.svg)

.png)

How Can I Present My Funding Needs to Family Offices?

You have a solid deal. You have a track record. You've raised capital before. And family offices keep passing.

The problem almost certainly isn't your project. According to the BNY Wealth 2025 Investment Insights for Single Family Offices report, 64% of family offices expect to make six or more direct real estate investments in the next 12 months. The demand is real. The capital is there. What's broken is the presentation.

The rules changed. Family offices have fundamentally shifted how they evaluate deals since 2023. They no longer respond to the same pitch that worked with your high-net-worth individual network. If you're still leading with projected returns and a polished deck, you're speaking the wrong language to the wrong audience.

This article gives you the framework to fix that. If you're already working through the broader challenge of raising $10M to $50M in institutional capital, this is the piece that specifically addresses how to position and present to the family offices in that market who actually write large checks. The gap between a good deal and a funded deal is almost always a presentation problem. Here's how to close it.

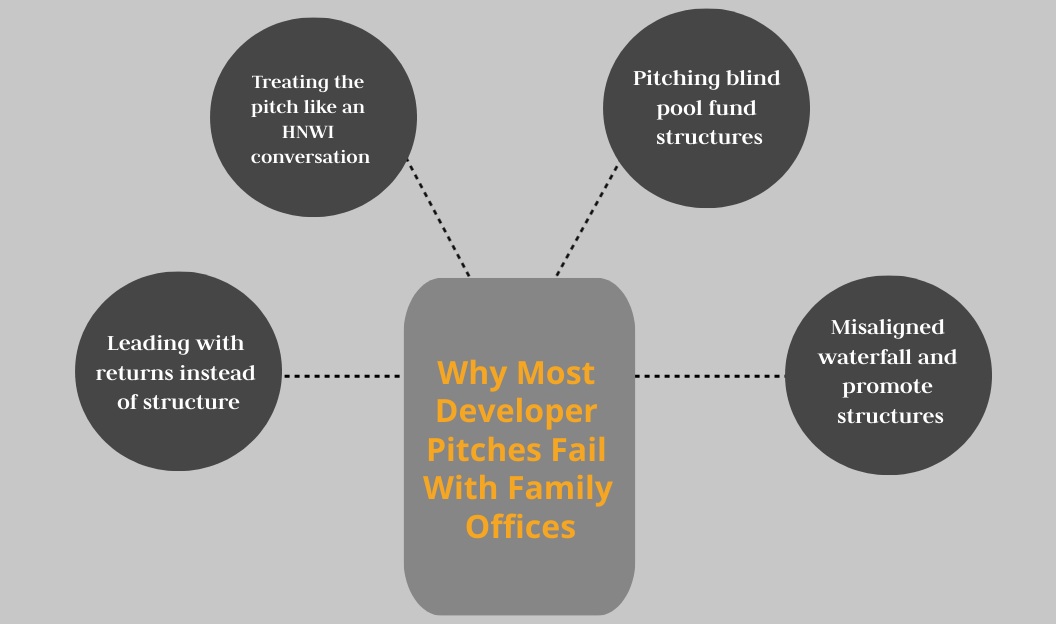

Why Most Developer Pitches Fail With Family Offices

Most developers who get passed over by family offices aren't losing on deal quality. They're losing on presentation format. Family offices are institutional allocators. They evaluate deals through a completely different lens than the private investors you've worked with before. The mismatch is predictable, and it shows up in the same four ways every time.

- Leading with returns instead of structure. The first question a family office asks is no longer "How high is the return?" According to Whitestone Capital's 2026 family office real estate report, the first question is now: "What happens if things don't go to plan, and how do the structure and partners behave then?" Developers who open with IRR projections signal they don't understand who they're talking to.

- Treating the pitch like an HNWI conversation. High-net-worth individuals often make decisions based on the relationship and the headline numbers. Family offices require institutional-grade documentation: stress-case models, governance frameworks, detailed waterfall mechanics, and a clear capital stack. Showing up without these materials signals you're not operating at the level they require.

- Pitching blind pool fund structures. Family offices have largely moved away from blind pool commitments. PwC's latest family office research finds that club deals and direct investments now account for roughly 69% of family office transactions. If your pitch asks an FO to commit capital to a fund before seeing the specific assets, you're fighting against a structural preference that has only strengthened over the past two years.

- Misaligned waterfall and promote structures. Family offices scrutinize promote structures in the context of downside scenarios, not just upside. If your waterfall shows the GP earning a promote even when the LP hasn't recovered their preferred return, that's a structural red flag. Whitestone Capital puts it plainly: "Misalignment destroys deals faster than weak markets." Models where GP incentives decouple from LP outcomes in a loss case are losing acceptance fast.

"Capital is no longer 'provided.' It is released. Not because of a compelling story, but only once structure, risk allocation, and decision logic are transparent." Whitestone Capital, Family Office Real Estate 2026

What Family Offices Are Actually Evaluating in 2026

Family offices don't think in quarters. They think in decades, sometimes generations. That time horizon changes everything about how they evaluate a deal. They're not just asking whether the project will deliver a 17% IRR. They're asking whether this operator, this structure, and this asset will hold up across market cycles they haven't seen yet.

The BNY Wealth 2025 Single Family Office report shows a 52% increase year-over-year in the number of family offices citing "alignment of interests" as a crucial consideration in direct investments. That's not a minor shift. It means the evaluation criteria have fundamentally changed, and most developers are still pitching to the old criteria.

How the Evaluation Criteria Compare

The table below shows the practical difference between what HNWIs typically evaluate and what institutional family offices require in 2026.

The 13% Rule

Here's a number most developers don't know: only about 13% of family offices actually write checks of $10M or more. The majority deploy $1M to $5M per deal. This means targeting the wrong family offices wastes months of effort on LPs who were never going to write the check you need. Identifying and approaching the right FOs, specifically those with the mandate and liquidity to lead a $10M-$20M commitment, is itself a strategic decision, not an afterthought.

Decision timelines have also lengthened. According to Whitestone Capital, "Decision cycles are longer, diligence runs deeper, and tolerance for uncertainty has fallen." Developers who expect a 30-day close are going to be disappointed and will often damage the relationship by showing impatience.

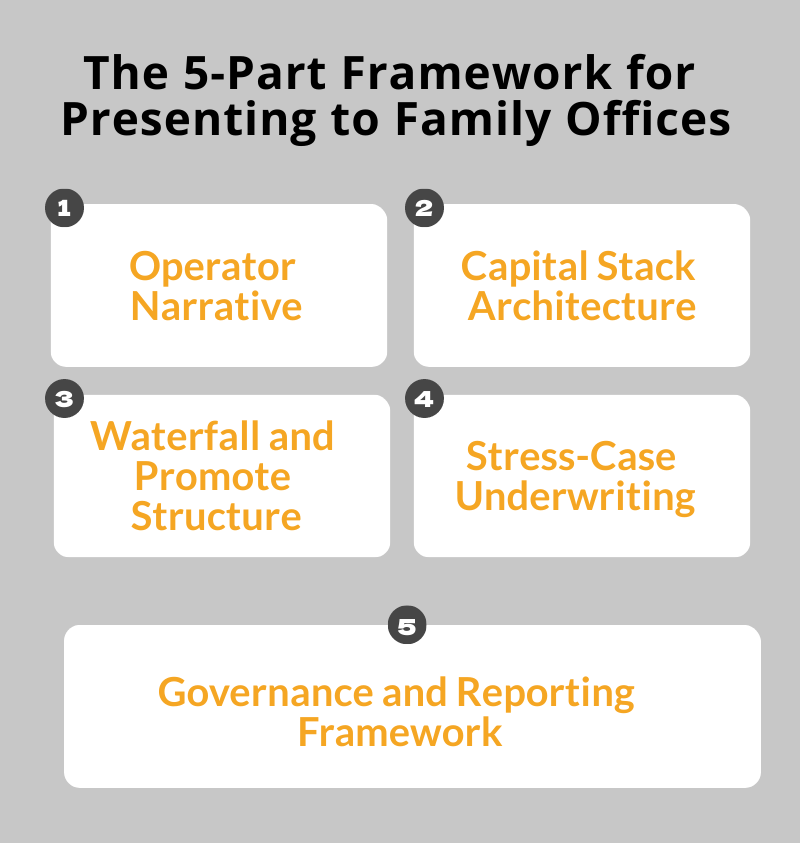

The 5-Part Framework for Presenting to Family Offices

The developers who consistently win family office commitments aren't necessarily running better projects. They're presenting better. The framework below is what institutional-grade presentation actually looks like. Each part addresses a specific evaluation criterion that family offices use. Skip any one of them and you create a gap in the picture that a sophisticated LP will notice.

- Operator Narrative. Don't lead with your best project. Lead with your full track record across market conditions. Family offices want to understand how you behaved when things went wrong: a project that ran over budget, a lease-up that took longer than expected, a market that turned. According to JMCO's 2026 family office real estate guide, "The quality of the partner matters as much as the property itself. Family offices should review the sponsor's track record across market cycles, not just recent performance during favorable conditions." The operator narrative is your answer to that standard.

- Capital Stack Architecture. Show a fully structured, institutional-grade capital stack before the first meeting. That means a clear layered structure: senior construction or permanent debt, preferred equity with defined return hurdles, and LP equity with explicit priority. The stack should be legible at a glance. A messy or incomplete capital stack is one of the fastest ways to signal that you haven't operated at this level before. For a deeper look at how to structure the layers correctly, the IRC guide on how the capital stack works covers the mechanics in detail.

- Waterfall and Promote Structure. Present your promote in the context of a downside scenario, not just the base case. Show explicitly what happens to LP returns if the project hits 80% of projected NOI. Show where the GP promote kicks in and whether it does so only after the LP has recovered their preferred return and capital. Structures where GP incentives decouple from LP outcomes under stress are being rejected. Structures where alignment is explicit and visible get funded.

- Stress-Case Underwriting. Include a bear case in your materials. This is the single most skipped element in developer presentations, and family offices notice the absence immediately. Model a scenario at 80% of projected NOI. Show debt service coverage at that level. Show the recapitalization path if needed. This doesn't signal weakness. It signals institutional discipline. For context on alternative capital structures that can add resilience to your stack, the IRC article on PIPE opportunities for real estate developers covers several approaches worth understanding before you structure your deal.

- Governance and Reporting Framework. Define the governance structure in writing before the meeting: quarterly reporting cadence, what decisions require LP consent, what triggers a capital call or recapitalization, and how disputes are handled. This is what separates institutional-grade operators from HNWI-grade ones. Family offices are choosing clarity of accountability. As Whitestone Capital notes, "Structure is not seen as a legal formality, but as an expression of risk allocation." If you want to understand how other operators are structuring advisory relationships to support this level of institutional presentation, the IRC comparison of top real estate capital advisory firms for $50M raises is a useful reference point.

What This Looks Like in Practice: An Anonymized Case Study

Consider a Southeast-based multifamily developer, a Principal with four completed ground-up projects and roughly $8M raised from a regional HNWI network over the prior six years. The next project was a 180-unit ground-up multifamily development requiring $18M in LP equity. The deal was underwritten conservatively. The submarket had strong fundamentals. By every internal measure, it was a fundable project.

Over six months, the developer pitched three family offices. All three passed. The feedback was vague: "not the right fit for us right now," "we're being selective," "we'll keep you in mind." No specific objections. No counter-proposals. Just polite exits. The developer's materials included a 20-slide deck with market data, projected returns, and a project timeline. There was no stress-case model. The capital stack was described in general terms. The waterfall was presented only in the base case. The governance section was a single paragraph. The pitch was built for an HNWI audience. It was being shown to institutional allocators.

After engaging IRC Partners, the approach was rebuilt from the ground up. The operator narrative was restructured to include two projects where the developer had navigated construction delays and a lease-up that ran 60 days behind schedule, with documentation of how each was resolved. The capital stack was formalized into a clear three-layer structure. A stress-case model was built at 80% projected NOI. The waterfall was rewritten to show LP recovery of preferred return before any GP promote. A governance framework was drafted covering quarterly reporting, LP consent rights, and recapitalization triggers. The deal was repositioned as a deal-by-deal JV structure, not a blind pool. For additional context on how capital raising strategy shifts at this level, the IRC article on what actually works when raising institutional capital in 2026 outlines the broader mindset shift required.

The result: a $20M commitment from a single-family office within 90 days of repositioning. Same developer. Same project. Different presentation.

The Mistakes That Kill Deals Even After a Strong Presentation

Even developers who build a strong institutional presentation can lose the deal in execution. The framework gets you in the room. What happens next determines whether you close.

- Sending the deck before the relationship exists. Family offices want to vet the operator before they evaluate the deal. Sending a full investment memorandum to a cold contact signals you don't understand their process. The first contact should be a brief introduction and a request for a conversation, not a 40-page OM.

- Using the same materials for every family office you approach. Family offices talk to each other. Bespoke positioning is not optional. Each presentation should reflect what you know about that specific FO: their asset class preferences, their typical check size, their governance requirements, and their current portfolio. Generic materials read as generic effort.

- Skipping the data room. By the time a family office is serious, they will want 24/7 access to organized documentation: audited financials on prior projects, operating agreements, construction contracts, debt term sheets, and a full due diligence package. Developers who scramble to assemble this after generating interest lose momentum and credibility at the worst possible moment.

- Underestimating the decision timeline. Family office investment decisions take 60 to 120 days minimum, sometimes longer. Developers who communicate urgency, push for faster decisions, or suggest the deal will close without them are almost always eliminated. The process moves at the LP's pace. Accepting that is part of operating at the institutional level.

How IRC Partners Structures the Approach for Developers

Most developers who come to IRC Partners have already tried to access family office capital on their own. They have strong projects and credible track records. What they're missing is the structural preparation and the access to the right allocators.

IRC structures the deal first, then raises. This is the core difference between IRC and a traditional placement agent. Before a single introduction is made, the capital stack is built, the waterfall is reviewed, the stress-case model is completed, and the governance framework is documented. The deal is packaged to institutional standard before it goes to market. This is why the repositioning process described in the case study above produced a result in 90 days rather than another six months of rejections.

IRC takes 3% to 5% advisory equity in each engagement, which means IRC's outcome is directly tied to the developer's outcome. There are no transaction fees that incentivize speed over structure. One engagement also covers all future raises through exit, so IRC functions as a permanent capital formation partner rather than a one-time broker. Through a network of 307,000+ institutional allocators and 77 global investment bank syndicate partners, IRC provides warm introductions to the specific family offices that actually write $10M+ checks, not the 87% that don't.

If you're navigating the broader institutional capital landscape, the complete framework in the IRC guide to raising $10M to $50M in institutional capital covers the full picture from capital stack architecture to LP selection. For developers ready to take the next step, apply to work with IRC Partners to discuss your current raise and whether the engagement model is the right fit.

Frequently Asked Questions

What do family offices look for in a real estate developer?

Family offices prioritize track record across market cycles, structural alignment, and governance clarity. While deal quality is important, the operator's institutional credibility is evaluated first. They look for waterfalls that hold up under stress and formal reporting protocols that mirror institutional standards.

How do I get a family office to invest in my deal?

Begin with a warm introduction through a trusted intermediary rather than cold outreach. Before the meeting, your materials must be institutional grade, including a fully structured capital stack and a stress-case model at 80 percent of projected net operating income. The deal must be fully packaged before it ever hits the market.

What is a deal-by-deal structure in real estate?

In a deal-by-deal structure, the Limited Partner commits capital to a specific, identified asset rather than a blind pool fund. This allows the family office to review and approve each investment individually. Currently, direct investments and club deals account for roughly 69 percent of family office real estate transactions.

How much do family offices typically invest?

Most family offices deploy between $1M and $5M per deal. Only about 13 percent of family offices write checks of $10M or more. If you are seeking $10M to $50M in equity, you must specifically target the subset of family offices with the mandate and liquidity to lead at that scale.

What is the difference between pitching a family office vs an HNWI?

High-Net-Worth Individuals often decide based on relationships and headline returns. In contrast, family offices require institutional documentation, including detailed waterfall mechanics and formal governance frameworks. They also have longer decision cycles, typically 60 to 120 days, and perform much deeper due diligence.

What documents do family offices require before investing?

Expect to provide audited financials from prior projects, a fully structured capital stack, a detailed waterfall schedule, and a stress-case underwriting model. You must also provide a governance framework that clearly outlines reporting cadences and partner consent rights.

What is a preferred return in a real estate deal?

A preferred return is the minimum return a partner must receive before the developer earns any profit split. For example, an 8 percent preferred return means the investor receives their 8 percent annual return before the developer profit split occurs. Family offices scrutinize whether the developer share kicks in before or after the investor has recovered their initial capital.

Most founders don't lose the raise because of the pitch. They lose it because the structure was wrong before the first investor call. IRC Partners advises founders raising $5M to $250M of institutional capital. 7 strategic partners per quarter. Start here to schedule a call with our team.

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.