.svg)

.png)

Structuring the Capital Stack for $10M+ Real Estate Deals

Structuring the Capital Stack for $10M+ Real Estate Deals

To structure a $10M+ real estate capital stack that gets funded today, developers must precisely sequence five layers: senior debt anchored at 50–60% loan-to-cost (LTC), a mezzanine or preferred equity gap layer priced at 12–16%, LP equity targeting 15–25%+ IRR, and GP equity of at least 5% of total project cost.

Navigating this complexity requires specialized capital advisory for real estate sponsors to ensure the stack is stress-tested against cost overruns, extended lease-ups, and interest rate shocks before outreach begins. Sponsors who skip this disciplined sequencing and go to market with a fragmented structure are rarely rejected because the underlying deal is bad—they are rejected because the structure is.

Institutional capital is highly available, with private credit platforms sitting on record dry powder and family offices actively deploying capital. However, accessing these funds is more structure-sensitive than in any prior real estate cycle. Lenders are underwriting tighter, institutional LPs are running deeper due diligence, and the bar for a "clean" deal has risen. Navigating this environment demands a strategic approach to capital architecture that aligns risk with returns across every layer of the stack.

In 2026, institutional capital is available. CBRE projects total U.S. commercial real estate investment at approximately $562 billion for the year, up roughly 16% from 2025. Debt availability has improved. Family offices are active. Private credit platforms are sitting on record dry powder. The capital is there.

But access to that capital is more structure-sensitive than it has been in any prior cycle. Lenders are underwriting tighter. Institutional LPs are running deeper diligence. And the bar for what counts as a "clean" deal has moved. Developers who walk into outreach with a fragmented capital ask, a leveraged-up pro forma, or a waterfall that does not hold up under stress are getting passed over, not because their assets are weak, but because their structure is.

This is the gap most developers do not see until they are already in the room.

The purpose of this guide is to fix that. It is written for experienced principals, managing partners, and GPs who have closed deals before and are now scaling into $10M to $75M institutional raises. It covers how the capital stack actually works at this deal size in 2026, how to sequence the layers before outreach, where most structures break down, and how to protect GP economics without losing institutional confidence.

Key takeaways from this guide:

- Institutional capital does not reward maximum leverage. It rewards disciplined sequencing and clear risk allocation across every layer of the stack.

- The 2026 market has tightened senior loan proceeds, expanded private credit, and made LP diligence more rigorous. The old playbook of maximizing leverage and filling gaps with cheap capital no longer works.

- The developers who get funded structure the deal first, then go to market. Structure is now a fundability issue, not just a finance issue.

For a broader breakdown of how capital structure instruments work across development and growth contexts, see IRC Partners' foundational piece on what investors actually want from the capital stack.

What a $10M+ Real Estate Capital Stack Actually Looks Like in 2026

A capital stack is the full set of financing sources used to fund a real estate project, arranged from the least risky to the most risky. Each layer has a different cost, a different claim on cash flow and collateral, and a different set of expectations from the people providing it.

For deals in the $10M to $75M range, the stack typically includes some combination of the following layers:

Return ranges sourced from Agora Real Estate institutional stack frameworks and current market benchmarks.

How each layer works

Senior debt is the first mortgage or construction loan. It is the cheapest capital in the stack because it has the strongest collateral position and the first claim on repayment. In 2026, agency lenders like Fannie Mae and Freddie Mac are pricing 7-year multifamily debt in the 6.5–7% range. Bridge and construction lending runs higher, often 8.5–10% for value-add or development plays. Senior debt is the foundation of any institutional stack.

Mezzanine debt sits between senior debt and equity. It is a loan secured by a pledge of the equity interests in the property-owning entity rather than the property itself. It carries a higher rate than senior debt and requires an intercreditor agreement with the senior lender. Not all senior lenders allow it.

Preferred equity occupies a similar position to mezzanine in the stack, but is structured as an equity instrument rather than a debt instrument. It carries a fixed minimum return, often 12% or higher, and is paid before common equity receives any distributions. Banks often prefer preferred equity over mezzanine because it does not trigger the same regulatory treatment as a second lien.

LP equity is the institutional capital most developers are actually trying to raise. LPs take on the highest risk below the GP and expect returns in the 15–25%+ IRR range depending on deal type and hold period.

GP equity is the sponsor's own capital contribution, typically 2–10% of total project cost. Thin GP equity is one of the fastest ways to lose institutional confidence.

What the 2026 market has changed: According to MSCI's Real Assets in Focus report, real-estate debt funds have grown to approximately 15% of the first-mortgage market and senior debt outperformed equity through mid-2025. Institutional investors are no longer treating equity as the default path to superior returns. That shift changes how every layer of the stack needs to be sized and justified.

Why the Old Playbook Stopped Working: What Changed in the Market

Developers who last raised capital in 2019 or 2021 are operating with assumptions that no longer match the market. Three structural shifts have changed how institutional capital evaluates real estate deals, and each one directly affects how the stack needs to be built.

Shift 1: Banks pulled back and senior proceeds shrank

Regional banks have tightened dramatically. According to research published by PREA, 72% of banks reported tightening lending standards in the period following the rate cycle. Federal regulations around High Volatility Commercial Real Estate (HVCRE) have further constrained construction lending, particularly for asset classes outside of multifamily and industrial. The result is that senior loan proceeds as a percentage of total project cost have come down, often landing in the 50–60% loan-to-cost range on development deals rather than the 65–70% many developers still assume.

That gap does not disappear. It becomes the most expensive part of the stack to fill.

Shift 2: Private credit expanded, but it prices risk fast

Private credit platforms have moved aggressively into the space left by regional banks. The private credit market now exceeds $2 trillion in assets under management and is projected to approach $4 trillion by 2030, according to CreditSights' 2026 Private Credit Outlook. Private credit CLOs now account for roughly 20% of the direct lending market.

This expansion creates more capital options for developers. But private credit is not patient or forgiving. These platforms underwrite quickly, price risk into their terms aggressively, and have little tolerance for deals where the capital stack logic is unclear. A developer who approaches a private credit lender with a stack that relies on optimistic senior proceeds and vague gap financing will get a price that reflects that ambiguity, not a pass.

The real cost of a messy structure is not a rejection. It is an expensive term sheet.

Shift 3: Institutional LPs changed what they are asking for

Family offices and institutional LPs have shifted their evaluation criteria. They are no longer leading with "what is the projected IRR?" They are asking "what happens if things do not go to plan?"

Cushman & Wakefield's 2026 outlook notes that investors are prioritizing cash-flow growth and downside protection over cap-rate compression. MSCI data confirms that 82% of wealth managers plan to increase allocations to private credit, which means LP capital is competing against debt alternatives that offer structured returns with less execution risk.

For developers, this means the stack must tell a coherent downside story, not just an upside one. LPs want to see what the deal looks like at 10% over budget, 90% occupancy, and a 200 basis point rate shock. If the structure does not survive that stress test on paper, it will not survive diligence either.

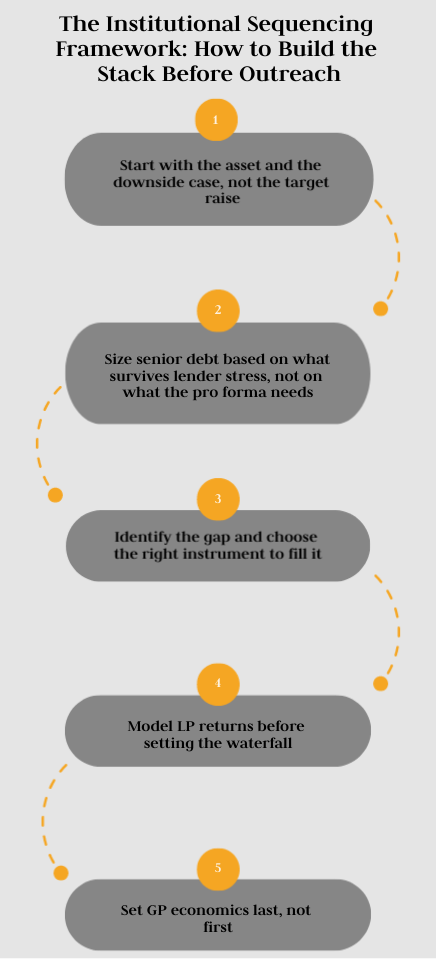

The Institutional Sequencing Framework: How to Build the Stack Before Outreach

Most developers approach capital formation in the wrong order. They decide how much they want to raise, build a pro forma that justifies it, and then go looking for capital sources to fill each slot. That is a reactive process. Institutional capital rewards a proactive one.

The sequencing framework below is how well-capitalized $10M–$75M projects are actually structured before they go to market. It is not a checklist of financing options. It is a decision sequence that forces each layer of the stack to earn its place based on what the deal can actually support.

Step 1: Start with the asset and the downside case, not the target raise

Before selecting any capital layer, model what the project looks like under stress. That means:

- Construction cost 10–15% over budget

- Lease-up taking 6–9 months longer than projected

- Stabilized occupancy at 88–92% instead of 95%

- A 200 basis point increase in the rate used for refinancing or exit cap rate

If the project cannot service its obligations and return capital to investors under those conditions, the structure is not ready for institutional outreach. Fixing the model before approaching capital sources is not a delay. It is the work that gets deals funded.

The institutions that will fund your project will run this exact stress test in diligence. Run it yourself first.

Step 2: Size senior debt based on what survives lender stress, not on what the pro forma needs

The most common structural mistake developers make is backing into the senior debt assumption. They decide the project needs 65% loan-to-cost to pencil, and then they go looking for a lender willing to hit that number.

The right approach is the reverse. Identify what a conservative senior lender will actually underwrite given the asset class, market, and sponsor track record. In most development deals today, that number is closer to 50–60% LTC. Lock that in as the anchor for the rest of the stack. Everything else gets sized around the gap between that number and total project cost.

This discipline matters because senior debt is the cheapest capital in the stack. Every dollar of senior debt that gets replaced by mezzanine or preferred equity costs the deal an additional 6–8 percentage points in blended cost of capital.

Step 3: Identify the gap and choose the right instrument to fill it

Once senior debt is sized, the gap between senior proceeds and total project cost is the real structuring problem. Developers have three main options:

- Increase sponsor equity to reduce the gap and improve the stack's credibility with LPs. This is the most LP-friendly option but requires more capital from the GP.

- Add a mezzanine or preferred equity layer to bridge the gap with structured subordinate capital. This is often necessary but adds cost and complexity. The choice between mezz and preferred equity depends on what the senior lender allows and how the intercreditor structure affects LP confidence.

- Reduce total project scope to bring cost in line with what the capital stack can realistically support. This is the option developers resist most, but it is often the right call.

Preferred equity has become the more common gap-filling instrument in bank-led structures. As noted by PREA, banks often prefer preferred equity over mezzanine because mezzanine financing can be treated as an additional loan under certain regulatory frameworks. Subordinate capital in this layer is currently pricing at 12–16% depending on attachment point and deal risk.

Step 4: Model LP returns before setting the waterfall

Once the debt and structured equity layers are set, model what LP investors will actually earn across the base, downside, and upside scenarios. If the LP return in the base case does not clear a 15% IRR threshold, one of two things is true: the deal does not work at this capital structure, or the stack needs to be rebuilt with lower-cost layers.

Do not set the waterfall first and then try to justify it. Build the waterfall from what the deal can support.

Step 5: Set GP economics last, not first

GP promote, catch-up mechanics, and sponsor fees should be the last variables in the model, not the first. The promote structure should reflect what the market will bear given the asset type, deal risk, and LP alternatives. Aggressive promotes in a market where LPs have strong alternatives will either get renegotiated in diligence or kill the deal entirely.

A reasonable institutional structure for a $15M–$50M development deal in 2026 typically looks like this:

- Preferred return to LPs: 7–8% annually on invested capital

- Catch-up to GP: until the sponsor has received approximately 20% of total distributions

- Split above the hurdle: 70–80% to LPs, 20–30% to GP depending on deal size and risk

This structure aligns incentives without signaling that the sponsor is extracting value before LPs are whole. The spokes in this series go deeper on GP/LP split mechanics and how to calculate the right promote for your specific deal.

When to Use Senior Debt, Mezzanine Debt, or Preferred Equity — and When Not To

Each capital layer has a job. The mistake most developers make is choosing layers based on what maximizes proceeds rather than what preserves execution certainty. Here is a practical decision framework for the three most commonly misused layers in $10M+ development deals.

Senior debt: use it as the anchor, size it conservatively

Senior debt should be the first layer sized and the last one compromised. It is the cheapest capital in the stack and the one that most directly signals deal quality to every other investor in the structure.

The key rule: Do not use the senior debt assumption to make the deal look fundable. Use it to anchor what the deal can actually support.

Mezzanine debt: use it when the intercreditor structure is clean

Mezzanine debt is a legitimate tool when the senior lender allows it, the intercreditor agreement is workable, and the sponsor can support a debt-like obligation that sits above the equity. It is not a universal gap filler.

When to use mezzanine debt

When to avoid it

Senior lender has approved mezzanine and intercreditor terms are agreed

Senior lender does not allow subordinate debt or requires clean first lien only

Sponsor has strong cash flow coverage and can support the debt service

Project cash flows are thin and adding a second fixed obligation creates execution risk

Deal has a clear exit path that retires the mezz before or at stabilization

Long-duration hold with uncertain refinancing at maturity

Mezzanine debt is currently pricing at 10–14% for well-structured deals with adequate equity cushions. If the blended cost of senior debt plus mezz approaches the expected yield on the asset, the deal needs to be restructured, not financed.

Preferred equity: use it when banks require it, not as a default

Preferred equity is increasingly the gap-filling instrument of choice in bank-led construction structures, specifically because banks often prefer it over mezzanine for regulatory reasons. But preferred equity is still expensive capital, typically pricing at 12% or higher in the current market, and it should not be treated as a convenient substitute for sponsor equity.

The part most coverage misses: The choice between mezzanine and preferred equity is not just about cost. It is about what the senior lender will approve, what the intercreditor structure looks like for LPs, and how each instrument affects the story you are telling to every other capital source in the stack. For a deeper breakdown of how these three layers compare in practice, the companion spoke in this series — Senior Debt vs. Mezzanine vs. Preferred Equity: Which Layer Do You Actually Need? — goes through the decision framework in detail.

How to Protect GP Economics Without Scaring Off Institutional Capital

GP economics are where most developers negotiate against themselves. They either give away too much trying to look LP-friendly, or they push for a promote structure that signals misalignment and slows diligence. The goal is not to minimize what the sponsor earns. It is to design economics that institutional capital can underwrite without hesitation.

Here are five rules that experienced capital advisors apply when structuring GP economics for $10M+ institutional raises.

- Rule 1: Tie your promote to actual performance, not to closing. Acquisition fees, asset management fees, and development fees are legitimate, but they should be sized relative to the project and disclosed clearly. Sponsors who load the deal with front-end fees before LPs have earned a return signal that the promote is more important to them than the outcome. Institutional LPs notice this immediately.

- Rule 2: Use a hard preferred return, not a soft one. A hard preferred return means LPs receive their pref before any distributions go to the GP, regardless of timing. A soft pref can be waived or modified. Institutional capital almost always requires a hard pref structure. Offering a soft pref to save a few basis points of economic flexibility will cost you the LP relationship.

- Rule 3: Keep the catch-up mechanics transparent and proportionate. The catch-up is the mechanism that brings the GP up to its promote percentage after LPs have received their preferred return. Vague or aggressive catch-up language is one of the most common reasons institutional LPs push back in diligence. The catch-up should be clearly defined, mathematically consistent with the split, and proportionate to the deal's risk profile.

- Rule 4: Put meaningful GP equity in the deal. Thin sponsor equity, anything below 5% of total project cost, is a signal that the GP is not sufficiently exposed to downside risk. Institutional LPs want to see that the sponsor has real capital at risk alongside them. GP equity is not just a regulatory requirement. It is a trust signal.

- Rule 5: Model your promote before you present it. Run the waterfall through your base case, downside case, and upside case before showing it to any LP. If the GP earns a strong promote in the downside scenario while LPs are barely whole, the structure will not survive diligence. The promote should reward outperformance, not compensate for underperformance.

The alignment test: Before finalizing GP economics, ask this question: If the deal performs at exactly the base case, does every party in the stack, senior lender, preferred equity, LP, and GP, earn a return that is proportionate to the risk they took? If the answer is no, the structure needs to be adjusted before outreach, not during it.

For a detailed walkthrough of how to calculate the right GP/LP split for different deal types and capital structures, see the companion spoke in this series on how to calculate the right GP/LP split for your deal.

Case Example: How Institutional-Grade Stack Design Changes the Raise

The difference between a deal that closes and one that stalls in diligence is rarely the asset. It is almost always the architecture of the capital stack and whether the advisor coordinating it understood how to make every layer speak the same language to every capital source.

The following is an anonymized example drawn from IRC Partners' advisory work.

IRC Partners — Anonymized EngagementAsset type: Mixed-use development Geography: Florida Total capitalization: $900 million Advisory role: Capital stack design, institutional capital coordination, and LP alignment

- The project involved a complex, multi-phase mixed-use development requiring coordination across multiple debt layers, institutional LP equity, and structured subordinate capital.

- When IRC Partners engaged, the existing capital structure had been assembled reactively, with each layer sourced independently and without a coherent story connecting senior debt sizing, gap financing, and LP economics.

- The first step was not outreach. It was a full structural audit: stress-testing the existing assumptions, identifying the layers that were mis-sized or mispriced, and rebuilding the stack sequencing from the senior debt anchor outward.

- Once the structure was rebuilt with consistent assumptions across every layer and a waterfall that institutional LPs could underwrite, the capital coordination process moved significantly faster than the developer's prior attempts.

- The completed structure gave senior lenders, subordinate capital providers, and institutional LP equity investors a coherent risk-return story at every position in the stack.

What this engagement illustrates is not a unique outcome. It is a repeatable process.

IRC Partners structures institutional-grade capital stacks first, then coordinates introductions to capital sources. The firm does not operate as a single-transaction placement agent. It embeds as a capital advisory partner across multiple raises, with access to a network of over 307,000 institutional allocators and a syndicate of 77 global investment bank partners.

For developers who have attempted institutional raises through broker-led processes and found that the outreach produced debt-only solutions or no meaningful LP introductions, the issue is almost always structural. The deal was not wrong. The stack was not ready.

For a deeper look at how to evaluate and select the right capital advisory firm for a $10M+ raise, see the companion spoke in this series on the best firms for structuring capital stacks in real estate.

Common Mistakes That Make Institutional Capital Walk Away

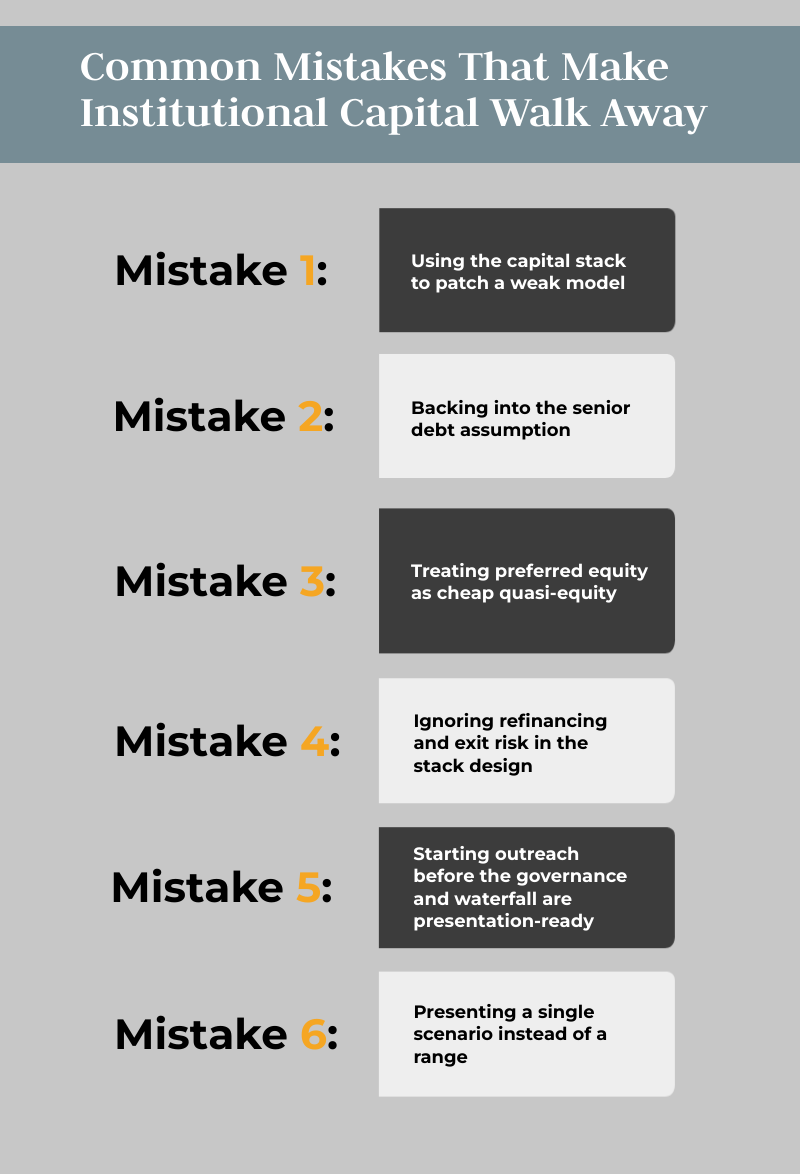

Most institutional capital does not walk away from bad deals. It walks away from deals that look like they were structured by someone who did not understand what institutional capital needs to see. These are the six most common structural mistakes that kill $10M+ raises before they close.

- Mistake 1: Using the capital stack to patch a weak model. If the project only works because the stack is maximally leveraged and every assumption is at the top of the range, the stack is not solving a financing problem. It is hiding a deal problem. Institutional lenders and LPs will find it in diligence. The fix is to address the model before structuring the raise, not after.

- Mistake 2: Backing into the senior debt assumption. As discussed in the sequencing framework above, starting with a target LTC and working backward to find a lender willing to hit it is the single most common structural error in $10M+ raises. It produces a stack where every other layer is sized around an optimistic anchor that may not survive underwriting.

- Mistake 3: Treating preferred equity as cheap quasi-equity. Preferred equity at 12–16% is not cheap. It is expensive subordinate capital that sits above LP equity in the payment waterfall and can compound against the deal if the exit timeline slips. Developers who use preferred equity to reduce their own equity contribution without modeling its impact on LP returns will lose LP confidence in diligence.

- Mistake 4: Ignoring refinancing and exit risk in the stack design. A capital stack that works at construction but cannot be refinanced at stabilization is not a complete structure. Every layer of the stack should be evaluated against what the deal looks like at exit, not just at close. Preferred equity with compounding accruals, mezzanine with hard maturity dates, and senior debt priced at bridge rates all create exit pressure that needs to be modeled before outreach.

- Mistake 5: Starting outreach before the governance and waterfall are presentation-ready. Institutional LPs will ask for the full waterfall, the operating agreement structure, and the distribution mechanics in the first or second meeting. Developers who say "we are still working on the structure" signal that the deal is not ready. Structure first. Outreach second.

- Mistake 6: Presenting a single scenario instead of a range. Institutional capital is managed by people whose job is to model downside scenarios. A developer who presents only the base case or upside case is not building trust. They are signaling that they have not done the stress testing. Present the base case, a conservative case, and the downside case. Show what happens to every layer of the stack in each scenario.

The common thread across all six mistakes: They are all symptoms of approaching capital markets reactively rather than structurally. The developers who avoid them are the ones who treat stack design as a pre-outreach discipline, not a mid-raise problem to solve.

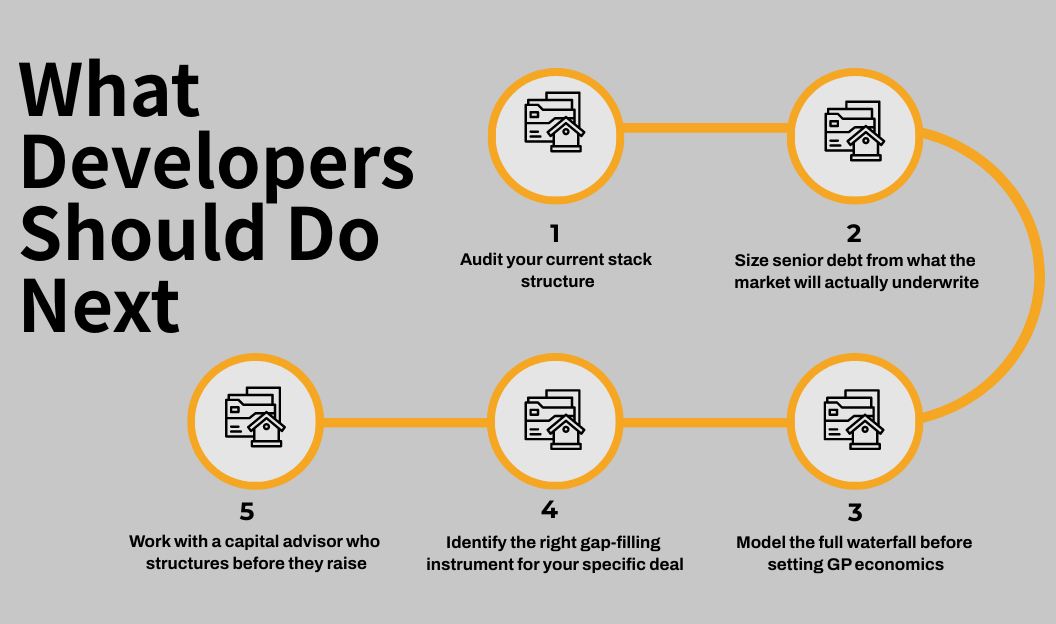

What Developers Should Do Next

Capital stack design is not a one-time task. It is the foundation of every institutional raise, and it needs to be rebuilt or stress-tested for each new project. Here is a practical sequence for developers who are preparing for a $10M+ raise in 2026.

- Audit your current stack structure. Before any outreach, map every layer of your proposed capital stack, identify the assumptions behind each one, and stress-test the full structure against a conservative scenario. If any layer only works under best-case assumptions, it is a structural weakness, not a financing solution.

- Size senior debt from what the market will actually underwrite. Get real-market feedback on senior debt sizing from two or three lenders before finalizing the stack. Use the lowest realistic LTC as your anchor, not the highest one you can find.

- Model the full waterfall before setting GP economics. Build the distribution model from LP returns upward. The promote structure should be the output of what the deal can support, not the input that drives the rest of the structure.

- Identify the right gap-filling instrument for your specific deal. Whether that is preferred equity, mezzanine debt, or additional sponsor equity depends on your senior lender's requirements, your LP's expectations, and the risk profile of the asset. The comparison spoke in this series — which capital stack layers are best for minimizing risk — walks through this decision in detail.

- Work with a capital advisor who structures before they raise. The most common failure mode in broker-led processes is that the broker leads with outreach and discovers structural problems mid-process. An institutional-grade capital advisor structures the deal first, aligns every layer, and then coordinates introductions to the right capital sources at the right time.

IRC Partners works exclusively with seasoned real estate developers raising $10M or more in institutional capital. The firm's model is to structure the capital stack before going to market, then coordinate warm introductions to family offices, private equity funds, and institutional allocators through a network of over 307,000 institutional allocators and 77 global investment bank partners.

If you are preparing for a $10M+ institutional raise and want to evaluate whether your current capital stack is structured to survive diligence, speak with the IRC Partners team about a capital stack review.

For a deeper breakdown of the topics covered in this guide, see the full IRC Partners Capital Stack Series on the IRC Partners YouTube channel, where each spoke in this series is covered as a standalone video.

Frequently Asked Questions

What is a capital stack in real estate development?

A capital stack is the complete set of financing sources used to fund a project, organized from least risky (senior debt) to most risky (equity). It typically includes senior debt, mezzanine debt or preferred equity, limited partner equity, and general partner equity. Each layer has distinct costs, claims on cash flow, and return expectations. For deals over 10M dollars, the stack must be sequenced to meet rigorous institutional diligence requirements.

How much senior debt can I get for a 10M dollar plus deal in 2026?

In 2026, most lenders are underwriting senior debt at 50 to 60 percent loan-to-cost for ground-up development. Agency lenders are pricing multifamily debt in the 6.5 to 7 percent range, while bridge or construction lending often runs between 8.5 to 10 percent. Developers should not build models around 70 percent loan-to-cost assumptions, as those levels are no longer standard for institutional-grade projects.

What is the difference between mezzanine debt and preferred equity?

Both layers sit between senior debt and common equity, but their legal structures differ. Mezzanine debt is a loan secured by a pledge of equity interests and requires an intercreditor agreement. Preferred equity is an equity instrument with a fixed minimum return. Banks often prefer the preferred equity format for regulatory reasons, making it the most common gap-filling instrument in current construction structures.

What return do institutional partners expect in a 10M dollar plus deal?

Partners typically target a 15 to 25 percent plus internal rate of return for development deals. Most institutional structures also include a 7 to 8 percent preferred return paid annually on invested capital before the developer participates in profits. Sponsors must demonstrate that these returns are achievable in the base case and that the project remains viable in a downside scenario.

Why do institutional raises fail even when the deal is good?

Failure is usually structural. Common issues include mis-sequenced capital stacks, overly aggressive leverage assumptions, or misaligned developer economics. In 2026, institutional investors prioritize risk mitigation; if a developer cannot clearly articulate what happens if the project underperforms, the deal will likely be rejected during the diligence phase.

What is a GP promote and how should it be structured?

The promote is the sponsor share of profits above the preferred return. It is typically structured as a tiered waterfall: investors get their 7 to 8 percent return, followed by a developer catch-up, and then a residual split, such as 80/20. The promote should be sized based on what the project can realistically support while maintaining investor interest and meeting internal rate of return hurdles.

How do I know if my capital stack is ready for institutional outreach?

It is ready when it passes three specific tests. First, it must survive a stress scenario, such as a 15 percent cost overrun. Second, every layer must reflect realistic market terms for 2026. Third, developer economics must be transparent and documented in a clear waterfall. If the stack breaks under these pressures, it is not yet ready for institutional review.

Continue reading in this series:

- Senior Debt vs. Mezzanine vs. Preferred Equity: Which Layer Do You Actually Need?

- Which Capital Stack Layers Are Best for Minimizing Risk?

- How to Calculate the Right GP/LP Split for Your Deal

- Programmatic JVs vs. Closed-End Funds: Which Capital Structure Fits Your Stage?

- Best Firms for Structuring Capital Stacks in Real Estate

The wrong structure doesn't just cost you this round. It costs you the next three. IRC Partners advises founders raising $5M to $250M of institutional capital. If you're about to go to market and want the structure reviewed before investors see it, book a call here

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.