.svg)

.png "Investor Ready Capital decorative background element")

Top Firms for Real Estate Capital Raising Without Losing Equity

Top Firms for Real Estate Capital Raising Without Losing Equity

Most developers think equity dilution is what happens when they bring in an LP. That is only part of the story.

The equity you lose in a real estate raise comes from four places: LP equity stakes, advisory fees, unfavorable waterfall terms, and promote erosion over a multi-year hold. Most developers only watch the first one. The other three are where the real damage happens.

Understanding how the institutional capital stack works before you go to market is the starting point. But the advisory firm you choose determines how much of your equity survives the raise intact. Different advisory models have fundamentally different impacts on developer economics, and most developers do not compare them carefully enough before signing an engagement.

This article breaks down how each advisory model affects your equity, what the top firms for equity-preserving capital raises actually do differently, and how to evaluate any firm before you give them access to your deal.

Key Takeaway: The equity you keep is determined before the first LP meeting, not after. The advisory model, the waterfall design, and the preferred return structure are all set before you pitch. Getting these wrong is expensive and largely irreversible.

The 4 Ways Developers Lose Equity Without Realizing It

Equity loss in a real estate raise is not always visible in the LP agreement. It shows up in four places, and most developers only protect against one of them.

1. LP Equity Stakes (The Obvious One)

This is the equity you trade for capital. You bring in an LP who takes a percentage of the deal's profits above the preferred return. This is the expected and necessary cost of institutional capital.

The question is not whether you give up LP equity. You will. The question is whether the waterfall terms are structured to protect your promote at the high end of performance. A flat 20% promote with a single hurdle leaves money on the table if your deal outperforms. A tiered promote structure captures significantly more upside when performance is strong.

2. Advisory Fees (The One Most Developers Ignore)

A placement agent earning 1-3% cash fee on a $20M raise collects $200,000-$600,000 at close. That fee is paid out of the deal's capital, reducing the equity available for the project. And unlike equity-aligned advisory fees, a cash fee provides no ongoing benefit to the developer after close.

The fee structure also reveals the incentive alignment. A cash fee at close is earned the moment capital closes, regardless of whether the deal structure protects your economics. An advisory equity stake of 3-5% means the advisor only earns when you earn, over the full life of the deal.

3. Waterfall Terms (The Most Expensive One)

This is where the largest equity losses happen and where the least attention is paid. A compounding preferred return on a $20M raise can add hundreds of thousands of dollars to LP distributions before your promote kicks in. A European waterfall structure delays your promote payments until fund wind-down. A clawback provision can require you to return promote you already earned.

As James Moore & Co's waterfall analysis demonstrates, a GP contributing 10% of equity in a well-structured deal can achieve a 46.2% IRR while LPs earn 15.4%. The same deal with poorly structured waterfall terms can produce dramatically different outcomes for the GP, even with identical project-level returns.

4. Promote Erosion Over a Multi-Year Hold (The Slow One)

This one is the hardest to see at signing. If your deal takes longer than projected to exit, preferred returns accrue. If cash flows are uneven, cumulative preferred returns compound. If the market softens and you need to extend the hold period, LP economics improve relative to yours.

The developers who protect against promote erosion model multiple hold scenarios before they sign the LP agreement. They know what they earn if the deal exits in year three versus year five. They negotiate terms that protect their economics in extended hold scenarios, not just the base case.

The equity preservation hierarchy:

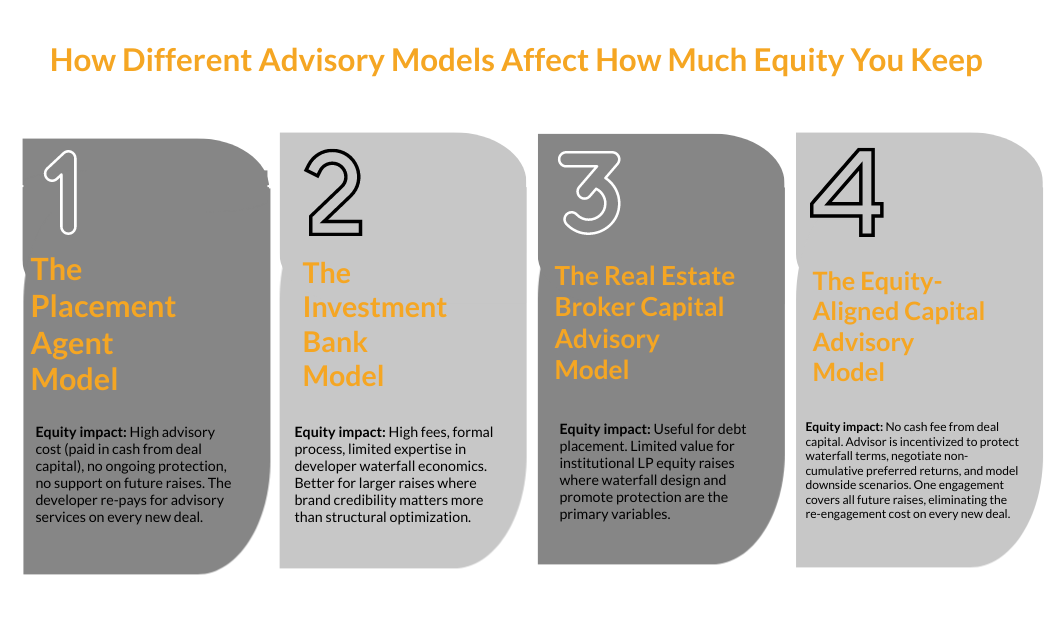

How Different Advisory Models Affect How Much Equity You Keep

The advisory model is not just a fee question. It determines what happens to your deal structure, your LP relationships, and your promote across every raise you do.

{{main-cta}}

The Placement Agent Model

A placement agent earns a cash fee (typically 1-3%) when capital closes. Their incentive is to close fast and move on. They have no reason to push back on unfavorable waterfall terms, negotiate non-cumulative preferred returns, or model your downside scenarios.

Equity impact: High advisory cost (paid in cash from deal capital), no ongoing protection, no support on future raises. The developer re-pays for advisory services on every new deal.

The Investment Bank Model

Middle-market investment banks charge higher fees and run more formal processes. They are better for developers raising $50M+ who need a recognized firm name and a structured marketing process. But their advisors are generalists, not real estate capital specialists.

Equity impact: High fees, formal process, limited expertise in developer waterfall economics. Better for larger raises where brand credibility matters more than structural optimization.

The Real Estate Broker Capital Advisory Model

Some commercial real estate brokerages have added capital advisory arms. They focus primarily on debt placement and may offer equity introductions as a secondary service. Their core expertise is brokerage, not institutional equity capital structuring.

Equity impact: Useful for debt placement. Limited value for institutional LP equity raises where waterfall design and promote protection are the primary variables.

The Equity-Aligned Capital Advisory Model

This is the model that produces the best long-term equity outcomes for developers who plan multiple raises. An equity-aligned advisor takes 3-5% advisory equity, structures the deal before going to market, and only earns when the developer earns.

Equity impact: No cash fee from deal capital. Advisor is incentivized to protect waterfall terms, negotiate non-cumulative preferred returns, and model downside scenarios. One engagement covers all future raises, eliminating the re-engagement cost on every new deal.

Advisory Model Comparison

The equity-aligned model costs more in advisory equity percentage. But it eliminates cash fees from deal capital, provides ongoing support across all future raises, and is the only model where the advisor has a direct financial incentive to protect your promote.

Understanding how anti-dilution protections work in the context of real estate waterfall design is the foundation for evaluating any advisory firm's actual value to your economics.

The 5 Equity Preservation Strategies That Institutional Developers Use

Developers who consistently close institutional rounds without giving away their upside use the same five strategies. None of them are complicated. All of them require doing the work before you go to market.

Strategy 1: Structure the waterfall before the first LP meeting. Do not negotiate waterfall terms under time pressure. Model the waterfall across three scenarios (base case, downside, extended hold) before you pitch. Know your numbers. Walk into every LP meeting knowing exactly what you earn at 10%, 15%, and 20% IRR.

Strategy 2: Push for non-cumulative preferred returns. This is negotiable in most deal-by-deal structures, especially with family offices who are evaluating each project individually. Non-cumulative preferred returns eliminate the compounding effect that can quietly add hundreds of thousands of dollars to LP distributions before your promote kicks in.

Strategy 3: Use tiered promote structures to capture high-performance upside. A flat 20% promote is the default. It is not the optimal structure. A tiered promote that reaches 30-40% above 15-20% IRR captures significantly more upside on outperforming deals. This is now standard in institutional structures and does not deter sophisticated LPs.

Strategy 4: Choose an equity-aligned advisor, not a transactional one. The advisor's compensation model determines their incentives. An advisor who earns a cash fee at close has no reason to protect your promote. An advisor who earns 3-5% advisory equity only wins when you win. That alignment changes the quality of every structural decision made before the LP agreement is signed.

Strategy 5: Build LP relationships before you need capital. Developers who are not raising at this moment are building the relationships that will make their next raise faster and better-structured. Warm introductions to institutional allocators take time to develop. According to Cushman & Wakefield's 2025 CRE fundraising analysis, CRE fundraising is on pace for $129B in 2025, up 38% from 2024, but concentrated with incumbents. The developers accessing that capital are the ones with established LP relationships, not the ones cold-pitching family offices.

The access problem is also an equity problem. When you are pitching from a position of desperation, you accept worse terms. When you have multiple institutional LPs interested in the deal, you negotiate from strength. The right advisory relationship, with warm introductions to the right 13% of family offices that actually write $10M+ checks, is itself an equity preservation strategy.

How IRC Partners Preserves Developer Equity Across Every Raise

IRC Partners was built specifically for the developer who is tired of watching equity walk out the door through advisory fees, unfavorable waterfall terms, and transactional advisors who disappear after close.

The IRC model works as follows:

No Cash Fees From Deal Capital

IRC takes 3-5% advisory equity in each engagement. There is no cash fee at close. The equity IRC earns is tied to the deal's performance, which means IRC only earns when the developer earns. This eliminates the $200,000-$600,000 advisory fee that a placement agent would pull from deal capital on a $20M raise.

Structure Before Pitch

IRC architects the capital stack and waterfall before any LP meetings. This includes:

- Modeling the waterfall across base case, downside, and extended hold scenarios

- Designing tiered promote structures that capture high-performance upside

- Negotiating for non-cumulative preferred returns where the LP relationship allows

- Reviewing every LP agreement provision before the developer signs

Access to the Right Allocators

IRC coordinates warm introductions to institutional allocators through a network of 307,000+ investors and 77 global investment bank syndicate partners. The firm focuses specifically on the 13% of family offices that write $10M+ checks, not the broader universe of smaller allocators who cannot move the needle on a $10M-$100M raise.

Family offices managing $17B+ request deal referrals directly from IRC. That means developers in an IRC engagement are being introduced to allocators who are already interested in the asset class, not cold-pitching a list of contacts.

One Engagement, All Future Raises

A single IRC engagement covers all future capital events through exit. Developers do not re-engage and re-pay for advisory services on every new deal. The ongoing relationship means IRC is embedded in the developer's capital formation strategy, managing LP relationships and positioning future deals with existing investors.

"The developers who build true institutional platforms are not the ones with the best deals. They are the ones who built the right advisory relationship early and protected their economics across every raise. That is the IRC model."

For developers who want to understand what a comprehensive capital raising service actually looks like for a $10M+ raise, the distinction between comprehensive and transactional advisory is most visible in what happens to developer equity over multiple raises.

IRC Partners accepts a maximum of 10 new strategic partners per quarter, by application only. This selectivity ensures every developer in an IRC engagement receives the focused attention that a $10M+ institutional raise requires.

Frequently Asked Questions

What is the biggest source of equity loss in a capital raise?

While developers focus on the investor stake, the primary hidden losses stem from unfavorable waterfall terms and upfront cash fees. Compounding preferred returns can add massive distribution requirements that must be met before the developer sees any profit. Furthermore, upfront fees of 1 to 3 percent immediately drain working capital that could have been used for the project itself.

How does the advisor compensation model affect my equity?

Placement agents earning cash fees have a transactional incentive to close a deal quickly, which often leads to overlooking poor waterfall terms. Conversely, an equity-aligned advisor taking 3 to 5 percent advisory equity only profits when you do. This alignment ensures they protect your profit split and optimize the deal structure for long-term equity retention.

Can I raise institutional capital without a fund structure?

Yes. In 2026, deal-by-deal structures are the preferred vehicle for many institutional family offices. By using an American waterfall and professional documentation, developers can access institutional-grade capital for specific projects. This avoids the regulatory overhead and complexity associated with managing a formal blind-pool fund.

What is the difference between a placement agent and an equity-aligned advisor?

A placement agent provides introductions for a one-time cash fee and typically exits the relationship after the deal closes. An equity-aligned advisor acts as a long-term partner who structures the capital stack and supports subsequent raises. This model lowers long-term costs for developers with a multi-project pipeline.

What GP co-investment percentage do institutional LPs require?

The current institutional standard for developer co-investment is 1 to 10 percent of the total project equity. This skin in the game is a non-negotiable requirement for most high-level allocators. It ensures the developer has a personal financial stake in the success of the project alongside the investors.

How do tiered promote structures protect developer equity?

A tiered structure increases the developer share of profits as the project hits higher internal rate of return hurdles. For example, a developer might earn a 20 percent split at an 8 percent hurdle, which increases to 30 percent after hitting a 15 percent hurdle. This rewards exceptional performance and allows the developer to capture more upside on successful deals.

How do I evaluate whether an advisory firm will protect my equity?

Evaluate them based on three criteria: compensation model, modeling capabilities, and engagement scope. You want a firm aligned with equity rather than cash fees, one that stress-tests the waterfall before going to market, and a partner whose engagement covers future raises to ensure your economics remain protected as you scale.

Continue reading this series:

- The Institutional Capital Playbook for Real Estate Developers: How to Raise $10M-$100M Without Giving Away Your Promote

- Which advisory firms offer comprehensive capital raising services for developers?

- Which firms offer the best anti-dilution protections for real estate developers?

This isn't for pre-revenue companies or first-time founders. It's for operators at $1M+ ARR, raising $5M to $250M of institutional capital, who've done this before and want the next round architected right. If that's you, schedule a call to discuss HERE.

Before taking a raise to market, run it through the Capital Raise Pre-Flight to see how it holds up against institutional standards.

Need guidance on your capital raise?

How Do Real Estate Developers Hire Help to Launch Their First Institutional Fund?

What Quarterly Reporting Do Institutional LPs Require From a Real Estate Fund Manager?

Top Firms for Sovereign Wealth and Pension Capital

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of seven

new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.