.svg)

.png)

Family Office Deal-by-Deal vs. Blind Pool: What Real Estate Developers Need to Know

Family Office Deal-by-Deal vs. Blind Pool: What Real Estate Developers Need to Know

Deal-by-deal is the right structure to bring to a family office in 2026. Family office investments in funds have declined by 9 percentage points since 2020, while club deals and direct co-investments now account for 60% of family office investment volume, according to PwC's Global Family Office Deals Study 2024. Blind pool structures are not impossible to place, but they require a documented sourcing engine, institutional-grade quarterly reporting, 5 or more completed projects with realized exits, and at least one anchor LP relationship before outreach begins. Most developers raising $10M+ do not yet meet that bar. Deal-by-deal lowers the trust threshold, gives investors direct visibility into one specific asset, and matches how family offices actually want to deploy capital right now.

This article is the next step after deciding which type of family office to target. If you have already worked through how to choose between a single-family office and a multi-family office for your LP equity raise, the question you now need to answer is: what structure should you bring to that family office once you get the meeting?

The answer matters more than most developers expect. Family offices have quietly shifted how they deploy capital into real estate, and the structure you present is one of the first things they use to screen whether you understand how they think. For a deeper look at how institutional allocators evaluate real estate sponsors before a conversation even starts, see the IRC Partners warm introduction framework for $10M+ raises.

Here is what this article will show you:

- Why family offices are moving back toward deal-by-deal structures in 2026, and what is driving that shift

- What each structure actually demands from you as the developer, in terms of track record, reporting, and LP expectations

- A practical decision framework you can use to choose the right vehicle before outreach begins

The core argument is simple. For most $10M+ raises targeting family offices right now, deal-by-deal is easier to place. Blind pools are not impossible, but they require more proof than most developers realize before the first meeting.

Why Family Offices Are Leaning Back Toward Deal-by-Deal in 2026

This is not a new preference. Family offices have always valued control and visibility. But several years of weaker fund performance, longer hold periods, and opaque underwriting pushed many of them to pull back from blind pool commitments and closer to the asset itself. That shift has accelerated in 2026.

According to PwC's Global Family Office Deals Study 2024, family office investments in funds declined by 9 percentage points since the end of 2020. At the same time, club deals, where investors participate alongside others in a specific transaction, held steady at 60% of family office investments by volume. That combination tells you something important: family offices did not stop investing. They changed what they were willing to invest in and how they wanted to structure their involvement.

The Gencom example is the clearest live signal available. In February 2026, Gencom's CIO disclosed that family offices had historically made up about 20% of the firm's capital pool. On recent deals, that figure exceeded 50%, with the most recent transactions almost entirely funded by wealthy families. The reason cited was direct: family offices want better economics, more governance control, and a direct relationship with the operating sponsor. A blind pool structure eliminates most of those.

Why family offices prefer deal-by-deal structures in 2026

The underlying shift is about what happens when things go wrong, not when they go right. As one analysis of the 2026 IMN Winter Real Estate Forum noted, family offices and passive investors are "retrenching back to deal-specific deals, especially if it's a unique deal that truly can stand on its own versus allocating into blind pool funds." The first question from a family office is no longer "what is the projected return?" It is "what happens if this deal slips, costs rise, or exit timing changes, and how does the structure protect me?"

The real insight: deal-by-deal structures do not just give investors visibility. They give investors accountability. And in 2026, accountability is what moves capital.

Deal-by-Deal vs. Blind Pool: What Changes for the Developer

Understanding why family offices prefer deal-by-deal is only half the picture. The other half is understanding what each structure actually demands from you as the sponsor. Most developers underestimate how much more institutional a blind pool pitch has to feel from day one. The differences are not just legal. They show up in how you prepare, what you need to prove, and how long each stage of the process takes.

Key principle: The more discretion you ask for, the more proof you need before outreach begins. A deal-by-deal raise asks investors to trust your judgment on one asset. A blind pool asks them to trust your judgment on every asset you will ever buy inside the fund.

Side-by-side comparison: deal-by-deal vs. blind pool

What this means for your materials

A deal-by-deal raise requires a tight investment memo, a clear business plan for the specific asset, a well-structured waterfall, and evidence that you have done this type of project before. Investors are underwriting one deal. Make that deal easy to underwrite.

A blind pool raise requires something much closer to an institutional fund pitch. You need a polished private placement memorandum, a detailed track record across multiple projects, a documented sourcing and underwriting process, and a team that looks like it can execute a pipeline, not just one project. The 10 mistakes that kill your first institutional raise apply here in full force, and the most common one is showing up with a fund pitch that looks like a deal pitch with a different cover page.

When Deal-by-Deal Is the Better Structure

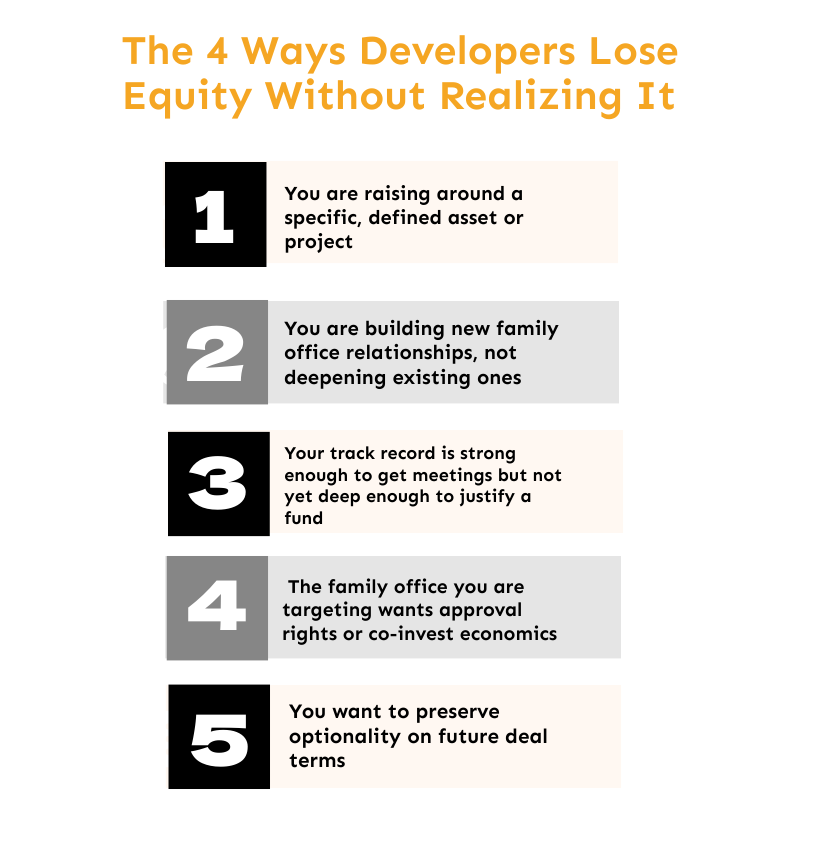

For most seasoned developers raising $10M+ from family offices in 2026, deal-by-deal is the right default. Here are five clear signals that it is the better fit for your raise.

1. You are raising around a specific, defined asset or project. If you have a ground-up multifamily site under contract, a value-add industrial acquisition under LOI, or a mixed-use development with a clear business plan, deal-by-deal is the natural structure. The investor can underwrite exactly what you are building, what it will cost, and how you plan to exit. That specificity reduces friction and shortens diligence.

2. You are building new family office relationships, not deepening existing ones. Family offices that do not know you yet are unlikely to commit blind discretion on a first engagement. Deal-by-deal gives them a lower-risk entry point. They can evaluate you on one transaction, and if it goes well, they will consider future deals. This is how most institutional LP relationships actually start.

3. Your track record is strong enough to get meetings but not yet deep enough to justify a fund. Three to five completed projects with good outcomes is enough to generate credibility in a deal-by-deal pitch. It is rarely enough to anchor a blind pool raise, where family offices want to see a documented sourcing machine and evidence of repeatable discipline across many cycles.

4. The family office you are targeting wants approval rights or co-invest economics. Many family offices, especially single-family offices with active investment committees, want to say yes or no to each deal. They do not want to commit capital to a fund and then receive capital call notices for assets they never approved. Deal-by-deal structures accommodate that preference. Blind pools do not.

5. You want to preserve optionality on future deal terms. Each deal-by-deal transaction is negotiated on its own terms. The waterfall, preferred return, and promote can be adjusted based on the asset type, risk profile, and LP relationship. A blind pool locks in fund economics across all assets for the fund's life. For developers still refining their LP relationships and deal mix, that flexibility has real value.

Bottom line: According to PwC's 2024 research, family offices still favor smaller deals under $25 million, with growing but selective interest in larger checks. Deal-by-deal structures match that preference almost perfectly, because the investor controls how much they deploy and on which assets.

When a Blind Pool Can Still Work With Family Offices

Blind pools are not dead with family offices. But the bar to get one placed is much higher than it was five years ago, and many developers who think they are ready for a fund are not. The honest question to ask yourself before pursuing a blind pool is: have I built the machine, or do I just have a deal list?

Use this checklist to pressure-test your readiness.

Blind Pool Readiness Checklist

Track record

- You have completed 5 or more projects of the same type you plan to acquire inside the fund

- You have realized exits, not just unrealized projections, to show to LPs

- Your returns are documented, auditable, and consistent across cycles, not just on your best deals

Pipeline and sourcing

- You have a documented sourcing process, not just a network of brokers

- You have a repeatable acquisition or development strategy that does not depend on finding the perfect one-off deal

- You can show a pipeline of future opportunities that fits the fund's stated criteria

Reporting and operations

- You have institutional-grade quarterly reporting in place from prior deals or funds

- Your team can manage investor communications, capital calls, and NAV reporting without adding significant headcount

- You have legal infrastructure for fund administration, including a PPM and fund counsel

Investor relationships

- You have at least one anchor LP who knows your work and is willing to commit early

- You have prior positive history with at least some of the family offices you plan to target

- Your existing LP relationships are strong enough to support a multi-year capital lock-up

Alignment

- Your fee structure is defensible against the question: "Why should I pay a management fee when I can access your deals directly?"

- Your promote is structured to align incentives, not front-load fees before performance is proven

If you cannot check most of these boxes honestly, a blind pool pitch to family offices is likely to generate polite interest that never converts. That is not a reflection of your project quality. It is a structure-fit problem. Understanding how the capital stack works and what investors actually want at each stage of a raise is the first step to choosing the right vehicle.

The Real Underwriting Test: Track Record, Reporting, Pipeline, and Control

When a family office evaluates whether to invest in your deal or your fund, they are really running a test across four variables. Each one answers a different question. Together, they determine whether your structure is credible or whether it is asking for more trust than you have earned.

Here is how to score yourself honestly before outreach begins.

Structure Fit Decision Matrix

How to read your score:

- Mostly Low: Deal-by-deal is the only credible structure right now. Focus on executing one or two strong projects, building the LP relationship, and earning the trust that a blind pool requires.

- Mix of Low and Medium: Deal-by-deal with a programmatic JV framework. Offer the family office a deal-by-deal entry now, with the option to formalize a broader relationship after the first project.

- Mostly Medium: Deal-by-deal is still the safer choice, but you can begin building the platform materials that a blind pool would require in 12 to 18 months.

- Mostly High: A blind pool is viable, provided you have an anchor LP and a compelling fund thesis that answers the question: "Why should I commit to your fund when I can access your deals directly?"

The question family offices actually ask in 2026 is not "what is the return?" It is "what happens if things do not go to plan, and how does the structure and the sponsor behave then?" Your score on these four variables determines whether you have a credible answer.

How Structure Choice Changes LP Expectations in First Meetings

The structure you bring to a family office changes the conversation from the first meeting. It determines what questions they ask, what materials they need to see, and what your data room has to prove. Developers who choose their structure before outreach show up prepared. Developers who try to explain structure gaps mid-process lose momentum.

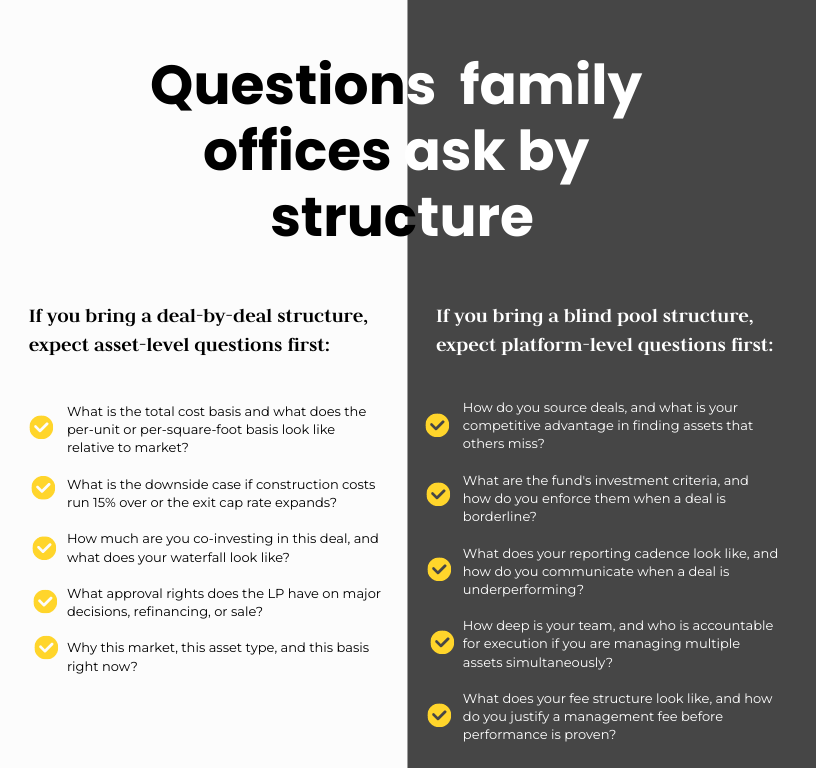

Questions family offices ask by structure

If you bring a deal-by-deal structure, expect asset-level questions first:

- What is the total cost basis and what does the per-unit or per-square-foot basis look like relative to market?

- What is the downside case if construction costs run 15% over or the exit cap rate expands?

- How much are you co-investing in this deal, and what does your waterfall look like?

- What approval rights does the LP have on major decisions, refinancing, or sale?

- Why this market, this asset type, and this basis right now?

If you bring a blind pool structure, expect platform-level questions first:

- How do you source deals, and what is your competitive advantage in finding assets that others miss?

- What are the fund's investment criteria, and how do you enforce them when a deal is borderline?

- What does your reporting cadence look like, and how do you communicate when a deal is underperforming?

- How deep is your team, and who is accountable for execution if you are managing multiple assets simultaneously?

- What does your fee structure look like, and how do you justify a management fee before performance is proven?

The key takeaway here is practical. If you choose deal-by-deal, build your materials around the asset. If you choose a blind pool, build your materials around the platform. Mismatching the two is one of the most common reasons a raise stalls after promising early conversations. For a full breakdown of how to position your raise to match what institutional investors are actually looking for, the 7 non-negotiables that make or break an institutional raise covers the preparation framework in detail.

A Simple Decision Framework for Seasoned Developers Raising $10M+

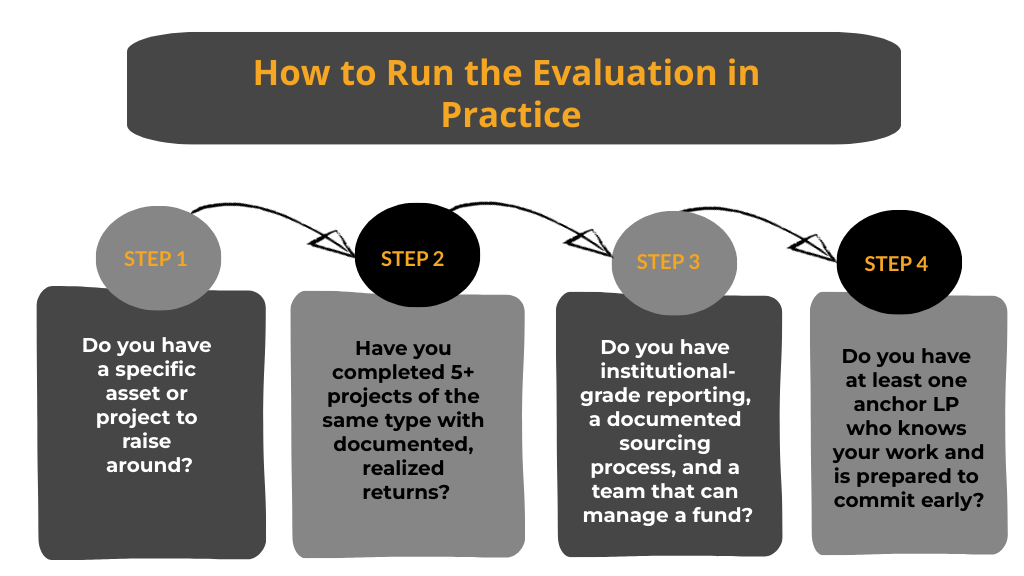

Before you start outreach, work through these questions in order. The answers will tell you which structure gives you the highest probability of closing.

Step 1: Do you have a specific asset or project to raise around?

- Yes: Start with deal-by-deal. You have something concrete for the investor to underwrite.

- No: Stop. Do not raise a blind pool on the promise of future deals. Find the asset first.

Step 2: Have you completed 5+ projects of the same type with documented, realized returns?

- Yes: A blind pool may be viable. Continue to Step 3.

- No: Deal-by-deal is the right structure. Use this raise to build the track record a blind pool requires.

Step 3: Do you have institutional-grade reporting, a documented sourcing process, and a team that can manage a fund?

- Yes: A blind pool is worth exploring. Continue to Step 4.

- No: Deal-by-deal with a programmatic JV framework. Offer the LP a deal-by-deal entry now with a path to a broader relationship.

Step 4: Do you have at least one anchor LP who knows your work and is prepared to commit early?

- Yes: A blind pool raise is viable. Build the fund materials and begin targeted outreach.

- No: Deal-by-deal first. Build the anchor relationship on a specific project, then revisit the fund thesis.

Choosing the structure that fits your current maturity is not thinking small. It is protecting close probability. If you are still deciding whether a family office is even the right LP type for your raise, family offices vs. private equity funds for real estate LP equity covers that decision in full.

Do Not Bring a Blind Pool Ask to a Deal-by-Deal Market

Family office capital is available in 2026. The constraint is not capital. It is the structure under which capital gets released.

Three things to take away from this article:

- Deal-by-deal is the default structure for most family office-targeted real estate raises right now. It asks for less blind trust, gives investors direct visibility into the asset, and matches how family offices actually want to deploy capital in this market.

- Blind pools still work, but only when the sponsor has already built the machine. A strong project pipeline is not a fund thesis. A repeatable sourcing engine, institutional reporting, and a track record of realized exits is.

- The structure you choose before outreach determines what questions get asked, what materials you need, and how long the process takes. Choosing the wrong one does not just slow you down. It signals to sophisticated LPs that you do not yet understand how they think.

The right next step is to pressure-test your structure before you start conversations, not after momentum stalls. If you want to understand why most capital raises fail before the first meeting, the positioning framework at that link is directly applicable to how family offices screen real estate sponsors.

IRC Partners works with seasoned developers to structure institutional-grade capital raises and coordinate warm introductions to family offices actively deploying $10M+ in real estate LP equity. If you are preparing for a raise and want to confirm your structure before outreach begins, book a capital strategy session to get a direct assessment.

Frequently Asked Questions

What is the difference between a deal-by-deal structure and a blind pool?

In a deal-by-deal structure, investors review and approve each specific asset before committing capital, providing total visibility. In a blind pool, investors commit capital to a fund upfront, granting the developer discretion to select assets according to a stated strategy. While blind pools offer speed and flexibility, they require a significantly higher level of trust from the partner.

Why do family offices prefer deal-by-deal structures in 2026?

Family offices have pivoted away from blind pools due to a desire for greater transparency, asset-level governance, and direct relationships with sponsors. Recent market data shows a steady decline in fund commitments as families prioritize club deals and direct investments, which allow them to monitor risks and performance at the individual project level.

How much track record do I need to raise deal-by-deal?

Generally, three to five completed projects with clear, realized outcomes are sufficient. Because the investor is underwriting a specific asset rather than your entire platform, the bar is more focused on your ability to execute that specific deal type responsibly and profitably. This lower barrier makes it the standard entry point for developers transitioning to institutional capital.

What questions do family offices ask in a deal-by-deal first meeting?

Expect deep-dives into asset-level metrics: cost basis relative to market, downside scenarios, developer co-investment, and specific governance rights. In 2026, allocators are far more concerned with the floor or capital preservation than the ceiling of projected internal rates of return.

What is the biggest mistake developers make when choosing a structure?

Mismatching platform maturity with the raise structure—specifically, bringing a blind pool pitch to a deal-by-deal market. A list of potential deals is not a fund thesis. Failing to provide the asset-level control that 2026 allocators demand can lead to lost momentum and damaged credibility with major family offices.

What is a programmatic JV and is it a middle ground?

A programmatic joint venture is a framework where a partner agrees to participate in future deals meeting specific criteria. It offers the developer predictability and the investor control without the capital being locked in a fund. This is an ideal path for developers with a repeatable strategy and at least one established anchor investor.

How do I know if my raise is better suited to a family office or private equity?

Family offices are typically more flexible, relationship-focused, and amenable to deal-by-deal structures. Private equity funds offer larger check sizes and faster decision timelines but come with higher governance burdens and standardized, rigorous investment committee processes that require institutional-grade back-office operations.

IRC Partners advises founders raising $5M to $250M of institutional capital on structure, positioning, and round architecture. 7 strategic partners per quarter. No placement agent model. No success-only theater. If you want a structural review of your current raise, apply at HERE

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.