.svg)

.png)

How Long Does Capital Raising Outcomes and Success Rates Take?

How Long Does Capital Raising Outcomes and Success Rates Take?

A capital raising engagement with an advisor typically runs 6 to 18 months from signed agreement through close. That range reflects two separate timelines running in parallel: the advisor's execution track, which covers preparation and outreach, and the investor's decision track, which covers diligence, committee approval, and legal close. The second track usually controls the finish date. Most timeline estimates operators receive collapse these two tracks into one number - and that is where planning errors start, where runway assumptions break down, and where operators end up signaling urgency to investors who notice when timelines slip.

Most timeline estimates operators receive collapse these two tracks into one number. That is where planning errors start. Understanding how the capital raising process actually works from engagement through close is the foundation. This article builds on that and maps each phase to a realistic duration range so operators can plan backward from investor timing rather than forward from an optimistic close date.

Key takeaways for this article:

- Most advisor-led raises run 6 to 18 months from signed agreement through close

- Advisor execution and investor decision timelines are separate clocks with different drivers

- Phase 1 prep is the most controllable variable in the entire timeline

- Institutional investors commonly need 60 to 120 days from first contact to serious commitment

- Planning for the realistic range protects runway, team capacity, and investor credibility

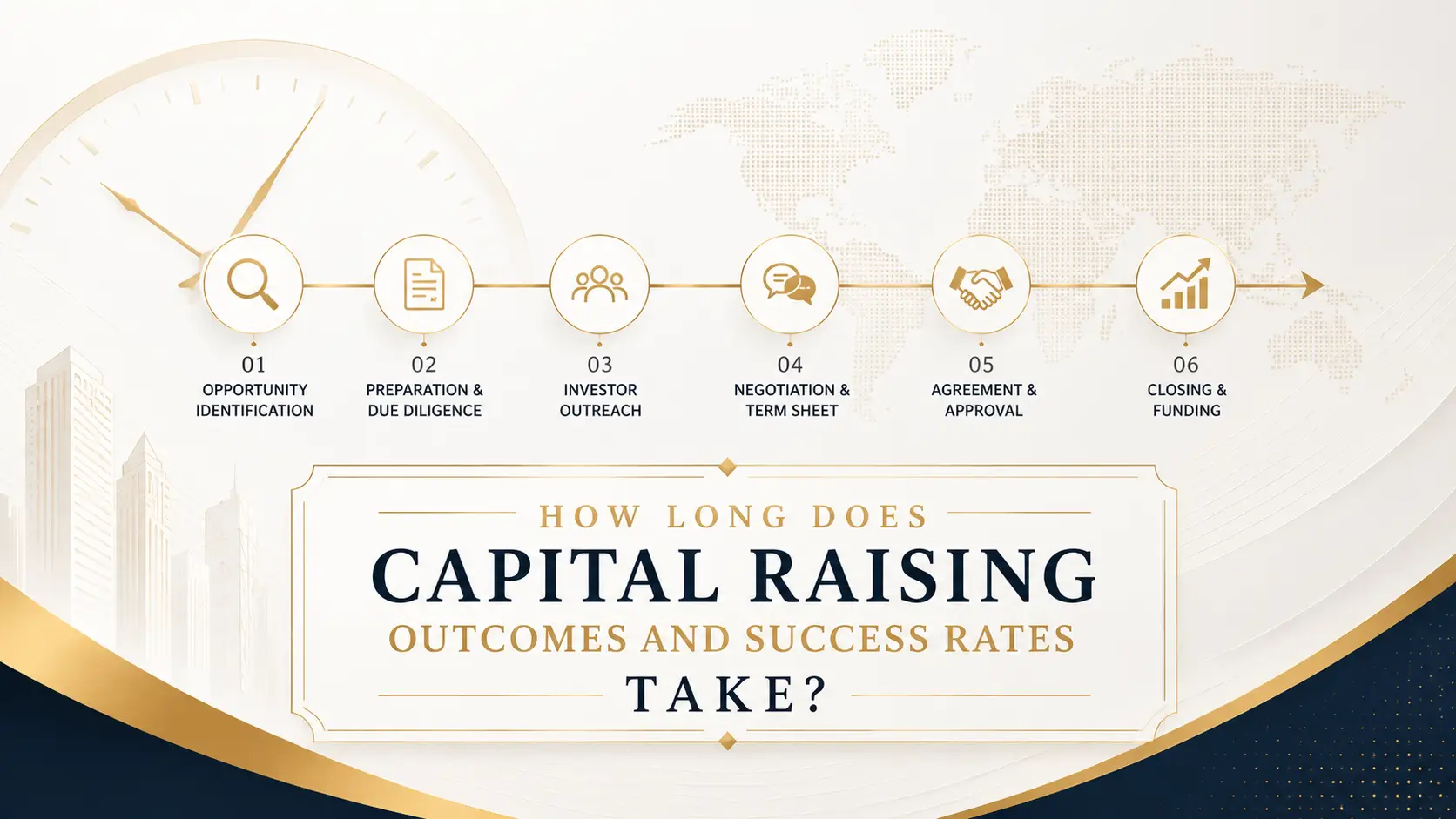

Phase 1: Pre-Outreach Preparation Usually Takes 1 to 8 Weeks

Signing an engagement agreement does not start the investor clock. It starts the preparation clock. Before any LP introduction happens, materials need to be investor-ready: track record package, financial model, executive summary, data room, capital stack, and governance structure. The advisor cannot run a credible institutional process without them.

A well-prepared operator who arrives at engagement with clean documentation and a resolved capital structure can move through this phase in 3 to 4 weeks. Most operators need 4 to 8 weeks. Some need longer if structure questions remain open at signing.

The table below shows the core prep tasks and what commonly delays each one.

The single biggest cause of Phase 1 delays is arriving at engagement with materials that were built for a different audience. Retail-grade pitch decks and informal track record summaries require a full rebuild before institutional outreach is appropriate. The IRC Partners guide on building a data room that closes institutional LPs in 30 days covers the exact folder structure, staged disclosure framework, and reconciliation steps that separate a fast institutional process from a slow one.

The practical implication: Phase 1 is the one phase operators can meaningfully compress before the engagement begins. Every week of preparation completed before signing is a week removed from the live engagement timeline.

Phase 2: Active Investor Outreach Usually Runs 6 to 20 Weeks

Outreach is not one event. It is a sequenced process: initial introductions, fit screening, follow-up calls, data requests, and investor qualification. Each step takes time, and the pace is largely set by the investor, not the advisor.

The key benchmark operators consistently underestimate: institutional investors commonly need 60 to 120 days from first contact to reach a stage of serious commitment or term-sheet-level conviction. That is not slow by institutional standards. That is the standard pace for a $10M+ private placement with a new GP relationship.

What drives variance in outreach duration

Five factors determine where a raise lands within the 6 to 20 week range:

- Investor channel type. Family offices with a single decision-maker move faster than institutional funds with investment committees and consultant layers.

- Raise size. Larger mandates require more LP conversations, longer qualification cycles, and more parallel tracks to reach coverage.

- Materials quality. Investors who can answer their own questions from Phase 1 materials move faster. Investors who have to request follow-up documents slow down.

- Sequencing discipline. Advisors who tier outreach by investor fit and warm introduction access generate faster early momentum than those who blast wide.

- Market conditions. When institutional committees are crowded or capital is concentrated with incumbent sponsors, even strong deals face longer response cycles.

The readiness criteria that determine whether an operator is ready to begin outreach are covered in detail in the timing and readiness guide. Phase 2 cannot be compressed by applying more pressure to investors. It can only be compressed by arriving with better materials and a tighter investor target list.

The practical implication: Outreach duration is mostly an investor-side variable. Operators who expect outreach to close in 4 to 6 weeks are almost always planning around a best-case scenario that applies to a minority of raises.

Phase 3: Diligence and Negotiation Usually Runs 12 to 32 Weeks

Diligence is not a single linear review. It runs across four parallel streams: investment analysis, operational verification, legal review, and investment committee approval. Each stream can stall independently, and they rarely move at the same pace.

A positive signal from an LP investment team is not funded capital. It is permission to enter diligence. The committee has not yet approved. Legal has not yet reviewed. Co-investors, if involved, have not yet aligned. This is where many operators misread the timeline and start planning around a close date that is still 3 to 5 months away.

Diligence timeline by investor type

The table below shows realistic ranges for the diligence phase by investor category, from term sheet or equivalent commitment signal through executed documents.

The most common delay triggers in Phase 3 are not deal quality issues. They are document gaps. Missing or outdated operating agreements, version mismatches between the data room and the PPM, unresolved structure questions that surface during legal review, and co-investor coordination lags are the primary causes of stalled closes. According to LP due diligence research from v7labs, the pre-commitment phase alone runs 4 to 12 weeks for most institutional investors, with endowments and pension funds often conducting reviews lasting 6 to 18 months for first-time manager relationships. The IRC Partners guide on how long institutional LP due diligence takes breaks down each overlapping approval track and explains why committee windows often add 1 to 2 months or more even after the core review is complete.

The practical implication: A 12 to 16 week diligence phase is normal for a $10M to $50M institutional raise. Operators who plan for 6 weeks are not being optimistic. They are setting themselves up for a runway shortfall and a credibility problem with investors who notice when timelines slip.

{{main-cta}}

Phase 4: Close and Post-Close Can Stretch from Week 24 to Week 52 and Beyond

Close is not a single event. It is a sequence of operational steps, and for raises with multiple investors, it may repeat across several tranches.

The steps between a signed commitment and funded capital include:

- Final subscription document execution by all parties

- AML/KYC verification for each investor entity

- Legal sign-off on operating agreements and side letters

- Fund administrator processing and account setup

- Wire instructions confirmed and capital transferred

- Post-close investor reporting and onboarding

For raises targeting a single anchor LP, this sequence can move in 2 to 4 weeks after documents are executed. For raises structured around multiple LPs closing in waves, the advisor's engagement often continues through a final close that may arrive 3 to 6 months after the first. Pipeline Road's 2026 fundraising data shows that for emerging managers, the final close typically arrives 6 to 12 months after first close, with most limited partnership agreements capping the total raise period at 18 months from first close.

The distinction that matters most: A first close is not a final close. Operators who plan their capital deployment timeline around a first-close date and then discover they are still running a second and third close 4 months later face real operational strain. The advisor's role, and the timeline, extends through the last dollar in.

The practical implication: Budget the engagement through final close, not first close. For layered or multi-LP raises, that typically means planning for a full engagement of 12 to 18 months, sometimes longer.

The Five Variables That Create the Most Timeline Variance

Most timeline overruns trace back to one or more of five variables. Operators who understand these before signing have a meaningful advantage in compressing the raise without cutting corners.

- Operator readiness at signing. This is the highest-leverage variable. Operators who arrive with clean materials, a verified track record, and a resolved capital structure compress Phase 1 from 8 weeks to 3. Those who do not can add 60 to 90 days before the first LP introduction happens.

- Capital structure complexity. Layered stacks with preferred equity, structured debt, and co-invest tranches require more diligence time from investors and more coordination across parties. Each additional complexity layer adds weeks to Phase 3.

- Investor channel type. Family offices and flexible private investors move on weeks-long cycles. Endowments, consultant-advised allocators, and fund-of-funds move on months-long cycles. The target investor list determines the realistic floor for the engagement timeline.

- Market conditions. Even well-structured deals slow when institutional committees are crowded, when capital is concentrated with incumbent sponsors, or when macro conditions create LP hesitation. These are external variables, but they are predictable enough to plan around.

- Advisor execution quality. Follow-up discipline, document control, investor sequencing, and the ability to move a stalled process forward without damaging the relationship are execution skills that separate advisors who compress timelines from those who let them drift.

The practical implication: Of these five, only the first is fully within the operator's control before the engagement begins. The others can be managed during the raise, but they cannot be eliminated.

Plan the Raise Like a Risk Window, Not a Best-Case Sprint

The most common timeline mistake is not a lack of ambition. It is planning around the fastest possible outcome and treating the realistic range as a fallback.

Operators who budget runway, legal spend, and internal team capacity around a 6-month close and then hit a 14-month engagement face compounding problems: runway pressure that forces bad decisions, internal stakeholders who lose confidence in the process, and investors who notice when an operator starts signaling urgency.

The right frame is a risk window, not a finish line. Plan the raise backward from realistic investor approval timing. Treat a faster close as upside. Treat the full 18-month range as the planning assumption for anything involving institutional LPs with committee processes.

The timeline you cannot control is the one that matters most. Investor decision cycles run on the investor's calendar, not the operator's. The advisor's job is to keep the process moving and prevent avoidable delays. The operator's job is to arrive ready and plan for the slower track.

IRC Partners structures engagements around phase-specific milestones and realistic investor timelines from day one. For operators raising $10M or more who want a timeline-aware, phase-structured engagement rather than a best-case estimate, that structure matters from the first conversation.

Frequently Asked Questions

How long does a full capital raising advisor engagement typically run from signing through close?

Most advisor-led institutional capital raises run 6 to 18 months from signed engagement agreement through final close. The range reflects four sequential phases: pre-outreach preparation (1 to 8 weeks), active investor outreach (6 to 20 weeks), diligence and negotiation (12 to 32 weeks), and close execution (2 to 8 weeks per tranche). Raises with a single anchor LP and clean materials at signing can close toward the lower end. Multi-LP raises with layered structures commonly run 12 to 18 months.

What causes the pre-outreach preparation phase to run longer than expected?

The most common causes are materials that were built for a retail audience rather than institutional review, inconsistent numbers across the pitch deck, financial model, and executive summary, unresolved waterfall and fee logic, and a data room that does not exist or is not staged for institutional access. Operators who arrive at engagement with these gaps in place add 4 to 10 weeks to the timeline before the first LP introduction can happen. Resolving these issues before signing is the highest-leverage timeline compression available.

How long do institutional investors typically take from first contact to a serious commitment?

Institutional investors commonly need 60 to 120 days from first contact to reach a stage of serious commitment or term-sheet-level conviction on a $10M+ private placement. That window covers initial fit screening, internal discussion, follow-up calls, data requests, and a preliminary investment team review. It does not include formal diligence, committee approval, or legal close, which run on a separate and longer clock after that initial conviction stage is reached.

What is the difference between a single close and a final close, and how does it affect the engagement timeline?

A single close is the first tranche of capital that funds under the offering documents. A final close is the last tranche, after which no additional investors may subscribe. For raises with one anchor LP, these may be the same event. For raises structured around multiple investors closing in waves, the final close can arrive 3 to 6 months after the first. The advisor's engagement, and the operator's active raise obligations, continue through the final close regardless of when the first tranche funded.

What are the five variables that drive the most variance in how long a raise takes?

The five primary variance drivers are operator readiness at signing, capital structure complexity, investor channel type, market conditions, and advisor execution quality. Operator readiness is the only variable fully within the operator's control before the engagement begins. Capital structure complexity and investor channel type set the realistic floor for the timeline. Market conditions and advisor execution quality determine how much the process drifts above that floor during the active raise.

How can an operator compress the timeline without cutting corners on diligence or materials quality?

Timeline compression happens before the engagement starts, not during it. Operators who arrive at signing with a verified deal-level track record, a fully structured capital stack, reconciled financial materials, and a substantially complete data room can move through Phase 1 in 3 to 4 weeks instead of 6 to 10. After outreach begins, the fastest lever is investor sequencing: targeting the highest-fit, most-accessible investors first generates early momentum that accelerates the broader process.

What does IRC Partners' typical engagement timeline look like for a $10M+ institutional raise?

IRC Partners structures engagements around phase-specific milestones rather than a single projected close date. For a $10M+ institutional raise, the planning framework typically spans 6 to 18 months from signed agreement through final close, with Phase 1 preparation running 3 to 8 weeks depending on operator readiness at signing. Operators who arrive with institutional-grade materials and a resolved capital structure move faster through preparation and into active outreach. Operators who need structural or materials work before outreach begins should plan for the longer end of the range.

Continue reading this series:

- Key Benefits of Capital Raising Outcomes and Advisor Success Rates

- How to Hire an Advisor for Capital Raising Outcomes and Success Rates

- When Does a Company Need Capital Raising Outcomes and Advisor Success Rates

The structure you carry into your first investor meeting sets the terms for every round that follows it. Founders who get it wrong spend the next three rounds negotiating from behind. IRC Partners advises operators raising $5M to $250M of institutional capital. The Capital Raise Pre-Flight runs your deal through the twelve gates institutional investors screen for, before any of them see it. Book your Capital Raise Pre-Flight consult here.

Need guidance on your capital raise?

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.