.svg)

.png "Investor Ready Capital decorative background element")

The Real Estate Developer's Guide to Raising $10M-$50M in Institutional Capital Without Losing Control of Your Deal

The Real Estate Developer's Guide to Raising $10M-$50M in Institutional Capital Without Losing Control of Your Deal

You have completed projects. You have a track record. You have a deal that pencils. And you still can't close institutional capital.

This is the most common story IRC Partners hears from seasoned developers. The problem is almost never the deal. According to the 2024 Real Estate Allocations Monitor, institutional target allocations to real estate remain at 10.8% in 2024. The capital exists. What most developers are missing is the structure, the story, and the access that institutional LPs require before they commit.

The hard truth: institutional fundraising is not a bigger version of HNWI fundraising. It operates by completely different rules.

Raising from high-net-worth individuals is relationship-driven. You pitch your vision, show your track record, and close on trust. Institutional LPs, especially family offices deploying $10M+ checks, run a formal process. They evaluate governance, waterfall mechanics, GP commitment, reporting infrastructure, and alignment of interests before they ever get to your returns narrative. Developers who show up with a HNWI pitch deck dressed up for institutional consumption get passed over, not because their projects are weak, but because their structure signals that they don't understand the game they're playing.

This guide is the framework for developers who are ready to change that. It covers why institutional raises fail, what the right capital stack looks like at the $10M-$50M level, how to protect your GP economics and deal control, and how to get in front of the right allocators. If you want to understand how capital structure decisions affect every layer of your raise, this breakdown of the capital stack is required reading before you go to market.

Why Most Developers Fail to Raise $10M+ in Institutional Capital

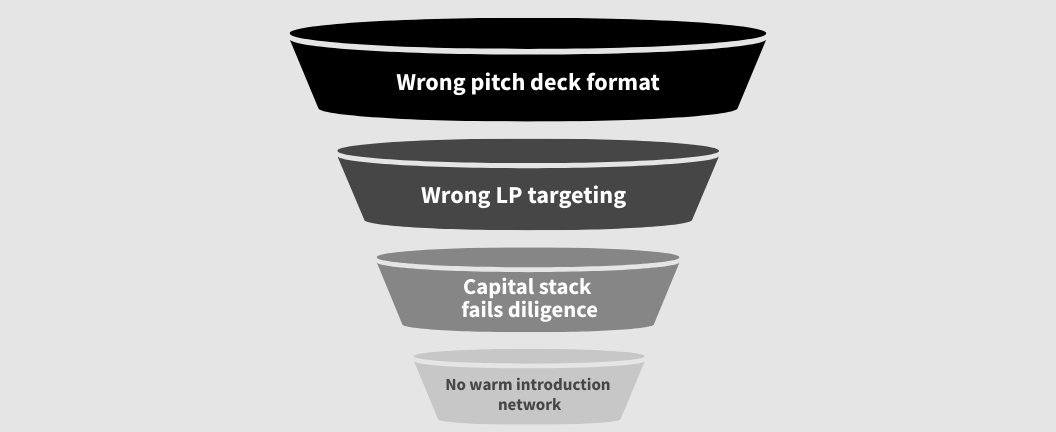

Most developers who hit the institutional wall aren't failing because of bad assets or weak returns. They're failing because they've never been told what the institutional screening process actually looks like. Here are the four failure modes that kill deals before they ever reach an LP investment committee.

Failure Mode 1: The HNWI Pitch Deck in a New Suit

Institutional LPs conduct what amounts to an operational audit disguised as investment due diligence. The Institutional Limited Partners Association (ILPA) has standardized this process through a Due Diligence Questionnaire that covers everything from team composition to cybersecurity protocols. The ILPA Principles establish three non-negotiable requirements: alignment of interests, governance, and transparency.

A pitch deck built for HNWI investors fails all three. It leads with the opportunity, the returns, and the story. Institutional LPs want to see the governance framework first. Who has decision-making authority? What controls prevent conflicts of interest? How are valuations conducted independently? Developers who can't answer these questions with documented processes get screened out before the first meeting.

Failure Mode 2: Targeting the Wrong 87% of Family Offices

Most family offices deploy checks in the $1M-$5M range. Only about 13% of family offices are positioned to write $10M+ checks on a single real estate deal. Developers who blast outreach to every family office they can find waste months chasing the wrong capital. Worse, they burn relationships with LPs who might have been right for a future deal.

The fix is not more outreach. It's better targeting.

Family offices that write $10M+ checks have specific requirements: direct GP access, co-investment rights, and a clear understanding of the harvesting plan. They underwrite based on alignment, trust, and legacy, not pitch polish or projected IRR.

Failure Mode 3: A Capital Stack That Can't Survive Diligence

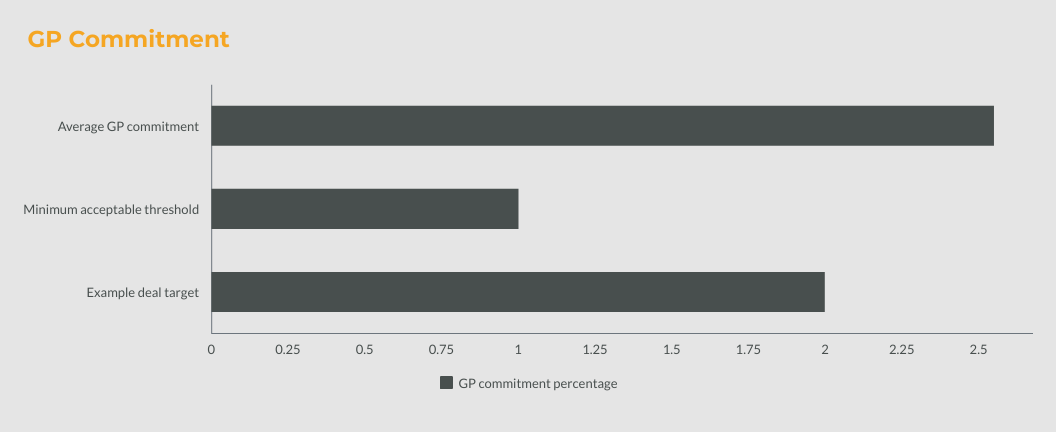

This is where most deals die. The waterfall is over-promoted at base case. The GP commitment is below the 1% threshold that triggers LP scrutiny. The preferred return floor is missing or ambiguous. Reporting commitments are vague.

According to Carta fund administration data, the average GP commitment for private equity funds runs 2.55%. LPs view GP commitment as the single most important alignment signal. Anything below 1% raises serious questions. The money needs to be real, not manufactured through fee waivers or creative structuring. Institutional LPs see through both.

Failure Mode 4: Cold Outreach to Institutional Allocators

Cold outreach to institutional LPs has a near-zero conversion rate. This is not an exaggeration. Institutional LPs receive hundreds of unsolicited decks every month. They act on warm introductions from trusted intermediaries. A developer without warm access to the right allocator network is not going to close institutional capital through direct outreach, no matter how good the deal is.

The four failure modes share a common root: developers treating the institutional raise as a larger version of what they've already done, rather than a fundamentally different process that requires a fundamentally different preparation.

What Institutional Capital Actually Looks Like at $10M-$50M

Before you structure a deal or approach a single LP, you need to understand who the players are, what they actually deploy, and what they require. Most developers have a vague sense of "institutional capital" as a category. The reality is far more specific.

The Three Capital Types for CRE Raises

At the $10M-$50M level, developers are typically working with one or more of these three capital types:

- LP Equity: The most common structure for ground-up development. LPs contribute equity capital in exchange for a preferred return plus a share of profits above the hurdle. The GP retains the promote. This is the structure most institutional family offices expect at this deal size.

- Preferred Equity: Sits between senior debt and LP equity in the capital stack. Preferred equity investors receive a fixed preferred return (typically 8-12%) before any profit sharing. Useful for filling gaps in the capital stack without diluting the LP equity tier.

- Structured Debt: Construction loans, bridge loans, and mezzanine debt. These are debt instruments, not equity, but they are often structured with equity kickers or warrants at the institutional level. Understanding how debt layers interact with equity layers is critical for protecting GP economics.

Who the Institutional LPs Are at This Deal Size

The table below maps the LP landscape for $10M-$50M CRE raises. Each LP type has a different check size, timeline, and primary requirement.

Regulatory compliance, asset-liability match

For most developers in the $10M-$50M raise range, family offices are the most accessible starting point. They move faster than pension funds and endowments, have more flexible mandates, and are more willing to engage with deal-by-deal structures. The tradeoff is that most family offices deploy $1-5M per deal. The 13% that write $10M+ checks require a different approach entirely.

Deal-by-Deal vs. Blind Pool: What 2026 LPs Prefer

Institutional LPs have shifted decisively toward deal-by-deal structures. In a deal-by-deal model, the LP commits to a specific project rather than a blind pool fund. This gives them more ownership, more transparency, and more control over their exposure. For developers, this is actually an advantage. You're not trying to raise a fund. You're raising capital for a specific project with specific assets, timelines, and return profiles.

The implication: your capital raise materials need to be project-specific, not fund-generic. Institutional LPs in 2026 are not writing checks into blind pools from developers they don't know. They want to see the specific deal, the specific market, the specific team, and the specific structure.

Developers who are also exploring non-traditional capital structures alongside LP equity should review how PIPE opportunities are being used by experienced real estate operators to access growth capital at scale.

The Institutional-Grade Capital Stack: What It Must Include

This is the section most developers skip. They focus on the pitch, the deck, the returns narrative. But institutional LPs evaluate the capital stack before they evaluate the opportunity. A deal with a clean, properly structured capital stack will outperform a better deal with a messy one every time.

Here is what an institutional-grade capital stack must include at the $10M-$50M level.

Layer 1: Senior Debt

Senior debt is the foundation. At this deal size, you are typically working with construction loans or bridge loans from commercial banks or debt funds. Key parameters institutional LPs will scrutinize:

- LTV ratio: Most institutional-grade construction deals target 55-65% LTC (loan-to-cost). Higher leverage signals risk, not sophistication.

- Recourse vs. non-recourse: Institutional equity LPs strongly prefer non-recourse or limited-recourse structures. Full personal recourse on senior debt creates misaligned incentives.

- Lender quality: The identity of your senior lender matters. A regional bank relationship lender signals a different risk profile than a structured debt fund.

Layer 2: Preferred Equity

Preferred equity fills the gap between senior debt and LP equity. It is not optional at this deal size. Institutional LPs expect to see it. Key parameters:

- Preferred return threshold: 8-10% is the institutional standard. Below 8% raises questions. Above 12% compresses LP equity returns.

- Cumulative vs. non-cumulative: Cumulative preferred returns accrue if unpaid. Non-cumulative do not. Institutional LPs will require cumulative preferred returns in most ground-up structures.

- Conversion rights: Some preferred equity structures include conversion rights to LP equity under specific conditions. These must be clearly defined upfront.

Layer 3: LP Equity and the Waterfall

This is where deals get won or lost. The LP equity waterfall defines how profits are distributed between LPs and the GP. Institutional LPs will read every line of the waterfall before they commit.

Standard institutional waterfall structure for a $10M-$50M CRE deal:

- Return of capital to all investors

- Preferred return to LPs (typically 7-9% IRR)

- GP catch-up (GP receives a disproportionate share until they reach their promote percentage)

- Residual profits split (typical institutional split: 70/30 or 80/20 LP/GP above the hurdle)

The most common structural mistake is setting the GP catch-up too aggressively or placing the promote too low in the waterfall. Over-promoted structures at base case signal that the GP is optimizing for their own economics, not LP alignment.

Layer 4: GP Commitment

This is the most scrutinized number in your entire deal structure.

Carta fund administration data shows the average GP commitment for private equity funds at 2.55%. Anything below 1% triggers active LP scrutiny. The GP commitment needs to be real capital, not fee waivers or creative structuring. Institutional LPs want to know that losing money on this deal would genuinely hurt the GP financially.

For a $20M equity raise, a 2% GP commitment means the GP is putting up $400,000 of personal capital. That is the minimum signal of alignment that most institutional LPs will accept.

The Red Flags That Kill Deals in Diligence

- No preferred return floor, or a preferred return below 7%

- GP commitment below 1% of total equity

- Waterfall with promote at base case (before LP preferred return is fully paid)

- Vague governance terms with no defined decision-making authority

- Quarterly reporting commitments not specified in the LPA

- No independent valuation methodology documented

If any of these apply to your current deal structure, you are not ready to go to market with institutional LPs. The structure needs to be fixed first.

How to Protect Your GP Economics and Keep Control of Your Deal

The title of this guide promises you can raise institutional capital without losing control. Here is exactly how that works in practice.

The fear most developers have is legitimate. They've heard stories of institutional LPs taking over deals, forcing exits at the wrong time, or squeezing GP economics down to nothing. Those stories are real. But they almost always trace back to the same root cause: the developer negotiated from a position of structural weakness because they needed the capital more than the LP needed the deal.

The answer is not to avoid institutional capital. The answer is to structure the deal and the relationship correctly before you sit across from an LP.

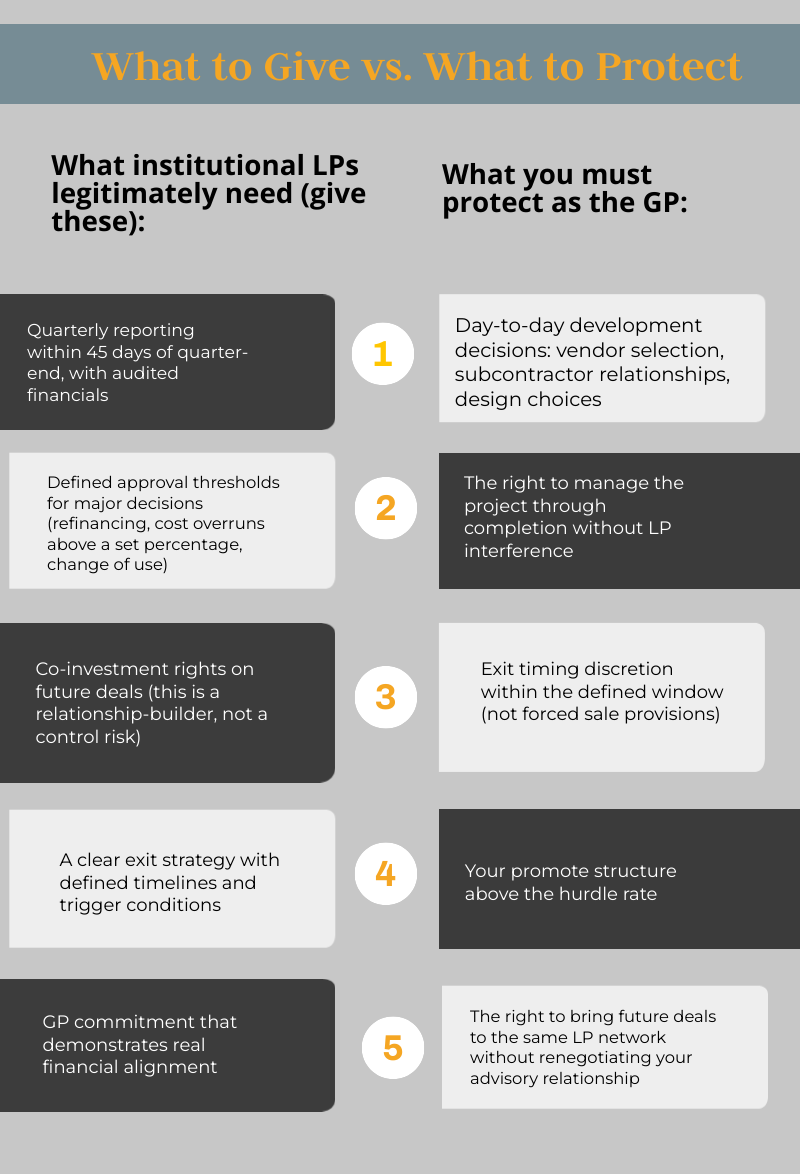

What to Give vs. What to Protect

What institutional LPs legitimately need (give these):

- Quarterly reporting within 45 days of quarter-end, with audited financials

- Defined approval thresholds for major decisions (refinancing, cost overruns above a set percentage, change of use)

- Co-investment rights on future deals (this is a relationship-builder, not a control risk)

- A clear exit strategy with defined timelines and trigger conditions

- GP commitment that demonstrates real financial alignment

What you must protect as the GP:

- Day-to-day development decisions: vendor selection, subcontractor relationships, design choices

- The right to manage the project through completion without LP interference

- Exit timing discretion within the defined window (not forced sale provisions)

- Your promote structure above the hurdle rate

- The right to bring future deals to the same LP network without renegotiating your advisory relationship

Waterfall Design: How to Protect the Promote

The promote is the GP's primary economic incentive. It is also the first thing institutional LPs try to compress. Here is how to protect it.

Design the waterfall in tiers, not as a single promote level. A tiered waterfall rewards the GP more as returns improve. At the base case (7-9% LP IRR), the GP might receive 20% of profits. At a 15%+ LP IRR, the GP might receive 30-35%. This structure is actually more appealing to institutional LPs because it aligns the GP's incentive with LP outperformance, not just deal completion.

Never put the promote below the preferred return hurdle. The LP gets their preferred return first. Then the GP catch-up. Then the residual split. Any structure that gives the GP promote before the LP preferred return is fully paid will be rejected by institutional diligence, and rightfully so.

The Advisor's Role in Protecting Your Position

This is where having an equity-aligned advisor changes the dynamic entirely. A placement agent gets paid when the deal closes. Their incentive is to close, not to protect your economics. An equity-aligned advisor like IRC Partners takes 3-5% advisory equity and earns on the outcome, not the transaction.

That alignment changes every negotiation. When your advisor's economics are tied to your long-term success, they push back on LP terms that compress your promote or add control provisions that limit your operating authority. They structure the deal to protect your position before the first LP conversation happens.

One engagement with IRC covers all future raises through exit. That means the capital stack gets structured once, correctly, and then IRC's network of 307,000+ institutional allocators is deployed to find the right LPs for each deal. You are not starting from scratch with every raise.

For a deeper look at how developers position their deals specifically for family office investors, the guide on presenting funding needs to family offices covers the relationship-building and materials preparation that makes the difference at this stage.

If you want to understand how capital advisory firms differ in their approach to protecting developer economics, comparing the top real estate capital advisory firms for $50M raises shows you exactly what to look for in an advisor before you sign an engagement.

How to Get in Front of the Right Institutional LPs

Structure gets you ready. Access gets you funded.

Most developers underestimate how closed the institutional LP market actually is. Pension funds, endowments, and the family offices that write $10M+ checks are not browsing deal submissions. They are allocating capital through relationships they have built over years, through trusted intermediaries, and through co-investment networks where one LP's commitment signals to others that the deal has been vetted.

Cold outreach to institutional LPs converts at nearly zero. Warm introductions from trusted intermediaries convert at 30%+. That gap is not a minor advantage. It is the entire game.

The 13% That Actually Write $10M+ Checks

Most family offices deploy $1-5M per real estate deal. They are valuable LPs, but they cannot anchor a $10M-$50M raise on their own. The 13% of family offices that write $10M+ checks on a single deal have a different profile. They have professional investment staff. They run formal diligence processes. They require ILPA-aligned reporting and documented governance. And they are almost exclusively accessed through warm introductions from advisors or co-investors they already trust.

IRC Partners maintains a network of 307,000+ institutional allocators, including family offices managing $17B+ in assets that actively request deal referrals. The 77 global investment bank syndicate partners provide additional access to institutional capital channels that most developers cannot reach independently.

Sequencing the Raise: Anchor First

The single highest-leverage move in any institutional raise is securing an anchor investor before approaching larger LPs. An anchor investor, even at $500K-$1M, shifts every subsequent conversation. Instead of "will you be first?", you are asking "here's who's already committed." That shift changes the dynamic entirely.

The sequence for a well-run $10M-$50M institutional raise looks like this:

- Structure the deal (capital stack, waterfall, governance docs, data room)

- Secure an anchor (a respected operator, a smaller family office, or a strategic co-investor)

- Approach the 13% (family offices and institutional allocators in the right check size range)

- Build momentum (each commitment makes the next one easier to close)

- Close the round with a defined timeline and no open-ended commitments

The developers who approach capital raising with the right strategic foundation understand that the raise begins months before the first LP meeting. The preparation, the structure, and the access strategy are the raise. The LP meetings are just the execution.

Case Study: How One Developer Closed a $22M Institutional Raise Without Giving Up Deal Control

The following is an anonymized account based on an IRC Partners engagement. Details have been modified to protect client confidentiality.

The Challenge

The developer was a seasoned GP with four completed multifamily projects across the Southeast, all with strong realized returns. He had raised from HNWIs and regional family offices before, closing rounds between $3M and $8M per deal. His fifth project was a 220-unit ground-up multifamily development with a total capitalization of $38M. He needed $22M in equity and had already secured senior debt commitments.

He had spent four months approaching institutional family offices independently. He had warm relationships with several. None had committed. The feedback was consistent: the structure wasn't institutional-grade. The waterfall had the GP promote starting before the LP preferred return was fully paid. The GP commitment was 0.8% of total equity. The reporting commitments in the draft LPA were vague. Every LP he approached saw the same red flags.

The Approach

IRC Partners was engaged to restructure the deal before going back to market. The process took six weeks.

The capital stack was rebuilt from the ground up. The waterfall was redesigned with a tiered promote structure: 20% GP promote above an 8% LP preferred return, stepping up to 28% above a 15% LP IRR. The GP commitment was increased to 2.1% of total equity. Quarterly reporting commitments were formalized in the LPA with specific deadlines and content requirements. A co-investment right was added for the lead LP on future deals.

With the structure corrected, IRC identified six family offices within its network that matched the deal profile: Southeast multifamily, $10M-$15M check size, deal-by-deal structure preference, 3-5 year hold tolerance. Three of the six engaged in formal diligence. Two committed.

The Result

$22M closed in 11 weeks from first LP introduction. The GP retained full development authority, with LP approval rights limited to defined thresholds (refinancing, cost overruns exceeding 10% of budget, change of asset class). The promote structure was protected at every return tier. The GP's co-investment in future deals with the same LP network was pre-agreed, establishing the foundation for a multi-deal capital relationship.

The developer did not give up control. He gave up the structural weaknesses that were preventing institutional LPs from committing.

That is the IRC model. Structure first. Then raise.

What to Do Next: Your Institutional Capital Raise Starts Before You Pitch

Institutional LPs have long memories. One bad pitch, with a poorly structured deal and a GP who clearly doesn't understand the institutional process, can close a door for years. The cost of going to market wrong is not just a failed raise. It is a damaged reputation in a small, relationship-driven capital community.

Here are three things to do before you approach a single institutional LP:

- Audit your capital stack. Run every layer against the institutional checklist in this guide. GP commitment, waterfall mechanics, preferred return structure, governance terms, reporting commitments. Fix what's broken before you go to market.

- Build your data room. Institutional LPs expect immaculate documentation available within 24 hours of request. Audited financials, project proforma, market analysis, track record documentation, and the full LPA draft. If your data room isn't ready, you aren't ready.

- Identify the right allocator subset. Not all institutional LPs are right for your deal. Asset class, geography, check size, hold period, and structure preference all need to match. Targeting the wrong LPs wastes time and burns relationships.

If you are ready to raise at institutional scale and want an advisor who structures the deal first and then deploys a network of 307,000+ allocators to find the right capital, IRC Partners accepts a maximum of 10 new strategic partners per quarter by application only.

This is not a transactional engagement. It is a long-term capital formation partnership. One engagement covers all future raises through exit. Apply to work with IRC Partners and get your deal in front of the institutional LPs who are actively looking for exactly what you're building.

Frequently Asked Questions

What is the minimum track record required to raise institutional capital?

Most institutional LPs require a minimum of 3 completed development projects with documented returns. In 2026, the bar is higher than in previous years; investors heavily favor operators who can demonstrate a verifiable track record across at least one full market cycle to prove resilience.

How long does it take to raise $10M–$100M for a project?

A well-structured raise typically takes 4 to 9 months. Poorly organized efforts or cold outreach can easily extend this to 18 months. Having your capital stack, waterfall, and due diligence package pristine and ready before your first pitch is the most effective way to compress this timeline.

What is a GP promote and how do I protect it?

The GP promote is the developer's share of profits above the LP preferred return, typically 20%. To protect your promote, you must design waterfalls with favorable hurdle rates and avoid compounding preferred returns. It is vital to model various stress scenarios to ensure the promote remains intact even if project costs rise.

What is the difference between an American and European waterfall?

An American waterfall pays the GP promote on a deal-by-deal basis as each asset is sold or refinanced. A European waterfall only pays the promote after 100% of all LP capital across an entire fund is returned. For developers raising capital on a per-project basis, the American structure is superior for maintaining healthy cash flow.

How much GP equity co-investment do institutional LPs require?

LPs typically expect a GP co-investment of 1% to 10% of the total project equity. This skin in the game is a critical signal of alignment; without a meaningful financial commitment from the developer, many institutional allocators will refuse to engage regardless of the project's quality.

What asset classes attract the strongest conviction in 2026?

Multifamily and Industrial remain the top conviction sectors for institutional capital. Data centers are currently the fastest-growing allocation category, followed by life sciences and mixed-use residential. Sponsors who lack a clear, specialized focus in one of these areas currently face significant difficulty accessing capital.

What is the biggest mistake developers make when pitching LPs?

Using HNWI-grade materials for institutional meetings. Institutional allocators require formal capital stacks, stress-modeled waterfalls, and audited financials. Failing to provide these sophisticated materials signals a lack of institutional readiness and usually results in an immediate screen-out.

The wrong structure doesn't just cost you this round. It costs you the next three. IRC Partners advises founders raising $5M to $250M of institutional capital. If you're about to go to market and want the structure reviewed before investors see it, book a call here

What Is Investor Pitch Deck Preparation Services

Mixed-Use Real Estate Development: How $10M+ Sponsors Structure Mixed-Use Deals That Institutional Lenders Will Fund

How to Hire an Advisor for Capital Stack Strategy

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of seven

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.