.svg)

.png)

Single-Family Office vs. Multi-Family Office for Real Estate LP Equity: Which to Target in 2026

Single-Family Office vs. Multi-Family Office for Real Estate LP Equity: Which to Target in 2026

For real estate developers raising $10M or more in LP equity, the right family office target depends on five factors: check size, asset class, relationship path, governance expectations, and deal structure. Multi-family offices (MFOs) are the better starting point for most developers entering institutional capital for the first time, because they offer broader access, structured intake processes, and co-investment pathways across multiple families. Single-family offices (SFOs) are the better target when a developer already has a warm introduction, needs a concentrated check from one relationship, or is bringing a specialized deal that fits one family's specific mandate.

Neither structure is universally better. Pitching the wrong type costs developers three to six months of follow-up cycles that go nowhere. According to the PwC Family Office Deals Study, real estate rebounded to 39% of total family office investment share in the first half of 2025, its highest level since 2019. The capital is available. What changed is how selective and structure-driven the access has become.

If you are raising $10M or more and want to understand how institutional allocators evaluate deals before the first meeting, the warm introduction framework for real estate developers covers the full process. This article focuses on one specific decision inside that process: which type of family office to target, and why the answer is different for every raise.

This article focuses on one specific decision inside that process: whether to target a single-family office (SFO) or a multi-family office (MFO) for your LP equity raise.

The answer is not the same for every developer or every deal. It depends on five factors:

- The check size your raise actually needs

- The asset class you are bringing to market

- The relationship path you have available

- The governance and diligence style the office uses

- The deal structure you are offering

This article walks through each one so you can make the right call before you spend time on outreach.

Single-Family Office vs. Multi-Family Office: The Fast Definition Real Estate Sponsors Actually Need

Most definitions of these two structures are written for wealthy families deciding how to manage their own wealth. That is not your situation. You are a real estate principal deciding who to approach for LP equity. Here is what each structure actually means from your side of the table.

A single-family office (SFO) is a private entity that manages the wealth of one ultra-high-net-worth family. It operates with a high degree of customization. The investment mandate, risk tolerance, and decision process are set entirely by that family. SFOs typically require at least $100M to $250M in assets under management to justify the overhead of running a dedicated operation. Every investment decision reflects one family's priorities.

A multi-family office (MFO) serves multiple wealthy families through a shared platform. It pools infrastructure, investment expertise, and deal access across its client base. MFOs tend to have more structured investment processes, professional investment committees, and broader access to deal flow. They often serve families with $25M to $100M in assets, though many serve clients well above that range.

From a developer's perspective, the most important differences are not about cost or governance for the family. They are about how each type sources deals, makes decisions, and writes checks.

The critical takeaway: neither structure is universally better for raising real estate LP equity. The right one depends on how your raise is sized, how it is structured, and what kind of relationship you can bring to the first conversation.

What Changed in 2026: Why Family Office Targeting Got More Precise

Family offices did not stop investing in real estate. They changed how they invest in it. That shift has direct consequences for how developers should approach outreach.

Here are the four trends that matter most for a developer raising $10M+ in LP equity right now.

1. Real estate allocations are back up, but the bar is higher.

After dipping as low as 26% of family office investment portfolios in 2023, real estate's share rebounded to 39% by the first half of 2025, according to the PwC Family Office Deals Study. That is a meaningful recovery. But the capital is being deployed more carefully. Longer diligence cycles, sharper focus on downside scenarios, and a strong preference for operators with proven track records are now standard. The first question from most family offices is no longer "what is the return?" It is "what happens if things do not go to plan, and how is the deal structured to protect us?"

2. Club deals dominate, and that changes how you think about check size.

According to the same PwC study, 69% of family office investments in H1 2025 were club deals, meaning multiple investors participating in the same transaction. This matters for developers. It means the question is often not which single family office will write the whole check. It is which type of family office is the right lead or anchor, and which ones will co-invest alongside them.

3. Direct and deal-by-deal structures are replacing blind pool commitments.

Family offices have moved decisively away from blind pool fund vehicles. They want to know exactly what asset they are investing in, who is running it, and how decisions get made. This benefits developers who bring specific, well-structured deals rather than asking for a broad mandate commitment.

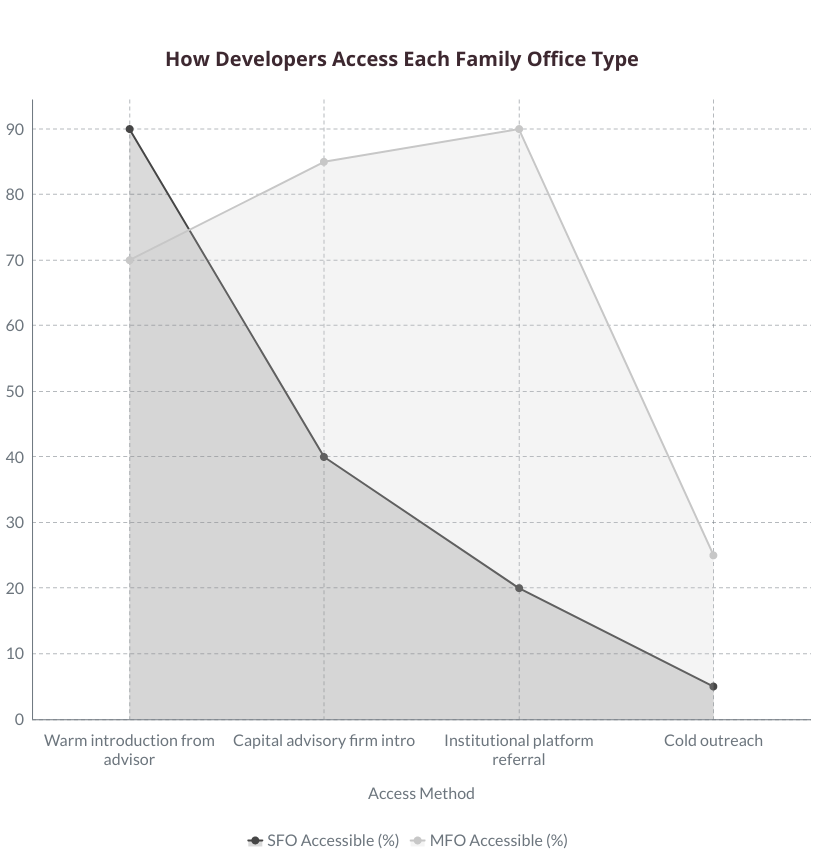

4. Relationship-sourced deals get through the door. Cold outreach rarely does.

Family offices receive far more deal inquiries than they can evaluate. The ones that get serious attention are almost always referred by a trusted advisor, co-investor, or known intermediary. Volume outreach to a list of family offices produces very little. A single warm introduction from the right source produces a real conversation.

The bottom line: Family office capital is available for real estate. But access has become more relationship-dependent, more structure-sensitive, and more precise than it was three years ago. Developers who understand which type of office fits their deal before they start outreach will move faster and waste less time.

When a Single-Family Office Is the Better Target

A single-family office can be the right LP target. But the conditions that make it the right choice are specific. Developers who go after SFOs without meeting those conditions usually end up in extended conversations that never convert.

What makes an SFO a strong fit

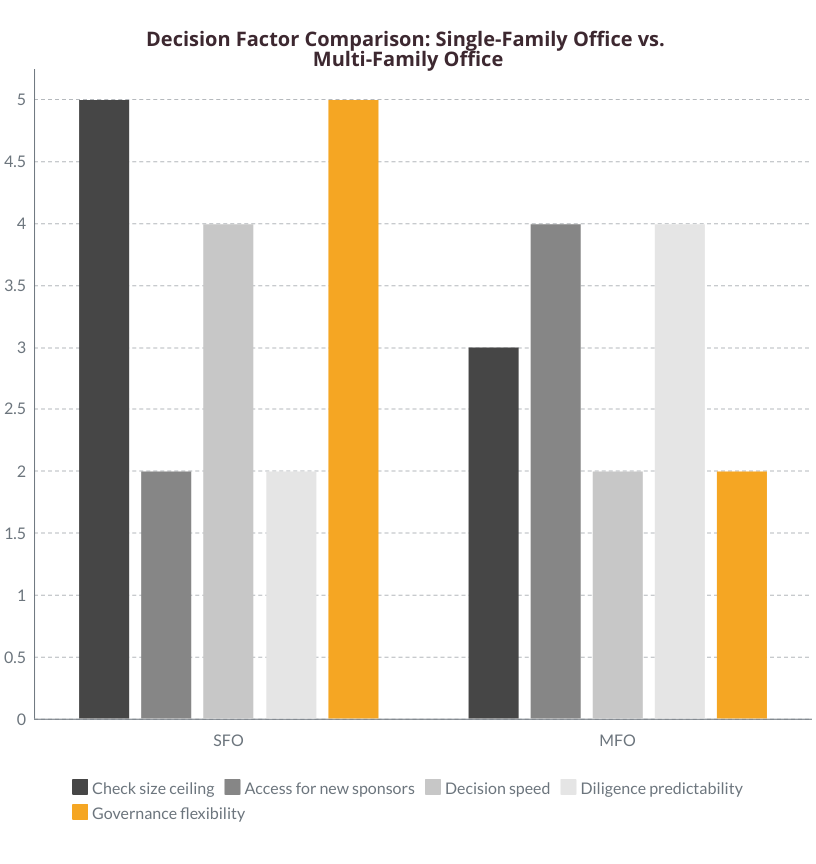

SFOs are built for one family's priorities. That means they can move in ways that institutional platforms cannot. They can make a decision in two meetings if the principals are engaged. They can structure a deal in a way that reflects the family's specific tax situation, timeline, or legacy goals. And they can offer a level of discretion that a multi-family platform simply cannot match.

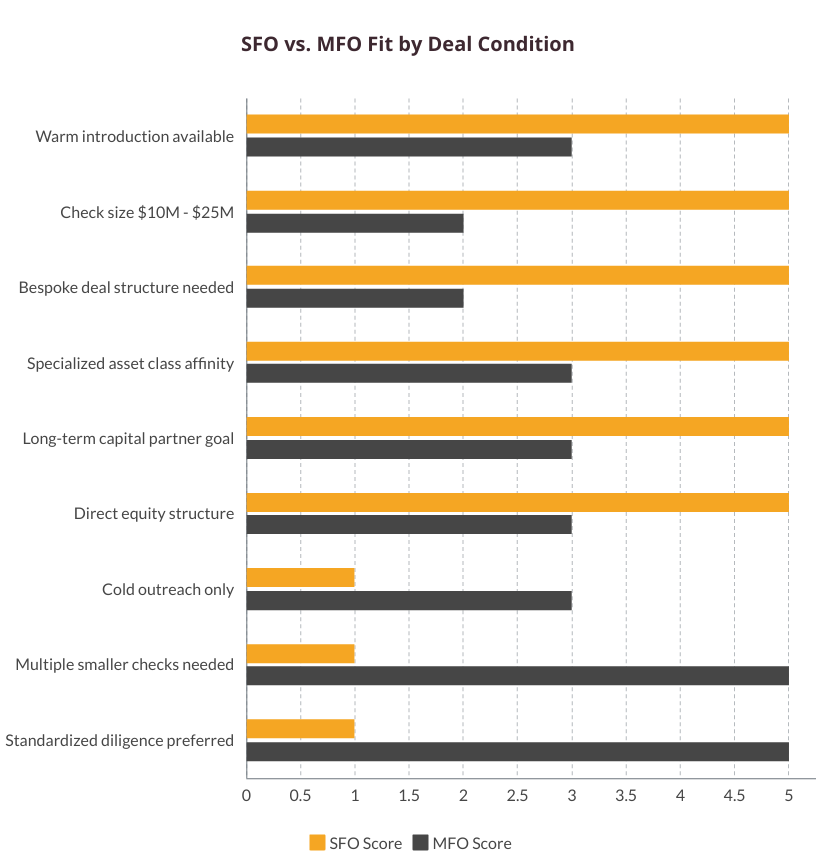

An SFO is likely the better target when:

- You already have a warm introduction to the family or their CIO through a trusted intermediary

- Your raise is sized for a concentrated check in the $10M to $25M range from a single source

- The deal requires a bespoke conversation about risk, structure, or timing rather than a standardized diligence process

- You are working on a specialized asset class where one family has a known affinity or operating background

- You want a long-term capital partner, not just a one-time LP, and are willing to invest in the relationship over time

- Your deal is structured as a direct equity or deal-by-deal investment rather than a fund commitment

Where SFOs fall short for most developers

The access problem is real. Most SFOs do not accept cold outreach. They do not publish contact information. They do not attend public investor conferences looking for new deals. Their deal flow comes almost entirely from trusted advisors, co-investors, and existing relationships.

This means the SFO path is only realistic if:

- You have a credible intermediary who can make the introduction

- You are willing to invest six to eighteen months building the relationship before capital commits

- Your deal track record and capital stack are already institutional-grade before the first meeting

Understanding how deal-by-deal structures work is also important before approaching SFOs, since most prefer to evaluate each asset individually rather than commit to a broader mandate. The distinction between deal-by-deal and blind pool structures is covered in detail in the family office deal-by-deal vs. blind pool guide for developers who want to go deeper on that topic.

Key takeaway: SFOs offer high-conviction, bespoke capital for the right deal. But the access path is narrow. If you do not already have a warm introduction, the MFO route is usually the more productive starting point.

When a Multi-Family Office Is the Better Target

For most developers who are making their first serious push into family office capital, a multi-family office is the more practical starting point. MFOs offer broader access, a more repeatable process, and a lower barrier to the first real conversation.

What makes an MFO a strong fit

MFOs run structured deal review processes. They have investment committees, defined mandates, and professional teams that evaluate opportunities across asset classes. That structure can feel slower, but it also means there is a defined path from introduction to decision. You know what they need. You know who reviews it. You know what the next step looks like.

An MFO is likely the better target when:

- You are entering family office capital for the first time and need to build a track record with institutional LPs

- Your raise benefits from co-investment pathways, where multiple family clients participate in the same deal

- Your deal is in a mainstream asset class with strong institutional appetite, such as multifamily residential or industrial

- You need a repeatable process you can run across multiple deals, not a one-time bespoke relationship

- Your raise is structured to accommodate several smaller checks from a platform rather than one concentrated commitment

- You want access to an investment committee that can move a decision forward without relying on one family's personal engagement

The co-investment advantage

MFOs often serve as natural co-investment aggregators. A single MFO relationship can result in participation from multiple client families in the same deal, which helps developers fill out a capital stack without running parallel conversations with dozens of individual investors.

According to the PwC Family Office Deals Study, 69% of family office investments in H1 2025 were club deals. MFOs are often the mechanism that makes those club structures work at scale.

For a fuller comparison of how family offices stack up against other institutional LP types, the family offices vs. private equity funds guide is worth reading before you finalize your target list.

Key takeaway: MFOs are more accessible, more process-driven, and better suited to developers who need to build institutional LP relationships from the ground up. The access path is wider, and the co-investment potential can be significant.

The 5-Factor Decision Framework: How to Choose Which to Target

Once you understand both structures, the practical question is: which one fits your specific raise? Here is a framework built around the five factors that actually matter.

Factor 1: Check size

This is the fastest filter. Think about the size of the single check you need from one LP source.

- SFO: Better suited when you need one concentrated check of $10M to $25M or more from a single relationship. SFOs can act with conviction when the deal matches their mandate.

- MFO: Better suited when you are filling a capital stack with several checks in the $2M to $10M range from multiple sources. The platform's co-investment structure makes this more natural.

Practical note: Most family offices, regardless of type, deploy equity tickets in the $5M to $15M range per deal according to industry research. Developers expecting a single $30M check from one family office without a prior relationship are often disappointed.

Factor 2: Asset class

Family office appetite is not uniform across asset classes. According to Citi's family office research, multifamily residential accounts for roughly 36% of family office real estate investment, making it the most common single asset class. Industrial and logistics are also in strong demand.

- SFO: Can accommodate more specialized or niche asset classes when the family has relevant operating experience or a specific mandate.

- MFO: Tends to favor mainstream asset classes with proven institutional demand. Multifamily, industrial, and mixed-use with residential components move through MFO processes more predictably.

If your deal is in a less conventional category, an SFO with a matching background is often more realistic than trying to fit a niche deal into an MFO's standard review process.

Factor 3: Relationship path

How you access the conversation matters as much as what you bring to it.

- SFO: Almost always requires a warm introduction from a trusted advisor, co-investor, or known intermediary. Cold outreach has a very low conversion rate.

- MFO: More accessible through advisors, capital advisory firms, and institutional platforms. The intake process is more defined.

If you do not yet have the right introduction, your capital stack and positioning need to be investor-ready before that conversation happens. Understanding how to structure the right capital stack for institutional LP due diligence is covered in the capital stack guide for developers.

Factor 4: Governance and diligence expectations

- SFO: Diligence is tailored to the family. One meeting with the right principal can move faster than any committee process. But it can also stall indefinitely if the principal loses focus or priorities shift.

- MFO: Diligence follows a defined path. Slower in some ways, but more predictable. You know what they need, and you can prepare for it.

Developers who have not gone through institutional LP due diligence before often find MFO processes more navigable because the requirements are documented and consistent.

Factor 5: Deal structure

The structure of your offering shapes fit more than most developers realize.

Both SFOs and MFOs have largely moved away from blind pool fund commitments. Deal-by-deal and direct investment structures are now the dominant preference across both types.

Mistakes That Waste Family Office Meetings

Even developers who target the right type of family office can undermine the conversation with avoidable mistakes. These are the ones that come up most often.

Pitching the same deck to every family office. SFOs and MFOs evaluate deals differently. An SFO principal wants to understand how the deal fits their family's specific goals. An MFO investment committee wants to see how the deal fits their documented mandate and risk framework. A generic pitch that ignores those differences signals that the developer has not done their homework.

Leading with return projections instead of structure. In 2026, family offices are asking a different first question. As one industry analysis of family office behavior put it: the first question is no longer "how high is the return?" It is "what happens if things do not go to plan, and how is the deal structured to protect us?" Developers who open with IRR targets before addressing downside protection, capital structure, and alignment are starting from the wrong place.

Treating access as a volume problem. More outreach does not equal more meetings with the right people. Family offices that receive cold pitches route them to the bottom of the pile or ignore them entirely. The ones that get serious attention come through trusted introductions. Sending the same email to 200 family office contacts produces almost nothing. One warm introduction from the right advisor produces a real conversation.

Not having the capital stack right before the first meeting. Family offices, especially MFOs with formal investment committees, will ask detailed questions about the full capital stack in the first or second meeting. If the structure is not investor-grade before you walk in, you are unlikely to get a second conversation. Getting the structure right before outreach begins is not optional.

Misreading the timeline. SFO decisions can be fast when the principals are engaged, but they can also stall for months. MFO processes are more predictable but often slower due to committee cycles. Developers who build a fundraising timeline without accounting for the realistic pace of family office decision-making often find themselves in trouble mid-raise.

Choose the Path That Fits the Deal, Then Get the Introduction Right

The SFO versus MFO question does not have a universal answer. The right target depends on the deal, the developer's current access, and the stage of the capital raise.

Here is the short version of the framework:

- If you have a warm introduction and a specialized deal: SFO is worth pursuing. The relationship-led, bespoke nature of a single-family office can work in your favor.

- If you are building institutional LP relationships for the first time: Start with MFOs. The access path is wider and the process is more navigable.

- If your raise is in multifamily or industrial: Both types can work. MFOs are often the faster first step, with SFOs as a secondary layer once relationships develop.

- If your raise needs co-investment from multiple sources: MFOs are structured to support that. Their club deal capability is a real advantage.

- If your capital stack is not yet institutional-grade: Neither type will close. Fix the structure first.

The most common mistake is not choosing the wrong type. It is spending months on outreach before the deal is structured to pass institutional LP review. Family offices, whether SFO or MFO, are asking harder questions than they were three years ago. Structure, downside protection, and operator alignment are evaluated before return projections.

If you are a seasoned developer raising $10M or more and are not yet sure which family office profile fits your raise, the right first step is a capital strategy conversation, not a pitch meeting.

Ready to identify which family office profile fits your raise? IRC Partners works with seasoned real estate developers raising $10M+ in institutional LP equity. We structure the deal first, then coordinate warm introductions to the right allocators. Book a capital strategy call to get clarity on your target profile before you start outreach.

For a broader view of the institutional allocator landscape, the institutional allocators warm introduction framework covers the full process from capital stack preparation through to first LP conversations.

Frequently Asked Questions

What is the difference between a single-family office and a multi-family office?

A single-family office manages the wealth of one family, making decisions based on a bespoke and often personal mandate. A multi-family office serves several families through a professional platform with standardized investment committees. For developers, single-family offices offer more flexible, relationship-driven terms, while multi-family offices provide a more structured intake process and the ability to aggregate capital from multiple sources.

Which type of family office writes larger checks for real estate equity?

Check size is determined by assets under management rather than office type. Most offices deploy equity tickets in the 5M dollar to 15M dollar range. While some single-family offices with massive liquidity can write concentrated checks above 20M dollars, multi-family offices often reach those levels by pooling smaller checks from several families into a single co-investment vehicle.

Do family offices prefer direct investments or fund commitments in 2026?

There has been a definitive shift toward direct, deal-by-deal structures. By 2026, nearly 69 percent of family office investments are structured as club deals or direct assets. Investors now prioritize the transparency and governance of specific assets over the blind pool risk associated with traditional fund commitments.

How do family offices find real estate deals to invest in?

Sourcing is almost entirely relationship-based. Family offices rely on a circle of trust consisting of advisors, existing partners, and established capital intermediaries. Cold outreach from unknown sponsors is generally ignored, as warm introductions serve as the primary filter for deal quality and sponsor credibility.

What asset classes do family offices favor for equity right now?

Multifamily residential remains the dominant asset class, representing roughly 36 percent of portfolios. Industrial, logistics, and data centers follow closely as high-conviction sectors. While niche assets can find a home, they typically require a specific mandate match within a single-family office rather than a broad platform.

How long does it take a family office to make an investment decision?

Timelines vary by complexity. A principal might issue a term sheet in a few weeks if a deal is a perfect fit. Conversely, multi-family office platforms—with their formal committees—typically require three to six months to move from initial introduction to a final capital commitment.

What do family offices look for in a developer before committing equity?

They evaluate the operator institutional readiness. This includes a documented history of stabilized assets, a sophisticated capital stack, and clear alignment of interests. In 2026, the ability to articulate a realistic downside strategy is just as important as the projected internal rate of return.

This isn't for pre-revenue companies or first-time founders. It's for operators at $1M+ ARR, raising $5M to $250M of institutional capital, who've done this before and want the next round architected right. If that's you, schedule a call to discuss HERE.

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.