.svg)

.png)

How to Structure a Capital Stack for a $10M-$50M Real Estate Development Deal

Institutional LPs pass on good deals every week. Not because the deal is bad. Because the capital stack doesn't answer the questions they need answered before they can say yes. Most developers never find out what those questions were. The LP just goes quiet, and the developer goes back to the drawing board wondering what went wrong.

This is the problem this article solves. If you're a seasoned developer raising $10M to $50M, leveraging professional real estate sponsor capital advisory ensures your project structure is built to the institutional standard. There's a difference, and it shows up in diligence every time. The Real Estate Developer's Guide to Raising $10M-$50M in Institutional Capital covers the full picture of what institutional LPs need to see. This article goes deep on one specific piece: how to build the capital stack itself.

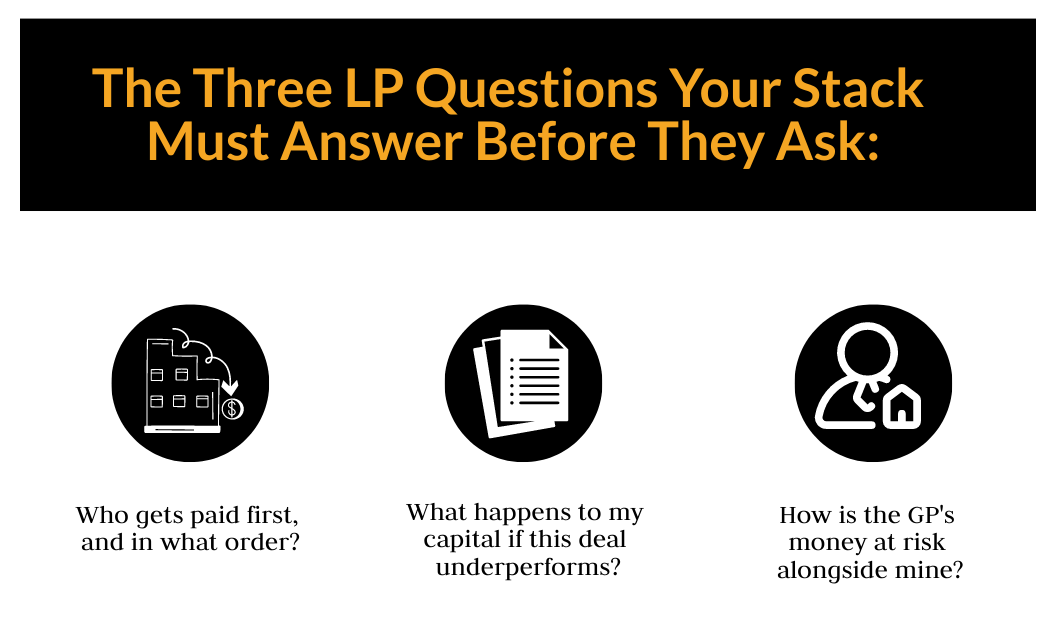

Every institutional LP, whether a family office, a private equity fund, or a structured debt provider, evaluates your stack through three questions:

The Three LP Questions Your Stack Must Answer Before They Ask:

- Who gets paid first, and in what order?

- What happens to my capital if this deal underperforms?

- How is the GP's money at risk alongside mine?

If your stack can't answer all three clearly, the LP will either pass or slow the process down while they dig for the answers themselves. Neither outcome is good. The developers who close $10M to $50M raises have stacks built to answer these questions before the LP opens the deck. Here's how to build one. You can also read our companion guide on how to choose a capital advisor for your institutional raise for context on the advisory side of this process.

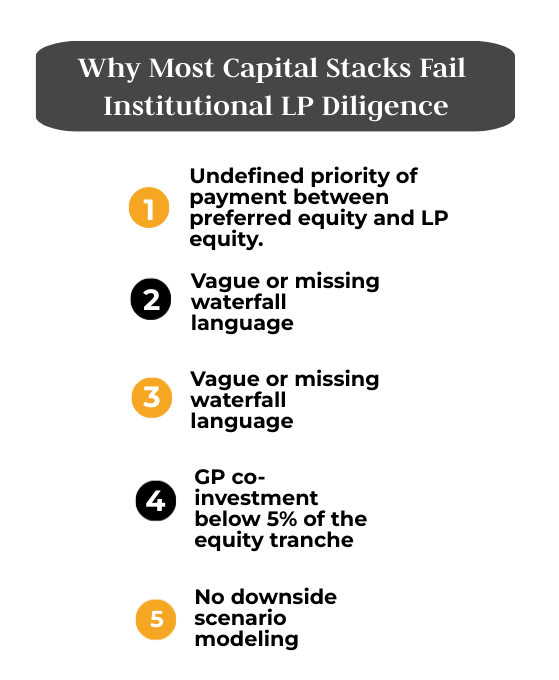

Why Most Capital Stacks Fail Institutional LP Diligence

The rejection is almost never about the deal itself. It's about what the stack signals to the LP about how the GP thinks. Here are the four structural mistakes that kill deals before the conversation gets serious.

- Undefined priority of payment between preferred equity and LP equity. Developers often layer in preferred equity without clearly defining where it sits relative to LP equity in the distribution order. Institutional LPs read this as either a lack of sophistication or a deliberate attempt to obscure the structure. Either way, the deal stalls. Every layer in the stack needs a defined position, and that position needs to be documented in the operating agreement, not just described in the deck.

- Vague or missing waterfall language. If your deck describes the waterfall in general terms ("LPs receive a preferred return before the GP participates in profits"), you've already lost ground with a sophisticated LP. They want to see the actual tier structure: the IRR hurdles, the promote percentages at each hurdle, the catch-up mechanics, and whether the structure is European or American style. Vague waterfall language signals that the GP hasn't done this at the institutional level before.

- GP co-investment below 5% of the equity tranche. According to industry benchmarks, GP co-investment typically ranges from 1% to 10% of total equity. Anything below 5% raises an alignment question immediately. The LP's internal logic is simple: if the GP doesn't have meaningful capital at risk, what keeps them focused when the deal gets hard? Co-investment is not just a number. It's a signal. Treat it like one.

- No downside scenario modeling. This is the mistake that kills the most deals at the $10M to $50M level. Developers present the base case and the upside. They skip the downside. Institutional LPs, especially family offices that have shifted to deal-by-deal structures in 2026, ask one question above all others: "What happens if things don't go to plan?" If you can't answer that with a model, the LP has to build it themselves. When they do, the deal slows and sometimes dies.

These four mistakes are structural, not strategic. They're fixable before you go to market. The 7 non-negotiables that institutional LPs require covers the broader diligence checklist. This article gives you the stack architecture to clear the structural bar.

The Four Layers of an Institutional-Grade Capital Stack

A $10M to $50M institutional stack has four layers. Each layer has a defined position, a defined provider, and a defined purpose. Skipping a layer or collapsing two layers into one is where most developer-built stacks break down under LP scrutiny.

Here's how to build the stack from the bottom up.

Layer 1: Senior Construction or Bridge Debt

This is the foundation of the stack. Senior debt sits in the first lien position, which means it gets paid back before any equity. For ground-up development, this is typically a construction loan from a commercial bank or a debt fund. For value-add deals, it may be a bridge loan.

Sizing: 50% to 65% of total project cost. Lenders at the institutional level rarely go above 65% LTC on ground-up deals in the current rate environment.

Layer 2: Preferred Equity or Mezzanine Debt

This layer fills the gap between what senior debt will fund and the total project cost. It's the most flexible layer in the stack and the one most often structured incorrectly. Preferred equity sits above LP equity in the priority of payment but below senior debt. Mezzanine debt works similarly but is structured as debt rather than equity.

Sizing: 10% to 20% of total project cost. This layer is often provided by a debt fund, a family office, or a structured credit vehicle.

Layer 3: LP Equity

This is the institutional capital you're raising. It sits above preferred equity in the upside distribution but behind it in the return of capital. Institutional LPs expect to hold 90% to 95% of the equity tranche, as confirmed by standard market structures tracked by Wall Street Prep's real estate waterfall framework.

Sizing: 25% to 35% of total project cost. The LP equity tranche is where the institutional raise lives.

Layer 4: GP Equity

This is your money. It represents 5% to 10% of the equity tranche, not 5% to 10% of total project cost. That's a meaningful distinction. On a $30M deal with a $7.5M equity tranche, a 10% GP contribution is $750,000. That's the skin-in-the-game number that institutional LPs are looking for.

The table below shows how these four layers typically size across a $10M to $50M deal:

Understanding the full picture of how these instruments interact is covered in depth in the capital stack explained guide. The key point here is that each layer must be defined, sized, and documented before you go to market.

Waterfall Mechanics: The Three-Tier Structure Institutional LPs Expect

The waterfall defines how money flows out of the deal. It's the most scrutinized part of the stack in institutional diligence. Vague waterfall language is one of the four structural mistakes covered earlier. Here's the specific structure institutional LPs expect to see.

Tier 1: Return of Capital Plus Preferred Return

All distributions go 100% to LPs until two things happen: their full capital contribution is returned and they've received their preferred return. The preferred return is the minimum annual return LPs receive before the GP participates in profits.

The institutional standard is an 8% preferred return, per benchmarks tracked by Wall Street Prep. Some structures use 6% to 7% for deals with stronger senior debt coverage. Some use up to 10% for higher-risk ground-up projects. For a $10M to $50M multifamily or industrial deal in 2026, 8% is the number to start with.

Key structural note: Institutional LPs strongly prefer European-style waterfalls. This means no promote is paid to the GP until all LP capital is returned plus the full preferred return is satisfied across the entire deal. American-style waterfalls, which pay promote on a deal-by-deal basis, are viewed as LP-unfavorable and will slow or kill institutional commitments.

Tier 2: The GP Catch-Up

Once the preferred return is satisfied, the catch-up provision kicks in. This is where most developer-built stacks leave money on the table.

Without a catch-up, the GP earns 0% of returns up to the preferred hurdle and only their promote percentage above it. With a 100% catch-up, all distributions after the pref go to the GP until they've received 20% of all profits generated above the return of capital. The difference in GP economics is significant.

A 100% catch-up is standard. A 50/50 catch-up is acceptable. No catch-up is a structural error that costs the GP real money.

Tier 3: Tiered Promote Based on IRR Hurdles

After the catch-up, remaining distributions are split based on tiered IRR hurdles. This is the promote structure that rewards the GP for outperformance.

The table below shows the institutional-standard tiered promote structure:

This tiered structure does two things. It protects the LP at the base case. And it gives the GP meaningful upside if the deal outperforms. That's the alignment structure institutional LPs are looking for.

GP Economics: How to Protect Your Promote Without Losing the LP

There's a common fear among developers going to institutional capital for the first time: that asking for a strong promote structure will turn off the LP. The opposite is true. A well-structured promote signals that the GP has done this before. It's vague or missing promote language that raises the red flag.

The most expensive mistake in GP economics isn't asking for too much promote. It's failing to include a catch-up provision and not knowing what that costs you.

Here's what the catch-up provision actually does to your economics. Take a $30M deal with a $7.5M equity tranche, an 8% preferred return, and a 20% GP promote. Assume the deal generates $4M in profits above the return of capital.

The difference is $600,000 to the GP on a single deal. Across a multi-deal development pipeline, this compounds significantly. Including a catch-up provision isn't aggressive. It's standard. LPs who work at the institutional level expect to see it.

The Three Rules of GP Economics at the Institutional Level

Rule 1: Co-invest at 5% to 10% of the equity tranche, minimum. GP co-investment in the 1% to 10% range is the institutional benchmark. Anything below 5% of the equity tranche triggers alignment questions. On a $7.5M equity tranche, 5% is $375,000. That's the floor.

Rule 2: Include the catch-up provision in the operating agreement, not just the deck. LPs will read the operating agreement. If the catch-up is described in the deck but not documented in the legal structure, it doesn't exist. Get it in the documents.

Rule 3: Use tiered promote, not a flat promote. A flat 20% promote above the pref is acceptable but leaves performance upside unaddressed. A tiered structure that steps up from 20% to 30% to 40% as IRR hurdles are cleared signals sophistication and rewards both parties for outperformance.

The 10 mistakes that kill institutional raises covers the broader pattern of errors developers make when going to institutional capital. The GP economics mistakes above are among the most common and the most fixable.

What a Properly Structured Stack Looks Like vs. a Common Mistake Pattern

The framework above is buildable. Here's what it looks like in practice on a $30M multifamily ground-up deal, compared to the mistake pattern that causes LP rejection.

Deal: $30M multifamily ground-up development, 18-month construction, 12-month stabilization.

The properly structured stack answers all three LP questions before they're asked. Who gets paid first: senior debt, then preferred equity, then LP equity, then GP equity. What happens if the deal underperforms: the downside model shows LP capital is protected through the senior debt position and preferred equity cushion. How is the GP's money at risk: $750,000 of GP equity sits in the same position as LP equity, losing value under the same conditions.

The mistake pattern doesn't answer any of those questions cleanly. It forces the LP to dig, and digging slows deals.

Downside Scenario Modeling: The Question LPs Ask That Most GPs Can't Answer

Most developers can answer the base case question in their sleep. Revenue projections, NOI, cap rate, exit valuation. They've run those numbers a hundred times. The question institutional LPs ask that most GPs can't answer is simpler: "Show me what happens if this deal doesn't go to plan."

In 2026, family offices and institutional allocators have made downside modeling a primary diligence requirement. They've seen too many deals underperform at the base case. They want to know the GP has thought through the failure scenarios before asking for a commitment.

The four scenarios to model before you go to market:

- Base case. The deal performs as underwritten. LP receives 8% pref plus their share of the tiered promote. GP receives catch-up plus promote at each IRR hurdle.

- 15% cost overrun. Construction costs run 15% over budget. Model the impact on LP returns, GP equity, and the pref coverage ratio. Show that LP capital is still protected by the senior debt and preferred equity cushion.

- 12-month lease-up delay. Stabilization takes 12 months longer than projected. Model the cash flow gap, the impact on IRR, and whether the preferred return still gets paid. Show the reserve structure that covers the gap.

- 20% NOI shortfall at stabilization. The property stabilizes at 80% of projected NOI. Model the exit valuation impact, LP returns, and GP promote. Show the LP what happens to their capital in this scenario.

The goal of downside modeling isn't to show the LP that nothing can go wrong. It's to show them that you've already thought through what happens when things do. That's the alignment signal that closes deals.

Build the Stack Before You Go to Market

The framework in this article is buildable. Four defined layers. A European-style waterfall with an 8% preferred return. A 100% catch-up provision. Tiered promote based on IRR hurdles. GP co-investment at 5% to 10% of the equity tranche. Downside scenarios modeled before the first LP conversation.

That's the stack that passes institutional diligence at the $10M to $50M level. It's not complicated. But most developers don't build it before they go to market. They build it during diligence, under pressure, while the LP is waiting. That's the wrong order.

The developers who close institutional raises at this level structure first, then raise. The structure is what creates the LP's confidence to commit. The raise is what follows.

If you're ready to structure your capital stack for an institutional raise, IRC Partners works with experienced developers to architect the stack, align the LP economics, and coordinate introductions to institutional allocators who write $10M+ checks. We structure the deal first. That's the order that works.

For the broader context on how institutional allocators evaluate developers at this stage, read How to Find Investors for a $20M+ Raise in 2026. For a complete picture of what it takes to raise $10M to $50M from institutional LPs, start with the Real Estate Developer's Guide to Raising Institutional Capital.

Apply to work with IRC Partners to structure your capital stack and get your deal in front of the right institutional allocators.

Frequently Asked Questions

What is a preferred return in a real estate capital stack?

A preferred return is the minimum annual return that limited partners receive before the general partner participates in any profits. In institutional real estate deals, the standard preferred return is 8 percent internal rate of return. It is calculated based on the investor capital contribution and must be satisfied in full before the developer earns any profit split.

What is a waterfall structure in real estate?

A waterfall structure defines the specific order in which profits are distributed between investors and the developer. It typically flows through distinct tiers: return of initial capital, preferred return, developer catch-up, and tiered profit splits based on internal rate of return hurdles. Institutional partners require a documented waterfall in the operating agreement to ensure payment priority is clear.

What is the difference between preferred equity and LP equity?

Preferred equity sits between senior debt and common equity in the priority of payment. It earns a fixed return and is repaid before the limited partner equity in a downside scenario. Limited partner equity participates in the full upside above the preferred return and the developer profit split. Confusing these two layers is a common structural mistake in developer-built capital stacks.

How much should a developer contribute to a deal?

The developer co-investment should be 5 percent to 10 percent of the equity tranche, not the total project cost. For a deal with a 7.5M dollar equity tranche, the institutional floor is 375,000 to 750,000 dollars. Anything below this range often raises alignment concerns with institutional partners who want to see significant skin in the game.

What is a catch-up provision in a real estate waterfall?

A catch-up provision allows the developer to receive a disproportionate share of distributions after the preferred return is met. This continues until the developer has received their target profit split percentage of all distributions made up to that point. In a large development deal, a 100 percent catch-up provision can significantly impact developer economics.

What is the difference between European and American waterfalls?

A European-style waterfall requires the developer to return all investor capital plus the full preferred return across the entire fund before receiving any profit split. An American-style waterfall allows the developer to collect a profit split on individual deals as they close. Institutional partners strongly prefer the European-style structure for fund investments to mitigate risk.

How do I structure a capital stack for a 10M to 50M dollar deal?

Aim for four distinct layers: senior debt at 50 to 65 percent, preferred equity or mezzanine at 10 to 20 percent, limited partner equity at 25 to 35 percent, and developer equity at 5 to 10 percent of the equity tranche. Use an 8 percent preferred return and ensure all terms are documented in the formal operating agreement rather than just the pitch deck.

This isn't for pre-revenue companies or first-time founders. It's for operators at $1M+ ARR, raising $5M to $250M of institutional capital, who've done this before and want the next round architected right. If that's you, schedule a call to discuss HERE.

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.