comes with a formal structure built around a defined investment mandate, a fixed fund cycle, and an investment committee that applies consistent underwriting criteria across every deal they review.

For developers, that means the bar for entry is clear but demanding. According to the McKinsey Global Private Markets Report 2026, private equity in 2026 is a mature industry where outcomes are shaped by disciplined asset selection, operational value creation, and rigorous risk management. PE funds are not looking for compelling stories. They are looking for deals that fit their box.

What PE Funds Will Pressure-Test

- Return profile and IRR underwriting. Most real estate PE funds target IRR in the 15% to 25% range. If your deal does not support that return at their required entry terms, it will not clear the investment committee regardless of how strong the relationship is.

- Defined hold period and exit strategy. PE funds operate on fixed fund cycles, typically five to ten years. They need a credible exit path within that window. Open-ended holds, stabilization timelines that stretch beyond the fund's life, or exit strategies that depend on market timing will create friction.

- Formal governance and reporting cadence. PE funds expect quarterly reporting, audited financials, defined GP/LP rights, and structured waterfall mechanics. Developers who have not operated with institutional-grade reporting before will feel the difference immediately.

- Sponsor creditworthiness and co-investment. Most PE funds want the GP to have meaningful skin in the game. They will review the developer's balance sheet, prior deal performance, and co-investment capacity as part of standard diligence.

- Market and asset class fit. PE funds have defined mandates. A fund focused on multifamily ground-up will not flex into industrial or mixed-use just because the deal is strong. Developers need to confirm mandate alignment before spending time in diligence.

- Scalability signals. PE funds are not just investing in one deal. They are evaluating whether this developer is a long-term partner for the fund's deployment strategy. Developers with a clear pipeline, a capable team, and a repeatable process are far more attractive than one-deal sponsors.

Key insight: PE funds are often the right LP when the developer has already built institutional-grade operations and is ready to support a formal LP relationship across multiple projects, not just one raise.

Where PE funds fall short for some developers is on flexibility. If a deal requires staged capital calls tied to entitlement milestones, a longer-than-expected hold due to market conditions, or waterfall adjustments mid-project, PE funds have less room to accommodate those changes than a family office would.

Family Offices vs. PE Funds Across 8 Decision Factors

This is the framework most developers need before they start allocator outreach. Each factor below reflects a real decision variable that affects whether a deal closes, how long it takes, and what the GP gives up to get it done.

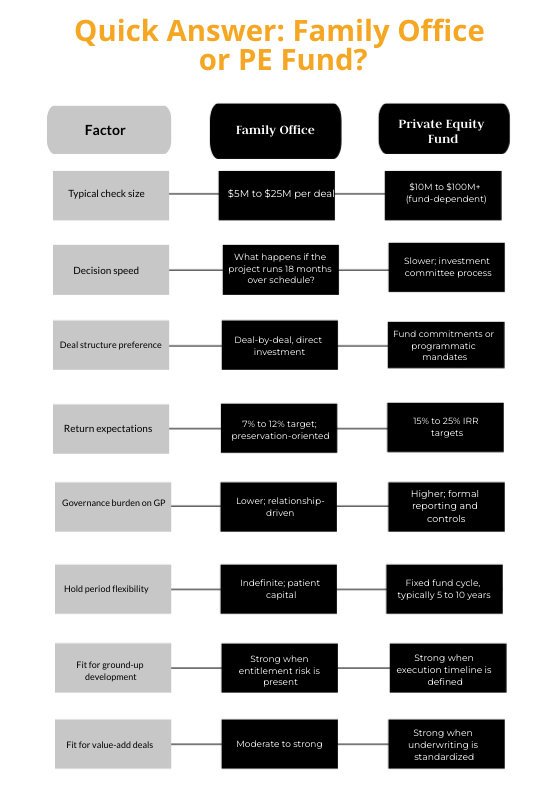

1. Check Size

Family offices typically write checks in the $5M to $25M range per deal, according to research compiled by IQ-EQ. That range fits many $15M to $75M development raises well, especially when a developer is syndicating across two or three family offices to fill a capital stack. PE funds can write larger single checks, often $10M to $100M or more depending on fund size, but they also come with more conditions attached to that capital.

What this means for you: If your raise requires a single anchor LP at $30M or more, a PE fund is often the more practical path. If you can fill the capital stack with multiple $10M to $20M checks, family offices give you more flexibility on terms.

2. Decision Speed

Family offices can move faster than PE funds when the relationship is in place. Many family offices have one or two decision-makers who can approve a deal without a formal investment committee process. PE funds almost always require an investment committee review, which adds weeks to the timeline.

What this means for you: If you have a time-sensitive closing or a deal with a hard contract deadline, a family office with a warm relationship can close faster. Cold outreach to either LP type will be slow regardless of structure.

3. Governance and Control Rights

PE funds typically require stronger governance rights: board observer seats, approvalinstitutional allocators warm introduction framework for $10M+ raises rights on major decisions, and defined GP removal triggers. Family offices vary widely, but many prefer a lighter governance footprint, especially when investing through a deal-by-deal structure rather than a fund commitment. For more on how family offices approach deal-by-deal structures specifically, see family office deal-by-deal vs. blind pool: what real estate developers need to know.

What this means for you: If preserving operational control is a priority, a family office is usually the lower-friction path. If you can absorb governance oversight in exchange for larger capital, a PE fund may be worth it.

4. Reporting Burden

PE funds require formal quarterly reporting, audited annual financials, and structured LP communications. Family offices typically require less, though the more institutionalized family offices are raising their expectations. Either way, developers who do not have a reporting infrastructure in place before going to market will lose credibility with both LP types.

What this means for you: Build your reporting infrastructure before outreach, not after. It signals institutional readiness regardless of which LP type you are targeting.

5. Return Expectations

This is one of the sharpest differences between the two. PE funds typically target IRR in the 15% to 25% range. Family offices, according to J.P. Morgan's 2026 Family Office Report, often target 7% to 12% returns with a stronger emphasis on capital preservation. That gap has a direct impact on how the waterfall is structured and how much of the deal economics the GP retains.

What this means for you: A lower return hurdle from a family office often means better GP economics on the promote. A PE fund's higher IRR target may require a more aggressive promote structure that reduces GP upside.

6. Hold Period Flexibility

Family offices can hold assets indefinitely. They are not constrained by a fund's lifecycle. PE funds must exit within their fund's term, which creates pressure to sell or recapitalize at a fixed point in time regardless of market conditions.

What this means for you: If your deal has any timeline uncertainty, whether from entitlement risk, construction delays, or lease-up variability, a family office is a more forgiving partner. A PE fund will enforce the exit timeline.

7. Downside Protection Requirements

Both LP types care about downside, but they express it differently. Family offices tend to focus on structural protections: preferred returns, loss of capital scenarios, and GP alignment through co-investment. PE funds add operational controls, covenant packages, and sometimes preferred equity structures with hard return floors.

What this means for you: Prepare a clear downside scenario analysis for any institutional LP conversation. Family offices want to see it in plain language. PE funds want to see it modeled with sensitivity tables.

8. Structure Fit for Real Estate Development

Family offices are generally more comfortable with deal-by-deal structures, joint ventures, and co-investment arrangements. PE funds are more comfortable with programmatic mandates, separate accounts, and fund structures where they have defined rights across multiple assets.

What this means for you: Match your offering structure to the LP's preferred format before outreach. Presenting a deal-by-deal JV to a PE fund that only does programmatic mandates is a fast path to a no.

Which LP Type Fits Ground-Up Development vs. Value-Add Deals?

The LP type question does not exist in a vacuum. It is always tied to a specific deal, a specific asset class, and a specific capital need. Here is how the comparison plays out across the two most common development scenarios.

Scenario 1: Ground-Up Development

Ground-up projects carry more risk variables than value-add deals. Entitlement timelines can shift. Construction costs can escalate. Lease-up projections can miss. These are not hypothetical risks; they are operational realities for any developer working on a multifamily, mixed-use, or industrial ground-up project.

Family offices are generally better suited for ground-up development because:

- Their patient capital model accommodates longer holds without fund-cycle pressure

- They can adjust to staged capital calls tied to construction milestones rather than requiring a single upfront commitment

- Their relationship-based diligence process allows the developer to explain deal-specific risks in context rather than fitting them into a rigid underwriting template

- Many family offices, especially those with real estate operating backgrounds, understand entitlement and construction risk at a practical level

PE funds can work for ground-up development, but only when the timeline is clearly defined, the entitlement risk is already resolved, and the developer can present a construction-to-stabilization schedule that fits within the fund's lifecycle.

Scenario 2: Value-Add Deals

Value-add strategies with defined renovation scopes, clear stabilization timelines, and predictable exit comps are a stronger fit for PE funds. The underwriting is cleaner, the hold period is more predictable, and the return profile is easier to model at a PE fund's IRR target.

Family offices can also be strong partners for value-add deals, especially for multifamily or industrial assets where institutional LP demand is high. According to the UBS Global Family Office Report 2025, U.S. family offices raised real estate allocations from 10% to 18% of portfolio between 2023 and 2024, with a significant portion directed toward income-producing and value-add strategies.

2026 asset classes with the strongest institutional LP demand:

- Multifamily ground-up and value-add (broadest LP interest from both FOs and PE)

- Industrial and logistics (high institutional conviction across both LP types)

- Data centers (fastest-growing allocation category, primarily PE and institutional FOs)

- Mixed-use with residential component (strong FO interest; PE varies by mandate)

- Life sciences and specialized CRE (niche; requires targeted LP matching)

How to Choose Before You Start Outreach

The biggest mistake developers make is treating allocator outreach as a volume exercise. They send the same pitch to every capital source they can find and wait to see who responds. That approach wastes months, burns relationships, and signals to institutional LPs that the developer does not understand the market.

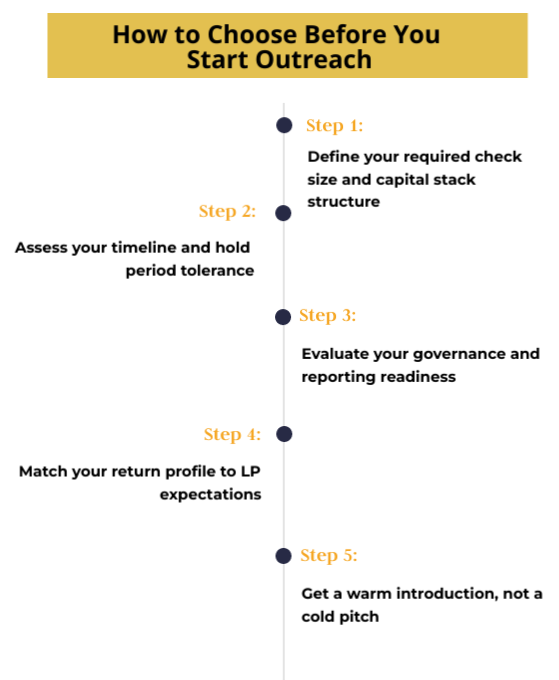

The right process starts with the deal, not the LP list. Here is a five-step pre-outreach framework for developers raising $10M or more in institutional LP equity.

Step 1: Define your required check size and capital stack structure. How much equity do you need, and in what form? A single $25M equity check from one LP requires a different target than three $8M to $10M checks from multiple family offices. Know your capital stack before you build your LP list.

Step 2: Assess your timeline and hold period tolerance. Does your deal have entitlement risk, construction variability, or lease-up uncertainty? If yes, you need an LP who can accommodate a flexible timeline. That points toward family offices. If your deal has a clean 36-month execution path to exit, a PE fund is more viable.

Step 3: Evaluate your governance and reporting readiness. Can your firm support quarterly institutional reporting, audited financials, and formal LP communications today? If not, a PE fund relationship will expose that gap immediately. Family offices are more forgiving, but the best ones still expect professionalism.

Step 4: Match your return profile to LP expectations. If your deal underwrites to a 12% to 15% net return to LP, a family office is likely the better fit. If your deal supports 18% to 22% net IRR with a defined exit, a PE fund becomes a realistic target. Mismatching return expectations is one of the most common reasons institutional conversations stall.

Step 5: Get a warm introduction, not a cold pitch. Both LP types are selective. But they filter trust differently. A PE fund evaluates the deal first and the relationship second. A family office often evaluates the relationship first and the deal second. That means warm introductions are even more valuable when targeting family offices, and they still matter significantly for PE fund access.

As covered in 10 mistakes that kill your first institutional raise, going to market without the right structure and the right access path is one of the most common and most costly errors developers make in their first institutional raise.

Structure the deal first. Then match the LP type to the deal. Then seek introductions to the allocators most likely to say yes on terms you can live with.

Final Verdict: Target the Allocator That Fits the Deal, Not the Logo

The most sophisticated developers in 2026 are not asking which LP type is better in the abstract. They are asking which LP type fits this deal, at this stage, with this capital stack. The answer changes from project to project.

When to lead with a family office:

- Your deal is ground-up with entitlement or construction timeline risk

- You need staged capital calls rather than a single upfront commitment

- You want to preserve operational control and limit governance overhead

- Your deal underwrites to a 7% to 12% net return to LP

- You are raising for a specific project rather than a fund commitment

- You are building a long-term LP relationship that can grow across multiple deals

When to lead with a PE fund:

- Your raise requires a single anchor check of $30M or more

- Your deal has a clean, defined execution timeline and exit strategy

- You can support formal quarterly reporting and institutional governance

- Your deal underwrites to a 15% to 25% IRR at the fund's required entry terms

- You are ready to operate under a programmatic or mandate-based LP structure

The most durable capital strategies are not built on one LP type. They are built on a clear understanding of which allocator fits which deal, and a network of warm relationships with both family offices and PE funds across different parts of the capital stack.

For developers who are ready to build that kind of institutional capital strategy, the next step is understanding how to access allocators at scale. The institutional allocators warm introduction framework for $10M+ raises covers the full access model.

IRC Partners works with seasoned developers to structure institutional-grade capital stacks and coordinate warm introductions to the right allocator type for each deal. If you are preparing for a $10M+ institutional raise, connect with IRC Partners to start with structure before outreach.

Frequently Asked Questions

What is the difference between a family office and a private equity fund?

A family office manages the wealth of a single family or small group, typically offering patient capital and flexible terms. A private equity fund pools capital from multiple institutions and operates under a fixed mandate with strict return targets and hold periods. Developers usually notice the difference in decision speed, governance burden, and return expectations.

How much do family offices typically invest in a single deal?

Most family offices write checks in the 5M dollar to 25M dollar range. Larger single-family offices with over 500M dollars in assets can invest more, but developers requiring 30M dollars or more from a single partner typically need to target private equity funds or aggregate commitments from multiple family offices.

Do private equity funds move faster than family offices?

Generally, no. Family offices often move faster—provided a warm relationship exists—because they usually have fewer decision-makers. Private equity funds require a formal investment committee review and extensive third-party due diligence, which can add four to eight weeks to the closing timeline.

What return do family offices expect from real estate investments?

Family offices generally target 7 percent to 12 percent net returns, prioritizing capital preservation. This is typically lower than the 15 percent to 25 percent internal rate of return targets common in private equity funds, often allowing for better developer profit split economics when working with a family office.

Are family offices or private equity funds better for ground-up development?

Family offices are usually better suited for ground-up projects due to their patient capital model, which accommodates longer holds and timeline variability. Private equity funds typically only enter ground-up deals once entitlement risks are resolved and the project timeline fits within their specific fund lifecycle.

What reporting do private equity funds require from developers?

Private equity funds require institutional-grade infrastructure, including standardized quarterly reporting, audited annual financials, and formal partner communications. Developers must have these accounting and management systems in place before approaching large-scale institutional allocators.

How do I know if my deal is ready for institutional partner outreach?

A deal is ready when it features a finalized capital stack, institutional-grade underwriting, and a credible downside scenario analysis. You must also have a documented track record of completed projects. Premature outreach with unfinished materials can permanently damage your credibility with these allocators.

The wrong structure doesn't just cost you this round. It costs you the next three. IRC Partners advises founders raising $5M to $250M of institutional capital. If you're about to go to market and want the structure reviewed before investors see it, book a call here

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.