.svg)

.png)

How to Compare Real Estate Capital Advisory Firms for a $50M Raise

Most developers spend more time negotiating an advisory firm's fee than evaluating whether that firm can actually close the raise. At $50M, that's a costly mistake.

The real cost of choosing the wrong advisory firm isn't the fee. It's the raise itself. A failed $50M raise signals to the institutional market that the deal couldn't close. The next attempt starts from a weaker position.

The good news: the criteria that separate firms that close $50M raises from those that don't are specific and testable. They have almost nothing to do with fee percentage or the size of a contact list.

If you're working through the broader question of how to structure and position a raise at this scale, the Real Estate Developer's Guide to Raising $10M-$50M in Institutional Capital covers the full picture. If you came here from our breakdown of how IRC's structure-first model works in practice, this article delivers the comparison framework that article references.

This is a four-criteria framework. Run any advisory firm through it. The answers will tell you everything you need to know in about 20 minutes.

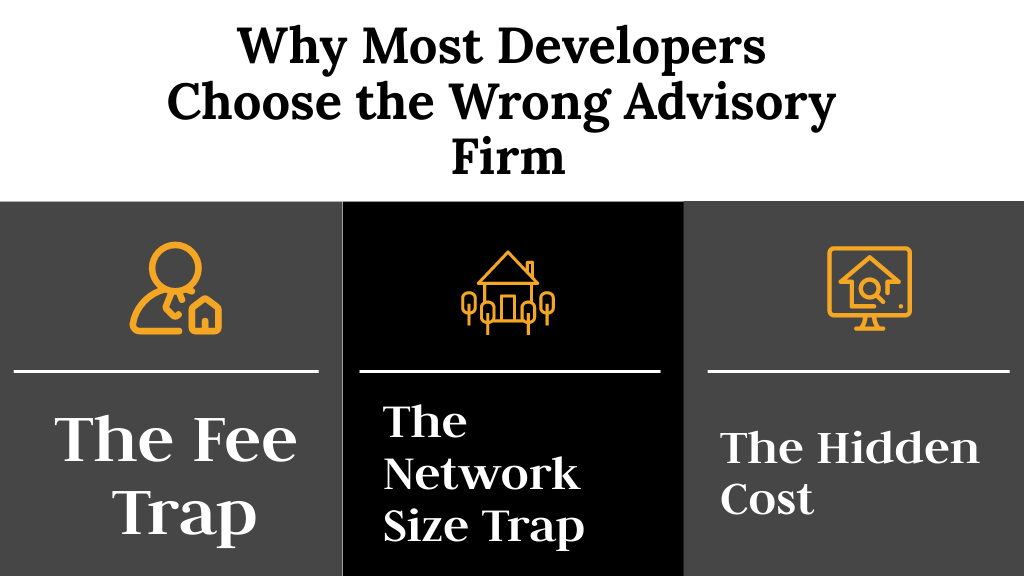

Why Most Developers Choose the Wrong Advisory Firm

There are two proxies most developers use when evaluating advisory firms. Both are the wrong signal at the institutional level.

The Fee Trap

Fee percentage is a measure of cost, not outcome. A firm charging 1% that fails to close the raise costs far more than a firm charging 4% that closes in eight months. Yet most developers open the conversation with "what's your fee?" and let the answer anchor the entire evaluation.

The fee structure does matter, but not in the way most developers think. The question isn't how low the fee is. It's whether the firm's compensation is tied to the developer's outcome or to the transaction itself. According to PipelineRoad's breakdown of capital raising fee structures, placement agents typically charge 1-3% of capital raised plus a monthly retainer, collecting fees regardless of whether the raise ultimately closes. A firm holding advisory equity only wins when the developer wins.

The Network Size Trap

A contact list of 300 family offices sounds impressive. It usually isn't.

Only about 13% of family offices deploy $10M or more per deal. According to Thesis Driven's analysis of family office types and check sizes, the majority of single-family offices without dedicated real estate teams write $2M-$10M checks, while only large multi-family offices and institutional-grade single-family offices consistently deploy $10M or more per deal. A firm with 300 contacts but no qualification process is broadcasting to the wrong audience. That's not a network. That's noise.

At the $50M level, allocator quality matters more than allocator quantity. The developer needs warm introductions to the specific subset of institutional allocators who write $10M+ checks in their asset class. Not a mass outreach to everyone on a list.

The Hidden Cost

A failed raise doesn't just waste 12 months. It creates a market signal. Institutional allocators talk. If a deal was shopped widely and didn't close, the next firm you hire starts from a worse position. The cost of choosing the wrong advisory firm compounds across every future raise.

This is why the evaluation framework matters. The right questions reveal whether a firm is built to close or built to collect a retainer.

The Four Criteria That Actually Predict Whether a Raise Closes

These four criteria apply to any advisory firm, regardless of how they present themselves. Ask each question directly. Vague answers are answers.

1. Deal-First vs. Raise-First

The most important structural question in the evaluation. Does the firm architect the capital stack before approaching allocators, or do they go to market first and adjust the structure based on feedback?

A raise-first firm pitches the deal to allocators and revises the structure when it gets rejected. This is backwards. Institutional LPs are doing more diligence in 2026 than at any point in the past decade. They're asking "what happens if this doesn't go to plan?" before they ask about returns. A deal that goes to market without a properly structured capital stack, clear waterfall mechanics, and aligned LP economics will get rejected by the allocators who matter most.

A deal-first firm builds the structure before the first introduction. That structure becomes the answer to the LP's diligence questions, not something that gets revised mid-process.

Test question: "Walk me through how you would structure my specific deal before you approach any allocators. What does that process look like and how long does it take?"

A firm that jumps to "here's our network" before answering this question is a raise-first firm.

2. Incentive Alignment

How a firm gets paid determines what they optimize for. This is not a subtle distinction.

A firm earning a retainer plus a success fee is compensated for moving quickly. Speed is their incentive, not outcome. If the deal doesn't close, they've still collected the retainer. The developer absorbs the entire downside.

A firm taking advisory equity has no exit unless the developer's raise succeeds. Their incentive is aligned with the developer's long-term outcome, not the speed of the transaction. This structure also changes the quality of advice. A firm with equity in the outcome will tell you when the deal isn't ready. A retainer-only firm rarely will.

Test question: "How are you compensated if the raise doesn't close? Walk me through your fee structure in a scenario where we go 12 months without a close."

3. Allocator Access Quality

Network size is a vanity metric. The relevant question is whether the firm has relationships with allocators who are actively deploying $10M+ in the developer's asset class right now.

Understanding how institutional capital stacks are structured helps clarify what allocators actually need to see before committing at this level. The point is that a $50M multifamily raise and a $50M industrial raise require access to different allocator subsets. A generalist network doesn't solve that problem.

Test question: "Can you name five family offices or PE funds that have deployed $10M or more in my asset class in the last 12 months? And can you get a warm introduction to each of them?"

If the answer is vague, the network isn't qualified.

4. Engagement Scope

A single-transaction engagement is a structural mismatch for a developer building a multi-raise pipeline. The best advisory relationships are embedded across multiple raises, not reset after each one.

A firm that exits after the first close leaves the developer to restart the process for the next project. Every future raise loses the institutional relationships built during the first one. A firm that stays engaged across multiple raises builds cumulative access, refines the capital stack with each project, and becomes a durable part of the developer's capital formation strategy.

Test question: "Does this engagement cover future raises, or does it end when this raise closes?"

Transactional Broker vs. Capital Advisory Partner: The Real Difference

The terms "placement agent," "capital advisor," and "capital advisory partner" are often used interchangeably. They describe fundamentally different models.

The table above isn't a judgment. Some developers at earlier stages or with simpler capital needs will find a transactional broker perfectly adequate. But at $50M, the stakes change. Institutional allocators at this level are running deeper diligence. They're evaluating the structure, the waterfall, the LP economics, and the developer's track record. Going to market without those elements buttoned down is how raises stall.

What the Difference Looks Like in Practice

Consider a multifamily developer who had spent 14 months working with a traditional placement agent on a $35M raise. The agent had a large contact list and moved fast. The deal went to 200+ family offices. It didn't close. The structure kept getting revised based on LP feedback. Each revision signaled to the market that the deal was unsettled.

The developer reengaged with a capital advisory firm. The first three months were spent restructuring the capital stack: waterfall mechanics and preferred return tiers, LP co-investment rights, and a clear downside scenario analysis. Only then did introductions begin, to 18 qualified allocators who had deployed in the multifamily space in the prior 12 months. The raise closed in eight months.

The difference wasn't the network. The prior firm had a bigger one. The difference was structure first.

Review the 7 non-negotiables that institutional LPs evaluate before any raise at this level. The list maps directly to what a deal-first advisory firm prepares before approaching allocators.

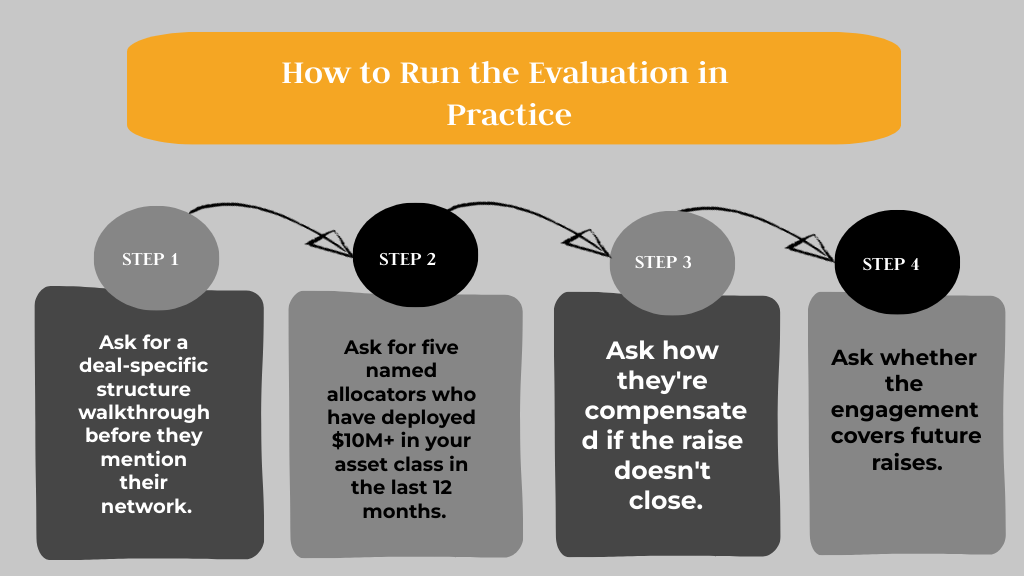

How to Run the Evaluation in Practice

Most advisory firms present well in the first meeting. They have polished decks, credible track records, and confident answers to broad questions. The four criteria only reveal themselves when you ask specific questions that can't be answered with a pitch.

Here's how to run the evaluation:

Step 1: Ask for a deal-specific structure walkthrough before they mention their network.

Tell the firm your deal type, asset class, raise size, and target LP profile. Then ask: "Before we talk about who you know, walk me through how you would structure this deal." A deal-first firm will engage immediately. A raise-first firm will pivot back to their network.

Step 2: Ask for five named allocators who have deployed $10M+ in your asset class in the last 12 months.

Not a category. Not "we have relationships with family offices." Five specific names, with specific recent deployment in your asset class. If they can't provide this, their network isn't qualified for your raise.

Step 3: Ask how they're compensated if the raise doesn't close.

This is the single most revealing question in the evaluation. A retainer-only firm has already been paid regardless of outcome. A firm with advisory equity has nothing until you close. The answer tells you whose side they're on when the raise gets hard.

Step 4: Ask whether the engagement covers future raises.

A firm that exits after the first close is a transactional firm. Period. A capital advisory partner who understands your pipeline, your track record, and your LP relationships is worth more on raise three than raise one. Ask explicitly whether the engagement structure extends to future projects.

These four questions take about 20 minutes. Any firm that can answer all four clearly and specifically is worth a deeper conversation. Any firm that deflects, generalizes, or pivots to their pitch deck is telling you exactly what you need to know.

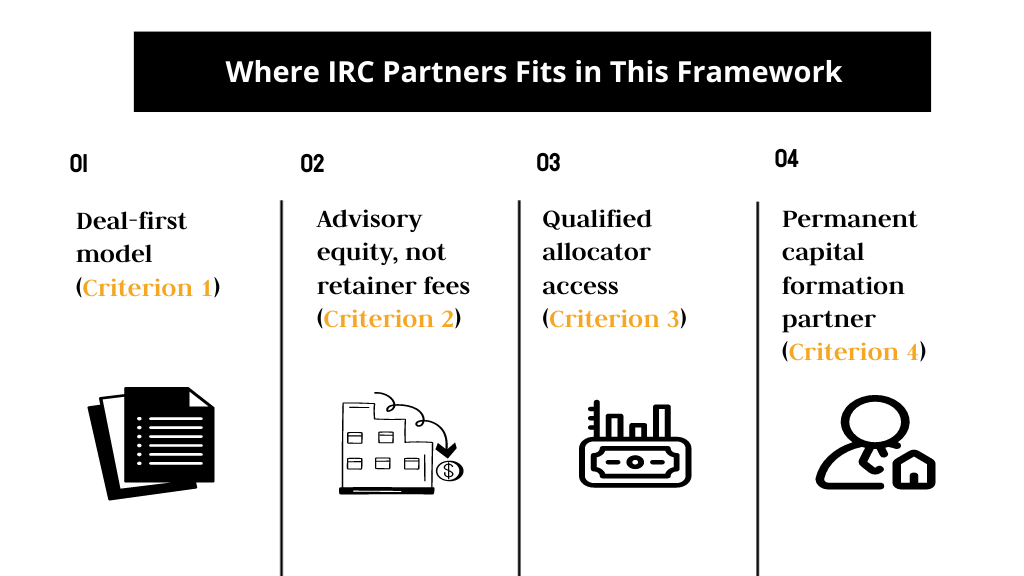

Where IRC Partners Fits in This Framework

Run IRC Partners through the same four criteria.

- Deal-first model (Criterion 1). IRC structures the capital stack before any allocator introduction. That means waterfall mechanics, preferred return tiers, LP alignment, and downside scenario modeling are complete before the first conversation with a family office or PE fund. The structure is the pitch, not something that gets revised after LP feedback.

- Advisory equity, not retainer fees (Criterion 2). IRC takes 3-5% advisory equity in each engagement. There is no retainer. There is no success fee on a failed raise. IRC's compensation is tied directly to the developer's outcome. The firm wins when the developer closes. That alignment changes the nature of the advisory relationship from the first day.

- Qualified allocator access (Criterion 3). IRC's network includes 307,000+ institutional allocators and 77 global investment bank syndicate partners. More importantly, the introductions are curated, not broadcast. IRC coordinates warm introductions to the subset of family offices and PE funds actively deploying $10M+ in the developer's asset class. The $17B+ in family office demand that requests deal referrals from IRC reflects allocators who are actively looking, not passively listed in a database.

- Permanent capital formation partner (Criterion 4). One IRC engagement covers all future raises through exit. The developer doesn't restart the process for each new project. IRC stays embedded, building on the LP relationships, capital stack refinements, and market positioning developed in each prior raise.

IRC accepts a limited number of new developer engagements each quarter, by application only. That constraint is intentional. It's what makes the model work.

Conclusion: The Framework Is the Filter

Any advisory firm that can answer the four test questions clearly and specifically is worth serious consideration. Any firm that can't is a transactional broker, regardless of how they describe themselves.

At $50M, the advisory firm you choose is as consequential as the deal itself. A failed raise at this level doesn't just cost you the project. It costs you market positioning for every raise that follows.

The framework in this article applies to every firm you evaluate, including IRC. If you're ready to run that conversation, IRC's engagement model is application-only. A limited number of new developer relationships are accepted each quarter, and the process starts with a structured deal review, not a pitch.

For developers building a multi-raise institutional pipeline, the right advisory partner is worth more on raise three than raise one. That's the standard to hold any firm to.

For a broader look at how institutional capital markets are shifting for real estate developers in 2026, the complete guide to raising $10M-$50M in institutional capital covers market context, LP behavior, and capital stack strategy in full. If you're evaluating what your deal needs before going to market, start there.

Frequently Asked Questions

What does a real estate capital advisory firm do?

A real estate capital advisory firm structures the developer capital stack, prepares the deal for institutional investor due diligence, and coordinates introductions to qualified allocators. Unlike a placement agent, which focuses primarily on outreach, an advisory firm prioritizes deal architecture to ensure the structure is sound and defensible before approaching investors.

How much does a real estate capital advisory firm charge?

Transactional brokers typically charge a retainer plus a 1 to 3 percent success fee on capital raised. Equity-aligned advisory firms instead take 3 to 5 percent advisory equity with no retainer. This aligns the advisor success directly with the developer long-term project outcome rather than the speed of the transaction.

What is the difference between a placement agent and a capital advisor?

A placement agent acts as a connector on a per-transaction basis for a cash fee. A capital advisor acts as a strategic partner who builds the deal structure first, then facilitates introductions to a curated set of qualified allocators. Their role often extends through the close and into support for future raises.

What do institutional investors look for in a 50M dollar real estate deal?

Beyond returns, institutional partners evaluate waterfall mechanics, preferred return tiers, and the developer track record. In 2026, they are hyper-focused on downside scenarios, specifically how the structure handles slower lease-up periods or cap rate compression.

How do I know if my deal is ready for institutional capital?

Your deal is ready when the capital stack is fully structured, investor economics are defined, and you have a quantifiable downside strategy. If you cannot articulate what happens if projections are not met without needing to rework the deal, it is not yet ready for institutional introductions.

What is advisory equity and how does it work?

Advisory equity is a 3 to 5 percent ownership stake taken by the firm in lieu of cash fees. The firm only earns a return if the project succeeds and generates returns for the developer. This creates a skin in the game environment that mirrors the relationship between the developer and the investor.

What is the right raise size to engage a capital advisory firm?

Advisory firms specializing in institutional capital usually focus on raises of $10M and above. The value proposition is strongest in the $25M to $75M range, where deal complexity and the need for rigorous allocator qualification become the primary barriers to success.

Most founders don't lose the raise because of the pitch. They lose it because the structure was wrong before the first investor call. IRC Partners advises founders raising $5M to $250M of institutional capital. 7 strategic partners per quarter. Start here to schedule a call with our team.

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.