.svg)

.png)

Senior Debt vs. Mezzanine vs. Preferred Equity: Which Layer Do You Actually Need?

Senior Debt vs. Mezzanine vs. Preferred Equity: Which Layer Do You Actually Need?

Senior debt, mezzanine debt, and preferred equity each fill a different position in the capital stack - and each comes with different lender permissions, cost structures, and execution risks.

Senior debt covers the largest portion of the stack, typically 55% to 70% of total capitalization, and carries the lowest cost but the strictest underwriting. Mezzanine debt sits behind senior debt in second lien position, fills a portion of the gap, and is permitted by some senior lenders but not all. Preferred equity sits in the equity layer, carries no lien on the property, and is the structure most senior lenders will accept when mezzanine is not permitted.

Choosing the wrong layer does not just affect your cost of capital. It can make your deal unbankable.

Most developers approach the capital stack gap the same way. They model total proceeds, rank the options by headline cost, and pick the one that looks most efficient on paper. Then they get to lender conversations and find out the structure they chose is not permitted, not bankable, or not something their institutional LPs will accept. That is an expensive lesson on a $10M+ deal.

This article is Spoke 1 in IRC’s Hub 4 series on structuring the capital stack for $10M+ real estate deals. The hub covers the full sequencing framework. Utilizing dedicated capital advisory for real estate sponsors helps clarify which layer - senior debt, mezzanine debt, or preferred equity - is actually the right fit for your specific gap.

By the end of this article, you will be able to:

- Identify which layer your senior lender will and will not permit

- Compare the real cost of each instrument beyond headline pricing

- Choose the structure that protects execution certainty, not just maximum proceeds

Where Each Layer Actually Sits in the Capital Stack

Before comparing instruments, you need to know where each one lives legally, not just financially. Position in the stack determines payment priority, default remedies, and what your senior lender will tolerate sitting behind them.

The legal distinction between mezzanine and preferred equity is not cosmetic. As Anchin's analysis of CRE financing structures makes clear, mezzanine debt is secured by a pledge of 100% of the equity interests in the borrowing entity, giving the lender UCC foreclosure rights. Preferred equity holds no lien on the property and no UCC filing. Instead, it relies on provisions in the LLC operating agreement.

That difference changes everything: lender approval requirements, intercreditor obligations, cure rights, and how fast a lender can act if the deal goes sideways.

The label matters less than the legal position.

The Practical Comparison Framework: Cost, Control, Lender Tolerance, and LP Impact

Headline pricing is the first thing sponsors look at and often the least useful variable for making this decision. Here is how the three layers compare across the dimensions that actually determine whether a deal closes cleanly.

Hidden Costs Sponsors Miss

Headline rate comparisons miss the real cost of each layer. Before choosing, model these:

- Intercreditor legal fees: Mezzanine requires a negotiated intercreditor agreement with the senior lender. On a $10M+ deal, this can add significant legal cost and weeks to timeline.

- Accrual and compounding: Preferred equity with deferred current pay can look cheaper up front but compounds quietly. Model the exit distribution, not just the stated rate.

- Governance and consent rights: Preferred equity providers often negotiate consent rights over major decisions, capital calls, or disposition. This affects sponsor control and LP waterfall.

- Co-terminus risk: Mezzanine loans typically mature when the senior loan matures. If the senior loan does not extend, the mezz does not either. That is a refinancing constraint most sponsors underestimate.

- LP perception: Institutional LPs reviewing a deal memo will scrutinize the subordinate layer. A preferred equity provider with aggressive control rights can raise red flags in LP diligence even if the economics look fine.

The bottom line: mezzanine is often cheaper on paper but carries more structural friction. Preferred equity trades some economics for lender compatibility and current-pay flexibility. Neither is automatically better. The right answer depends on what your senior lender will allow, what your cash flow can carry, and what your LPs will accept.

Senior Lender Reality: Why Your Lender Often Makes This Choice for You

Most sponsors think they are choosing between mezzanine and preferred equity. In many cases, their senior lender has already made the choice for them.

Agency lenders - Fannie Mae, Freddie Mac, and similar programs - typically prohibit mezzanine debt outright. Bank construction lenders are more varied, but many restrict or require consent for any subordinate debt layer. According to PREA's analysis of the multifamily capital stack, most banks prefer preferred equity over mezzanine because mezzanine can be treated as an additional debt layer under HVCRE regulations, which complicates their regulatory capital treatment.

The real risk: sponsors who assume mezzanine is available without confirming it in writing often discover the conflict after term sheets are signed. Rebuilding the structure at that stage costs time, legal fees, and sometimes the deal.

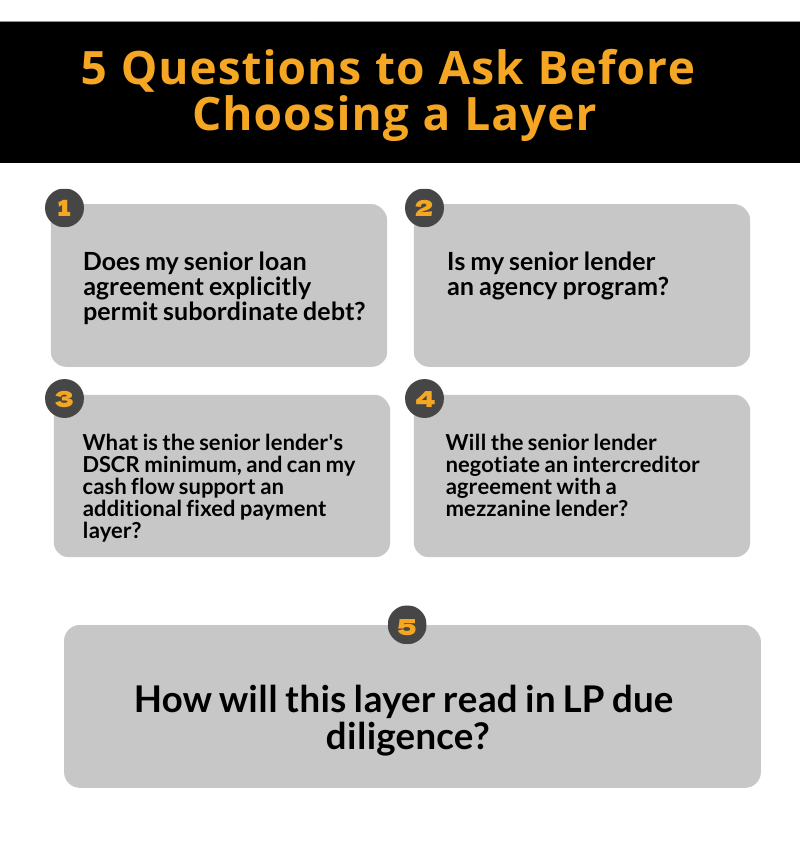

5 Questions to Ask Before Choosing a Layer

Ask these before approaching any subordinate capital provider:

- Does my senior loan agreement explicitly permit subordinate debt? Get the answer in writing from your lender, not just verbal confirmation.

- Is my senior lender an agency program? If yes, mezzanine is likely off the table. Preferred equity is the practical starting point.

- What is the senior lender's DSCR minimum, and can my cash flow support an additional fixed payment layer? Mezzanine adds a mandatory cash obligation. Model the combined debt service before committing.

- Will the senior lender negotiate an intercreditor agreement with a mezzanine lender? Some lenders allow mezz in principle but impose intercreditor terms so restrictive that mezz providers will not accept them.

- How will this layer read in LP due diligence? Institutional LPs will ask about subordinate capital. Know how the structure looks before you have to explain it in a capital call memo.

Understanding the answers to these questions is part of what IRC addresses before any capital outreach begins.

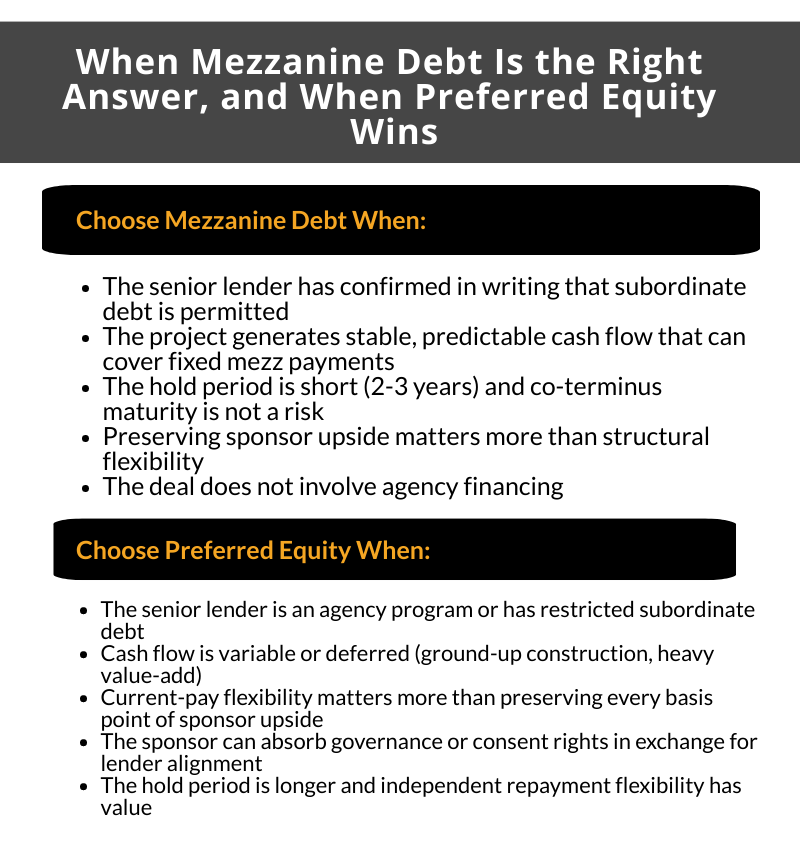

When Mezzanine Debt Is the Right Answer, and When Preferred Equity Wins

Once you know what your senior lender permits, the selection comes down to four variables: cash flow predictability, hold period, sponsor control priorities, and LP composition. Here is how to apply them.

Choose Mezzanine Debt When:

- The senior lender has confirmed in writing that subordinate debt is permitted

- The project generates stable, predictable cash flow that can cover fixed mezz payments

- The hold period is short (2-3 years) and co-terminus maturity is not a risk

- Preserving sponsor upside matters more than structural flexibility

- The deal does not involve agency financing

Choose Preferred Equity When:

- The senior lender is an agency program or has restricted subordinate debt

- Cash flow is variable or deferred (ground-up construction, heavy value-add)

- Current-pay flexibility matters more than preserving every basis point of sponsor upside

- The sponsor can absorb governance or consent rights in exchange for lender alignment

- The hold period is longer and independent repayment flexibility has value

If This, Then That

Private real estate debt funds raised $51 billion in 2025 and captured 31% of private real estate commitments according to Fidelity Institutional research, reflecting how much institutional capital has moved into this space. That means providers exist for both instruments. The constraint is almost never availability. It is fit.

For a broader look at how layer selection connects to downside protection across the full stack, see IRC's guide on which capital stack layers are best for minimizing risk.

Proof Point: One IRC Engagement Where Layer Selection Mattered

Engagement: Capital advisor, multifamily development, Texas, $150M total capitalization

The Challenge

The developer had identified a gap in the capital stack and was approaching mezzanine providers based on headline pricing. The senior construction lender had not been formally consulted on subordinate debt. The deal had institutional LP involvement and a ground-up business plan with no current cash flow during the construction phase.

The Decision

IRC's role was to pressure-test the proposed structure before outreach began. The senior lender's loan documents restricted subordinate debt without prior written consent, and the lender indicated that consent would not be granted for a mezzanine instrument given HVCRE exposure concerns. The structure was repositioned around preferred equity with an accrual feature aligned to the construction timeline, eliminating the intercreditor conflict and reducing documentation friction with the senior lender.

The Implication

The deal did not need a different capital source. It needed the right instrument for the lender relationship and business plan already in place. Choosing the wrong layer first would have required rebuilding the structure after term sheets were in motion. Layer selection happened before outreach, not after.

IRC structures the deal before going to market. That sequencing is the difference between a clean raise and a delayed one.

What Developers Should Do Next Before Lender Outreach

Capital is available in 2026. The issue is whether your structure can actually close under the constraints your senior lender, LPs, and timeline will impose. Before approaching any subordinate capital provider, work through this checklist.

Pre-outreach structure checklist:

- Confirm in writing whether your senior lender permits subordinate debt

- Identify whether your senior loan is agency or bank - this narrows the menu immediately

- Model combined DSCR under both mezzanine (fixed current pay) and preferred equity (accrual) scenarios

- Map the governance and consent rights a preferred equity provider is likely to require and assess LP tolerance

- Review co-terminus maturity risk if mezzanine is on the table

- Confirm how the subordinate layer will be presented in LP deal memos and subscription documents

For a deeper look at how firms approach this kind of structuring work, see IRC's overview of best firms for structuring capital stacks in real estate.

Ready to choose the right layer before lender outreach?

IRC works with seasoned developers raising $10M+ to pressure-test capital stack structure before going to market. Book a strategy call with IRC to get the layer selection right before term sheets are in play.

Frequently Asked Questions

What is the difference between mezzanine debt and preferred equity?

Mezzanine debt is a loan secured by a pledge of ownership interests, giving the lender foreclosure rights under the Uniform Commercial Code. Preferred equity is an equity investment governed by the operating agreement. While both sit between senior debt and common equity, banks often prefer the preferred equity structure for regulatory reasons, making it the more common gap-filling instrument in 2026.

Can I use mezzanine debt with an agency loan?

Generally, no. Fannie Mae, Freddie Mac, and most agency programs strictly prohibit subordinate debt. This is a hard restriction rather than a negotiation point. Since agency lenders require specific equity percentages and mezzanine debt does not count as equity, preferred equity is usually the only viable subordinate capital option for agency-backed senior loans.

Which is cheaper: mezzanine debt or preferred equity?

Mezzanine debt typically costs 10 to 15 percent all-in. Preferred equity rates often range from 8 to 15 percent, but the total cost can be higher once participation and compounding are modeled. Developers should compare exit economics rather than headline pricing to understand the true impact on the project bottom line.

What is an intercreditor agreement and why does it matter?

An intercreditor agreement is a contract between the senior and mezzanine lenders defining priority, cure rights, and enforcement controls. Negotiating this agreement can add weeks to a closing. If the terms are too restrictive, mezzanine providers may decline the deal entirely, making it critical to confirm these terms early in the process.

How does preferred equity affect my investor waterfall?

Preferred equity sits ahead of common equity in the payment priority. If the provider has participation rights, it reduces investor returns before the developer profit split is even calculated. Institutional partners will scrutinize these terms heavily, so it is vital to disclose and model these exit economics clearly in your deal memos.

What loan-to-cost ratios should I expect in 2026?

In 2026, construction lenders are underwriting at 50 to 65 percent loan-to-cost, a notable decrease from pre-2022 levels. Agency lenders remain active in multifamily with 7-year debt priced at 6.5 to 7 percent, while bridge lending for value-add projects typically runs between 8.5 to 10 percent.

When should I use senior debt alone?

Use senior debt alone if the proceeds are sufficient and adding subordinate capital would create unnecessary cash flow stress. The cleanest structure is usually best; subordinate layers should only be used to solve a genuine funding gap, not just to maximize paper proceeds at the expense of execution certainty.

Most founders don't lose the raise because of the pitch. They lose it because the structure was wrong before the first investor call. IRC Partners advises founders raising $5M to $250M of institutional capital. 7 strategic partners per quarter. Start here to schedule a call with our team.

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 7

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.