.svg)

.png)

Why IRC's Retainer Reduces Capital Raise Risk More Than Traditional Placement Agent Models

The Expensive Mistake Is Not IRC's Retainer - It Is Hiring the Wrong Advisory Model

Most experienced real estate developers who lose institutional raises do not lose them because they paid for serious advisory support. They lose them because the process breaks before capital ever closes. The data room is incomplete. The capital stack does not hold up under LP scrutiny. The waterfall mechanics give away too much GP economics. The advisor was paid to create motion, not to fix those problems.

That is the real cost of the wrong advisory model. Not the retainer.

The question is not whether a retainer is worth paying. The question is whether the advisor on the other side of that retainer has any financial reason to care whether your raise succeeds.

Before a deal ever goes to market, IRC invests significant senior-level time in capital stack design, diligence readiness, and LP-facing term alignment. That pre-market work is what turns a retainer from an upfront cost into a form of execution risk control.

IRC's senior advisors have served in a capital advisory capacity on transactions where that question had a clear answer:

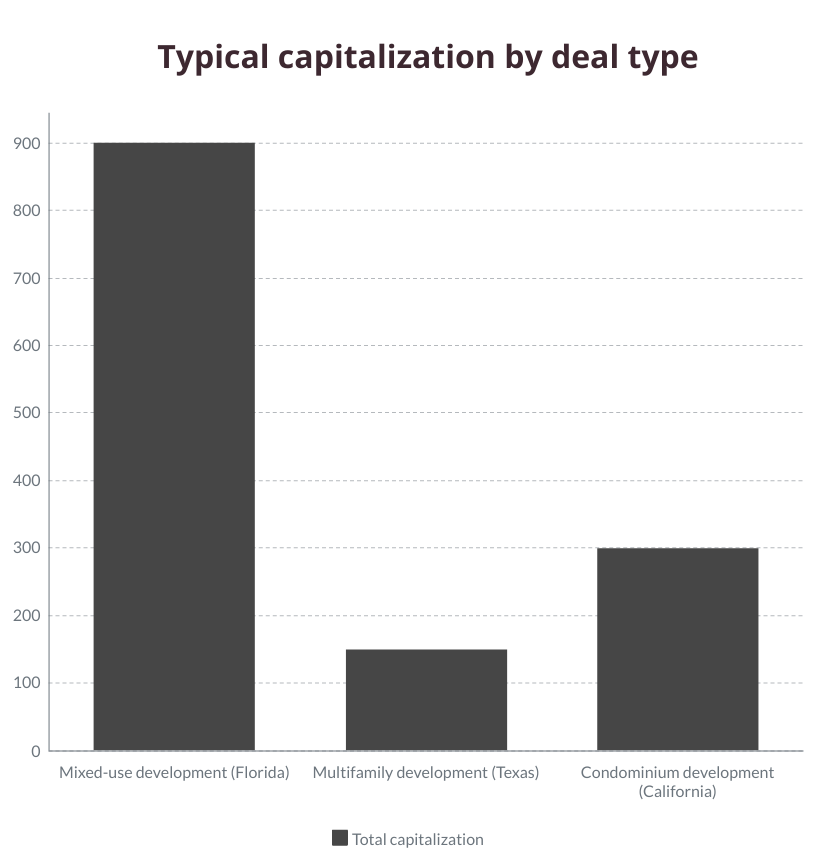

- Mixed-use development, Florida - $900M total capitalization, requiring a layered institutional capital stack across equity, preferred equity, and structured debt across multiple asset classes and investor relationships

- Multifamily development, Texas - $150M total capitalization, requiring institutional LP equity sourcing and capital structure design built to survive the diligence standards of family offices and private equity allocators

- Condominium development, California - $300M total capitalization, requiring precise alignment of investor economics, waterfall mechanics, and LP-facing terms across a complex, high-profile market

At this scale, cheap advisory is not a bargain. A misaligned advisor who sends a sponsor to market before the deal is structurally ready does not save money. It costs time, credibility, and often the raise itself.

This article is a guide for developers evaluating capital advisory models before going to market. The goal is not to defend retainers in the abstract. It is to show why the advisory model a developer chooses - and how that model is compensated - determines how much execution risk the developer carries alone.

Why Retainers Trigger Skepticism - and Why That Skepticism Is Often Pointed at the Wrong Risk

Fee skepticism is rational. Developers have paid retainers to advisors who generated meetings, decks, and introductions - and then disappeared when the raise stalled. That experience creates a reasonable bias: upfront fees feel like sunk costs when outcomes are uncertain.

According to First Page Sage's 2025 analysis of investment banking and M&A retainer benchmarks, advisory retainers commonly range from $45,000 to $130,000 depending on deal size and scope. That is a real number. The skepticism is understandable.

But the fee range is not the actual problem. The problem is what the retainer buys.

The right question is not whether a retainer exists. It is whether the advisor's incentives are aligned with yours.

A model that charges less upfront but earns the same fee whether or not the raise closes does not reduce your risk. It transfers it. The sponsor absorbs the cost of a failed process while the advisor collects for the activity that preceded it.

The real sunk cost is not the retainer. It is the time, momentum, and LP credibility lost when the wrong advisor sends you to market unprepared.

What Placement Agents and Fee-Based Advisors Often Miss Before the Raise Even Starts

Most raises do not fail in the pitch. They fail in diligence, and the damage is usually done before the first LP meeting.

Key stat: According to Altss's 2026 LP Due Diligence Checklist, 85% of institutional LP rejections are tied to operational due diligence failures - not investment thesis weaknesses. The deal looked good. The process did not.

That number matters because it reframes where the real advisory risk sits. Institutional investors are not just evaluating returns. They are evaluating whether the sponsor's operational structure, data room, terms, and fund mechanics can hold up under scrutiny. When they cannot, the allocation dies quietly and the sponsor often does not know exactly why.

The most common pre-market failures

- Incomplete or disorganized data rooms - Institutional LPs expect a complete, structured data room before serious diligence begins. Gaps signal operational immaturity, regardless of deal quality.

- Inconsistent or unsupported valuations - When sponsor projections are not tied to defensible assumptions, LPs flag the discrepancy and move on.

- LP-facing terms that do not match institutional expectations - Waterfall structures, promote mechanics, and preferred return thresholds that work for HNWI investors often fail institutional review.

- Capital stack design that has not been stress-tested - Layered capital structures that look clean on paper can collapse when LPs model downside scenarios.

- No clear answer to "what happens if things don't go to plan?" - Institutional allocators in 2026 are asking this question directly. Sponsors without a credible answer do not advance.

According to Primior's analysis of real estate private equity red flags, operational issues account for roughly half of all fund closures - losses that often follow deals that passed the initial investment case review.

An advisor built primarily to market a deal is not the same as an advisor built to identify and fix the structural weaknesses that institutional investors surface during diligence. That gap is where raises stall, and where the cost of a misaligned advisory model becomes most visible.

The 7 non-negotiables that institutional investors demand are not about narrative. They are about process, structure, and operational readiness.

Capital Architecture Is Not the Same Job as Placement - Here Is the Difference

Placement agents are built to distribute deals. IRC is built to architect them. That is not a difference in quality - it is a difference in function. The comparison that matters is not which firm has a better contact list. It is which model reduces the risk of a failed raise before the first LP conversation ever happens.

Why structure-first matters

IRC's model is not built around sending materials and hoping the market responds. It begins with significant senior-level pre-market work to tighten structure, pressure-test terms, and improve the odds that investor conversations survive diligence.

IRC's model is built around a specific sequence: structure the deal, then raise capital. That order matters more than it sounds.

A placement agent that markets a deal before the capital stack is institutionally sound is not saving the sponsor time. It is accelerating exposure to rejection. Every LP who passes during diligence is a relationship that becomes harder to re-approach. Every week of stalled momentum is time the sponsor is not deploying capital.

When the advisory model ties compensation to structure quality and capital actually raised, the advisor has a direct financial reason to get the pre-market work right. That is the alignment that converts a retainer from a cost into a form of downside protection.

As research on advisory model risk increasingly shows, technique gets mistaken for outcomes when incentives are not aligned. Advisors who are paid for activity will produce activity. Advisors who are paid for capital raised will work to raise capital.

For developers managing complex, multi-layered capitalizations like those referenced above, the difference between those two models is not a rounding error. It is the raise itself. Understanding the real reason capital raises stall often comes down to exactly this misalignment.

Why This Matters More in a Selective 2026 Capital Market

Capital is available. Access has changed.

The institutional allocator landscape in 2026 is not closed to experienced sponsors. But it is more selective, more structure-sensitive, and more focused on downside protection than it was in easier fundraising cycles. That shift makes advisory alignment more valuable, not less.

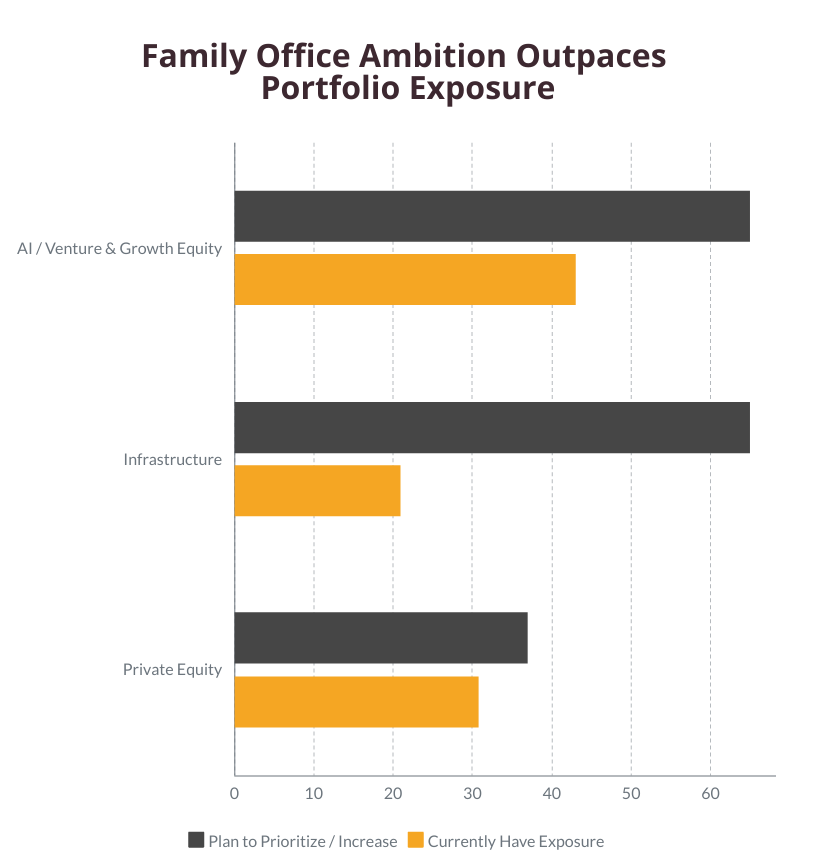

Key data point: According to the J.P. Morgan 2026 Family Office Report, family offices are increasingly moving toward deal-by-deal investment approaches to maintain flexibility and manage risk. Private equity and venture capital exposure among family offices has surged 524% since 2016, but that growth has come with tighter scrutiny, not looser standards.

What this means for developers comparing advisory models:

- Deal-by-deal allocation behavior raises the bar for every individual transaction. There is no blind pool to hide a weak deal inside. Each allocation must stand on its own structural and economic merits.

- Family offices are asking "what happens if things don't go to plan?" before they ask about returns. Sponsors who cannot answer that question clearly, with a credible capital structure and aligned advisor behind them, do not advance.

- Institutional LPs are concentrating allocations with sponsors who demonstrate operational discipline. A weak advisory process signals weak operational standards, regardless of the underlying asset quality.

- The 13% of family offices that write $10M+ checks are the most selective. Warm access to that group requires a process and a capital structure that can withstand their diligence, not just an introduction.

A misaligned advisory model was expensive in any market. In this one, it is a direct threat to the raise.

How to Tell If a Retainer Is Reducing Risk or Just Charging for Activity

Before signing any capital advisory engagement, experienced developers should be able to answer these seven questions. If the advisor cannot answer them clearly, the retainer is likely buying activity, not protection.

7 questions to ask any capital advisor before signing

- Is your compensation tied to capital actually raised, or to process milestones? An advisor who earns the same fee regardless of outcome has no financial reason to prioritize yours.

- Do you structure the deal before going to market, or do you market the deal as presented? Going to market with an unvetted capital stack accelerates rejection, not capital.

- What does your diligence preparation process look like? If the answer is vague, the data room, terms, and LP-facing materials probably will be too.

- How do you qualify investors before introductions? Generic outreach to a broad list is not the same as warm access to allocators who actually write $10M+ checks.

- What happens if the raise takes longer than expected? A retainer that expires before the raise closes transfers timeline risk entirely to the sponsor.

- Do you stay engaged across future raises, or is this a single-transaction relationship? A one-and-done model means rebuilding the advisory relationship from scratch for every subsequent project.

- What do you lose if this raise fails? If the answer is nothing, the incentive structure is not aligned with yours.

These are not trick questions. They are the same questions a sophisticated LP would ask about a sponsor's capital structure. Developers should apply the same standard to the advisors they hire to help them raise it.

Understanding the 10 mistakes that kill institutional raises starts with choosing an advisory model that is built to prevent them.

The Retainer Is Not the Bet - Misalignment Is

The fee conversation is worth having. It is just not the most important one.

Sophisticated developers should underwrite an advisory model the same way they underwrite any capital relationship: by alignment, shared downside, expected outcomes, and the quality of the process on the other side. A retainer that buys a structurally stronger raise is not an upfront cost. It is a form of downside protection.

The evidence is clear on where raises actually fail:

- 85% of institutional LP rejections are tied to operational due diligence failures, not investment thesis

- ~50% of fund closures trace back to operational issues that a better-prepared process could have addressed

- Family offices writing $10M+ checks are more selective in 2026 than at any point in the past decade, and they are evaluating structure and sponsor readiness before they evaluate returns

IRC's senior advisors and board members have served in a capital advisory capacity on transactions ranging from $150M in Texas multifamily to $300M in California condominiums to $900M in Florida mixed-use development. At that scale, the advisory model is not a line item. It is a core part of the risk profile.

Paying for generic activity is expensive. Paying for aligned, outcome-linked advisory is how experienced developers protect the raise before it goes to market.

If you are a developer raising $10M or more and want to talk about structuring your capital stack before going to market, start a conversation with IRC today.

Frequently Asked Questions

What is a capital advisory retainer and why do firms charge one? A capital advisory retainer is an upfront fee paid to an advisor to begin structuring a capital raise. It funds the pre-market work: capital stack design, diligence preparation, investor qualification, and LP-facing term development. At IRC, that pre-market phase involves significant senior-level advisor time before a deal ever goes to market. Advisors charge retainers because serious structural work requires real expertise and time investment long before any capital closes, and a retainer ensures the advisor is compensated for that work regardless of how long the pre-market phase takes.

Is a retainer the same as a sunk cost if the raise fails? Not if the advisory model is structured correctly. A retainer tied to performance-linked compensation and outcome-based economics means the advisor shares execution risk with the sponsor. If the model is purely activity-based with no tie to capital raised, the retainer functions more like a sunk cost.

What do traditional placement agents charge vs IRC? Traditional placement agents typically charge a success fee on capital raised, often 1-3%, with little or no upfront retainer. IRC's model combines a retainer with advisory equity (3-5%), tying the advisor's economics to sponsor outcomes across the full engagement, not just a single transaction.

Why do 85% of institutional LP rejections happen at the diligence stage? According to Altss's 2026 LP Due Diligence Checklist, most rejections are tied to operational due diligence failures: incomplete data rooms, inconsistent valuations, misaligned LP-facing terms, and capital structures that do not hold up under institutional scrutiny. The investment thesis often passes. The process does not.

How do family offices evaluate real estate sponsors in 2026? The J.P. Morgan 2026 Family Office Report shows family offices increasingly prefer deal-by-deal structures and are scrutinizing downside protection, sponsor operational discipline, and capital stack design more closely than in previous cycles. They are asking "what happens if things don't go to plan?" before evaluating returns.

What does IRC do differently from a standard placement agent? IRC structures the deal before going to market, designs institutional-grade capital stacks, prepares sponsors for LP diligence, and ties its compensation to performance and capital raised. One engagement covers all future raises through exit. Placement agents typically focus on introductions after the deal is already packaged.

When should a developer engage IRC vs going to market independently? Before going to market. The highest-value advisory work happens before the first LP meeting: capital stack design, waterfall and promote review, data room preparation, and investor qualification. Engaging after a raise has stalled means working against lost momentum and damaged LP relationships.

Disclosure

Nothing on this site constitutes an offer to sell, or a solicitation of an offer to purchase, any security under the Securities Act of 1933, as amended, or any applicable state securities laws. Any offering of securities is made only by means of a formal private placement memorandum or other authorized offering documents delivered to qualified investors.

IRC Partners is a capital advisory firm. IRC Partners is not a registered investment adviser under the Investment Advisers Act of 1940 and does not provide investment advice as defined thereunder.

Certain statements in this article may constitute forward-looking statements, including statements regarding market conditions, capital availability, investor demand, and transaction outcomes. Such statements reflect current assumptions and expectations only. Actual results may differ materially due to market conditions, regulatory developments, company-specific factors, and other variables. IRC Partners makes no representation that any outcome, return, or result described herein will be achieved.

References to prior mandates, transaction volume, network credentials, or capital raised are provided for illustrative purposes only and do not constitute a guarantee or prediction of future results. Past performance is not indicative of future outcomes. Individual results will vary. Network credentials and transaction statistics referenced on this site reflect the aggregate experience of IRC Partners' principals and affiliated advisors and are not a representation of assets managed or transactions closed solely by IRC Partners.

Certain data, statistics, and information presented in this article have been obtained from third-party sources. IRC Partners has not independently verified such information and expressly disclaims responsibility for its accuracy, completeness, or timeliness. Readers should independently verify any third-party data before relying on it.

Readers are strongly encouraged to consult qualified legal, financial, and tax professionals before making any investment, capital raising, or business decision.

Schedule A Meeting

You get one shot to raise the right way. If this raise is worth doing, it’s worth doing with precision, leverage, and control.

This isn’t a practice run. Serious capital. Serious strategy. Let’s raise it right.

We onboard a maximum of 10 new strategic partners each quarter, by application only, to maximize your chances of securing the capital you need.