.svg)

.png)

Capital Stack Risk Reduction Strategies: 5 Ways Developers Can Lower Risk Before a $10M+ Raise

Capital Stack Risk Reduction Strategies: 5 Ways Developers Can Lower Risk Before a $10M+ Raise

Most developers approach capital stack risk the same way: cut the leverage ratio and call it conservative. That instinct is understandable, but it misses the real problem. A stack with 55% LTV and aggressive mezzanine terms, a short cure window, and a cash-pay requirement that kicks in at month six can be far more dangerous than a 65% LTV structure that was built with extension flexibility and a patient capital partner.

In 2026, that distinction matters more than it has in years. According to the Mortgage Bankers Association, roughly $875 billion in commercial mortgages are maturing this year. The Federal Reserve’s Senior Loan Officer Opinion Survey confirms that construction and land development loans face modest tightening while broader standards hold. Senior lenders are no longer extending troubled deals on goodwill alone. They are stress-testing structures before agreeing to anything.

For developers raising $10M or more in institutional capital for real estate sponsors, this is the environment that exposes weak stack design. The full framework for understanding how each layer fits together is covered in Structuring the Capital Stack for $10M+ Real Estate Deals. The Deloitte 2026 Commercial Real Estate Outlook notes that 75% of real estate leaders plan to increase investment this year, but capital providers are simultaneously becoming more selective on structure, not less. This article goes one level deeper: given that you already understand the hierarchy, here are five structural levers you can actually control to reduce risk before the raise closes.

The five risk-reduction levers covered in this guide:

- Layer substitution: swapping a higher-risk layer for a structurally safer one

- Document negotiation: tightening the terms that determine how fast a problem becomes a crisis

- Equity cushion sizing: building enough true common equity to survive a bad year

- Waterfall engineering: structuring promote thresholds and rescue capital before stress hits

- Capital provider selection: choosing partners whose behavior under pressure matches the deal's risk profile

1. Layer Substitution: Replace the Wrong Risk With a Safer Kind of Risk

Layer substitution is not about removing debt from the stack. It is about identifying which layer is creating the most structural fragility and replacing it with one that behaves better under pressure.

The question is not "how much debt?" It is "does this layer create refinance pressure, cash-pay strain, or control risk at a point in the business plan when the deal is most vulnerable?"

Outperforming operators in today's market are underwriting closer to 55-65% LTV rather than the 75%+ leverage ratios that were common before 2022. But the leverage ratio alone does not determine risk. A developer who replaces high-coupon, short-duration mezzanine with a more patient structured equity source may increase headline cost of capital while materially reducing execution risk. That trade is often worth making.

For a deeper look at how each layer compares on cost, control, and position, see Senior Debt vs. Mezzanine vs. Preferred Equity: Which Layer Do You Actually Need?.

The substitution test: before finalizing any layer, ask whether the risk it introduces is one you can manage if the business plan runs 6-12 months long. If the answer is no, the layer is a candidate for substitution.

2. Document Negotiation: Risk Lives in the Paper Before It Shows Up in the Model

Two capital stacks can look nearly identical on a term sheet summary and have completely different risk profiles once you read the actual documents. The coupon rate gets attention. The cure period, the removal right, the cash-pay trigger, and the consent threshold usually do not, until something goes wrong.

The end of the "extend and pretend" era makes this more urgent. Lenders and preferred equity providers who once tolerated plan slippage informally are now enforcing documents as written. That means the terms a developer accepts at close are the terms they will live with under stress.

Key document negotiation levers

Cure periods

- What it is: the window a developer has to fix a default or covenant breach before the capital provider can exercise remedies

- Why it matters: a 10-day cure period on a construction draw delay is a trap. A 30-60 day cure period gives the development team time to solve the actual problem

- Target: negotiate the longest cure period the provider will accept, and push for notice-plus-cure rather than automatic trigger

Removal rights

- What it is: the preferred equity or mezz provider's right to remove the GP or take operational control on default

- Why it matters: removal rights that trigger on technical defaults, not just payment failures, give the capital provider enormous leverage in a renegotiation

- Target: limit removal rights to material, uncured payment defaults or fraud, not operational or reporting covenants

Cash-pay requirements

- What it is: whether the coupon must be paid in cash on a set schedule or can accrue (PIK) during the business plan

- Why it matters: a hard cash-pay requirement during a lease-up or construction period can create a liquidity crisis independent of asset performance

- Target: negotiate PIK optionality for at least the construction and initial stabilization period

Consent thresholds

- What it is: decisions that require capital provider approval before the developer can act

- Why it matters: overly broad consent rights slow decision-making and give providers informal leverage during amendments

- Target: limit consent rights to major capital events, not routine operational decisions

Key insight: the most dangerous terms in a capital stack are rarely the ones with the highest headline cost. They are the ones that transfer control fastest when the plan slips by a quarter.

3. Equity Cushion Sizing: Enough True Common Equity to Pass the Bad-Year Test

Equity cushion sizing is not about hitting a round number. It is about building enough true common equity to accomplish three specific jobs: satisfy a senior lender's extension logic, absorb a meaningful valuation decline, and preserve optionality if the business plan needs more time or more capital.

In practice, equity portions in middle-market deals have been growing. Data from Q4 2025 shows equity portions reaching 60.6% of deal structure in middle-market transactions, up from 59.2% in Q4 2024. That shift is not coincidental. Developers and their advisors are sizing cushions against what actually happens in a stressed scenario, not just what the base case model shows.

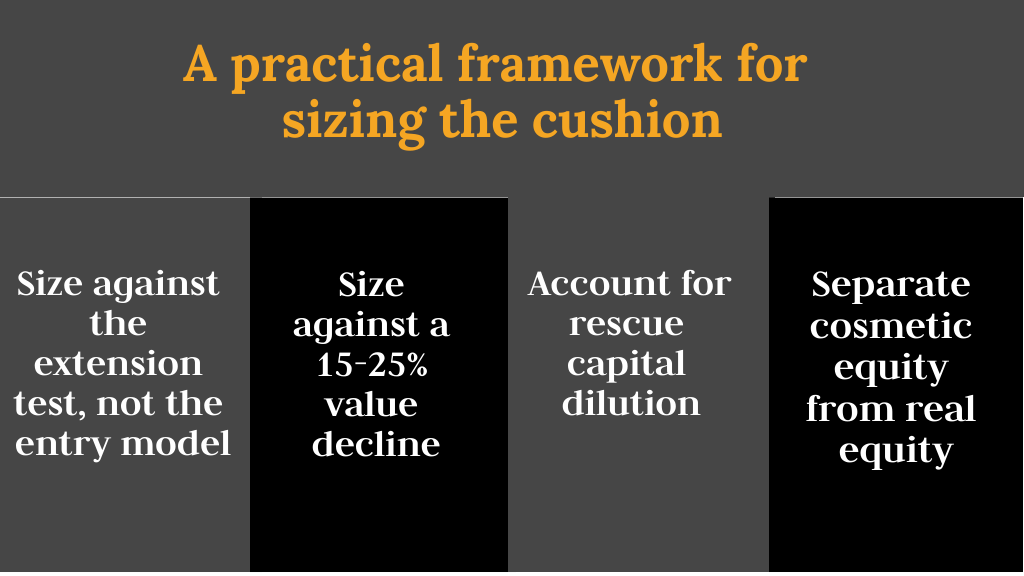

A practical framework for sizing the cushion

1. Size against the extension test, not the entry model Senior lenders grant extensions based on whether the remaining equity can absorb further value deterioration and still leave the loan in a defensible position. Model the downside case first and ask whether the common equity still provides meaningful protection at that level.

2. Size against a 15-25% value decline For ground-up and transitional deals, a 15-25% reduction in stabilized value is a reasonable downside scenario in the current market. If that decline wipes out the common equity layer entirely, the senior lender has no reason to extend.

3. Account for rescue capital dilution If the deal needs additional capital during the business plan, where does it come from and at what cost? A cushion that looks adequate at entry can become inadequate if rescue capital enters at a punitive priority. Size the initial cushion to leave room for a recapitalization without destroying GP economics.

4. Separate cosmetic equity from real equity Promoted interest, deferred fees, and GP co-invest that is immediately leveraged do not provide the same cushion as clean LP equity. Senior lenders look through structure. The cushion that matters is the one that absorbs losses before the senior loan is impaired.

Key insight: a thinner stack with a higher headline IRR can underperform a better-cushioned structure the moment an extension or amendment conversation begins. Position in the stack matters more than projected return when the lender is deciding whether to cooperate.

4. Waterfall Engineering: Protect GP Economics Before the Deal Gets Stressed

Most developers think about the waterfall as an upside-sharing mechanism. It is also a downside-governance document. How the waterfall is built determines whether the GP keeps meaningful economics if the deal needs more time, more capital, or a restructured timeline.

The decisions that matter most are made before the deal closes, not after the stress arrives. For a detailed analysis of how each layer behaves under stress and which combinations best protect GP economics, see Which Capital Stack Layers Are Best for Minimizing Risk?. This section focuses on what to build into the waterfall proactively.

Common waterfall choices and their tradeoffs

Protective provisions to address before launch

- Define rescue capital rights and priority before the deal closes, even if rescue capital is never needed

- Include a GP cure right that allows the GP to contribute additional capital to protect the promote before an LP can trigger a forced sale or recap

- Avoid waterfalls that reset the preferred return clock if the business plan extends beyond the original term

- Negotiate a promote that vests progressively rather than only at final exit, so partial value creation is recognized if the deal is recapitalized mid-hold

Key insight: rescue capital negotiated at the closing table costs far less than rescue capital negotiated after a covenant breach. Structuring for the bad outcome before it happens is the single most underused risk-reduction tool available to a developer.

5. Capital Provider Selection: The Wrong Partner Can Turn a Manageable Issue Into a Crisis

Provider selection is the most underestimated risk lever in a capital raise. Most developers evaluate capital providers on rate, proceeds, and speed. Those are pricing variables. Behavior under stress is a different variable entirely, and it is rarely visible from a term sheet.

According to the Deloitte 2026 Commercial Real Estate Outlook, lenders and investors are increasingly broadening services across the capital stack, integrating preferred equity and mezzanine debt under single platforms. That trend creates more structuring options, but it also concentrates behavioral risk. A provider who controls multiple layers of the same deal has more leverage in a restructuring conversation.

A provider with a slightly higher coupon but a history of working constructively through plan changes may reduce total deal risk more than the cheapest term sheet in the market.

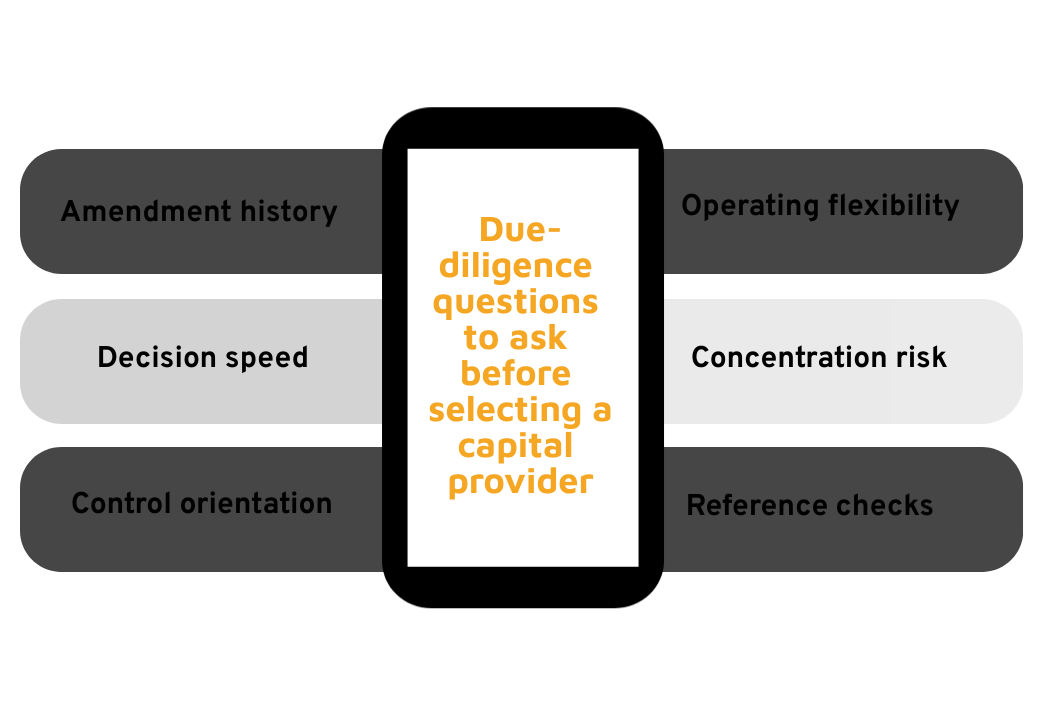

Due-diligence questions to ask before selecting a capital provider

- Amendment history: has this provider amended deals when the business plan stretched, or do they accelerate remedies at the first opportunity?

- Decision speed: how quickly does the provider respond during a crisis? Slow amendment approvals can turn a solvable problem into a default.

- Control orientation: does the provider seek operational control rights beyond what the documents require, or do they stay in a passive position when the deal is performing?

- Operating flexibility: will the provider allow lease modifications, capital expenditure changes, or partnership restructuring without triggering consent rights?

- Concentration risk: does this provider hold multiple layers of the stack? If yes, what is their track record when both layers are under pressure simultaneously?

- Reference checks: talk to other developers who have been through a stressed or extended deal with this provider, not just ones who had clean exits

The bottom line: the best time to understand how a capital provider behaves under stress is before you close with them. That diligence is harder to do alone, which is why experienced developers increasingly rely on advisors with direct market relationships to inform provider selection before the term sheet is signed.

An IRC Example: How Stack-Structuring Discipline Changes the Outcome

The five levers above are not theoretical. They are the kind of decisions that determine whether a deal stays financeable when the market, the timeline, or the capital markets environment shifts.

IRC Partners served as capital advisor on a multifamily development in Texas with a total capitalization of $150 million. The structuring work on that engagement focused on aligning capital layers, negotiating document terms, and selecting providers whose behavior under a stretched timeline would not create a secondary crisis. The goal was a stack that would still work if the business plan ran long, not just a stack that worked in the base case.

That kind of structural discipline, applied before the raise closes, is what separates deals that survive plan changes from deals that do not. The structure is the strategy.

For developers who want to understand the common structural mistakes that surface during institutional raises, 10 Mistakes That Kill Your Institutional Raise covers the patterns IRC sees most often across engagements.

The best time to reduce capital stack risk is before the raise closes. Once the documents are signed, the structural decisions are made.

Before launching materials or circulating a draft term sheet, work through these five steps:

- Audit the stack for each of the five levers. Identify which layers, terms, waterfall provisions, and providers are creating the most structural fragility.

- Model the downside case first. Size the equity cushion, test the extension logic, and stress the waterfall against a scenario where the business plan runs 12 months long.

- Read the documents, not just the term sheet. Cure periods, removal rights, and consent thresholds are where real risk lives.

- Diligence the provider, not just the price. A cheaper coupon from a difficult provider is not a better deal.

- Engage a capital advisor before the raise, not after the first problem. Stack structuring is harder to fix mid-raise than it is to get right at the start.

IRC Partners works with developers before the raise to structure a more durable stack and protect GP economics. If the next raise is on the horizon, that conversation is worth having early.

Frequently Asked Questions

What are the most effective capital stack risk reduction strategies?

The most effective strategies are layer substitution, document negotiation, equity cushion sizing, waterfall engineering, and provider selection. While reducing leverage is important, structural decisions regarding cure periods and provider behavior often dictate whether a deal survives a plan change more than the headline loan-to-value ratio does.

How do I reduce mezzanine risk in my capital stack?

Mezzanine risk is mitigated by negotiating longer cure periods and limiting removal rights to material payment defaults. Additionally, pushing for Payment-in-Kind (PIK) optionality during the construction or lease-up phase provides a cash-flow buffer that prevents a technical default during temporary dips in liquidity.

How do I negotiate preferred equity terms to reduce risk?

Focus on four key provisions: cure period length, removal right triggers, cash-pay versus PIK flexibility, and consent thresholds. A preferred equity position with 30 to 60 day cure periods and removal limited strictly to uncured defaults is structurally safer than one with aggressive cash-pay requirements and broad operational vetoes.

How much equity cushion do I need for an institutional deal?

The cushion should be sized to absorb a 15 to 25 percent valuation decline without wiping out the common equity layer. It must be sufficient to satisfy a senior lender extension logic and leave room for rescue capital. Always distinguish between clean limited partner equity and cosmetic equity that provides no real loss absorption.

How do I protect developer economics in a waterfall if the deal gets stressed?

Address rescue capital terms and profit split vesting before closing the initial round. Pre-negotiating the priority of rescue capital is far cheaper than doing so after a covenant breach. Furthermore, ensure the waterfall does not reset the preferred return clock upon loan extensions, which can exponentially increase the investor hurdle.

What is the biggest risk in a capital stack that developers overlook?

Document terms. While developers often fixate on the interest rate and total proceeds, it is the cure periods and consent thresholds that determine how quickly a minor plan slip escalates into a control event. Two stacks with identical pricing can have vastly different risk profiles based on the fine print.

How do I evaluate a capital provider behavior under stress before closing?

Request references from developers who navigated stressed or extended deals with that specific provider, not just those with clean exits. Inquire about their decision speed during a crisis and their willingness to amend terms versus seeking immediate control rights. This due diligence on the partner is as important as their due diligence on your project.

Continue reading this series:

- Structuring the capital stack for $10M+ real estate deals

- Senior debt vs. mezzanine vs. preferred equity: which layer do you actually need?

- Which capital stack layers are best for minimizing risk?

IRC Partners advises founders raising $5M to $250M of institutional capital on structure, positioning, and round architecture. 7 strategic partners per quarter. No placement agent model. No success-only theater. If you want a structural review of your current raise, apply at HERE

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.